Serving Arizona Homeowners Since 2004

|

Michael G. Branson, CEO of All Reverse Mortgage, Inc., and moderator of ARLO™, has 45 years of experience in mortgage banking, with the past 20 years devoted exclusively to reverse mortgages. A Forbes Real Estate Council member, he developed the industry's first fixed-rate jumbo reverse mortgage and has been featured in Forbes, Kiplinger, the LA Times, and Yahoo Finance. (License: NMLS# 14040) |

|

Cliff Auerswald, President of All Reverse Mortgage, Inc., and co-creator of ARLO™ — the industry's first real-time reverse mortgage pricing engine — has 27 years of experience in mortgage banking, with 20+ years focused exclusively on reverse mortgages. A recognized expert in reverse mortgage technology and consumer education, he has been featured in Kiplinger, Yahoo Finance, Realtor.com, and HousingWire. (License: NMLS# 14041) |

Arizona's average home value of $448,500 sits well under the 2026 HECM limit, so a standard reverse mortgage fits most homeowners here. This page answers the Arizona-specific questions: community property rules, manufactured homes, snowbird residency, and homes on tribal land.

Experience Excellence with Arizona’s Top Reverse Mortgage Lender

For over 20 years, All Reverse Mortgage, Inc. (ARLO™) has helped Arizona homeowners access their home equity through HUD-approved HECM and jumbo reverse mortgages. As Arizona’s #1 Rated Reverse Mortgage Lender, we hold an A+ BBB rating with perfect 5-star reviews and zero complaints — a record that earned us recognition as a BBB Torch Award for Ethics Finalist three years running.

As a HUD-approved direct lender and proud member of the National Reverse Mortgage Lenders Association (NRMLA), we specialize exclusively in reverse mortgages — it’s all we’ve done since 2004. Arizona’s popularity as a retirement destination means homeowners across the state — from active-adult communities in Sun City and Mesa to golf course properties in Scottsdale and high-value homes in Paradise Valley and Sedona — are increasingly using reverse mortgages as a strategic retirement planning tool. For properties that exceed the $1,249,125 HECM lending limit, our team introduced the first fixed-rate jumbo reverse mortgage in 2008, and our experienced originators can clearly explain the pros and cons of each program so you can choose the one that best fits your goals.

Whether you’re looking to eliminate monthly mortgage payments, create a financial safety net with a growing line of credit, or access equity for retirement planning, we’re here to help you choose the right program with competitive rates and lower costs. Let us show you the difference two decades of dedicated experience can make.

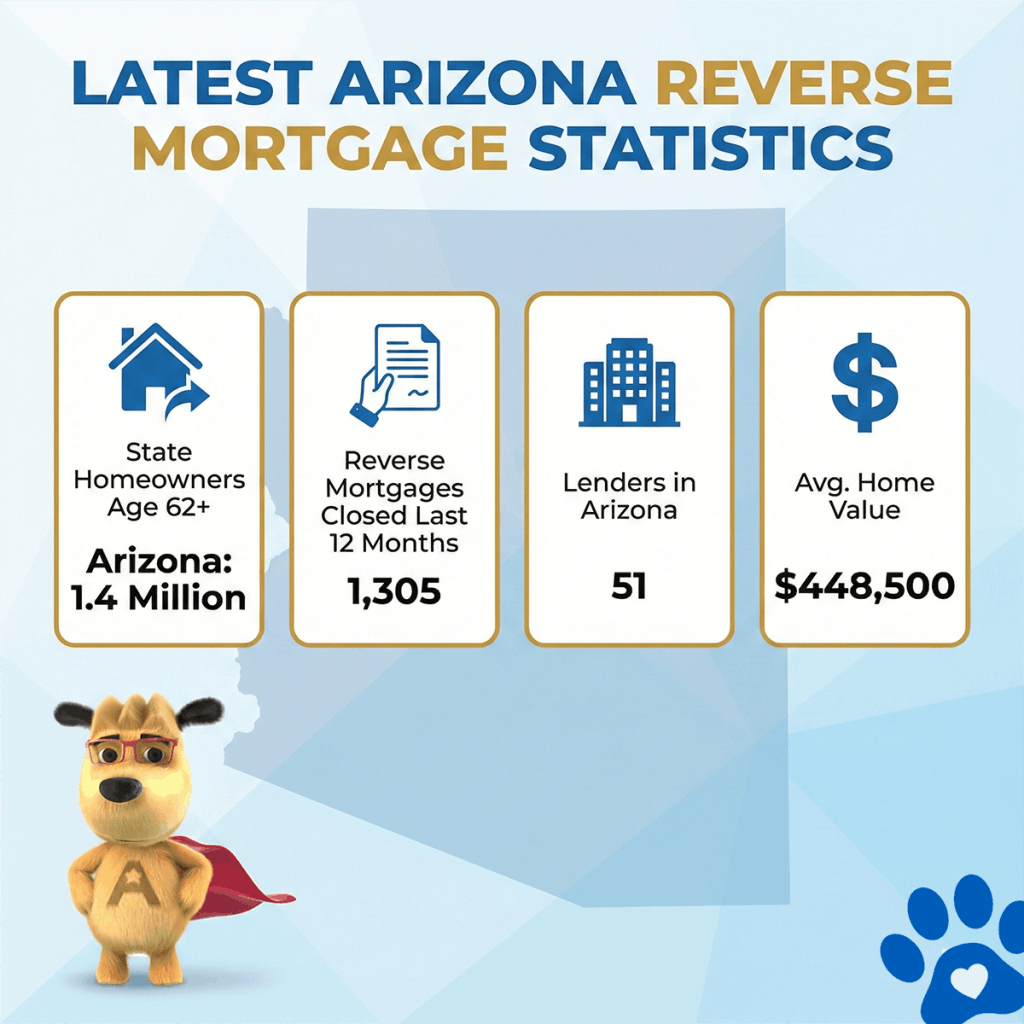

Arizona Reverse Mortgage Facts (2026 Update)

| State | Homeowners Age 62+ | Reverse Mortgages Closed Last 12 Months | Lenders in Arizona | Avg. Home Value |

|---|---|---|---|---|

| Arizona | 1.4 Million | 1,305 | 51 | $448,500 |

Top Reverse Mortgage Cities in Arizona

| City | Homeowners Age 62+ | Reverse Mortgages Closed Last 12 Mo. | Active Lenders | Avg. Home Value |

|---|---|---|---|---|

| Buckeye | 7,842 | 17 | 6 | $393,805 |

| Chandler | 18,214 | 29 | 8 | $517,058 |

| Gilbert | 19,887 | 33 | 8 | $565,937 |

| Glendale | 24,661 | 42 | 9 | $399,596 |

| Goodyear | 8,973 | 15 | 6 | $464,593 |

| Lake Havasu City | 15,442 | 18 | 7 | $455,741 |

| Mesa | 61,774 | 74 | 11 | $417,558 |

| Oro Valley | 9,116 | 8 | 4 | $525,306 |

| Peoria | 21,308 | 35 | 9 | $459,872 |

| Phoenix | 168,442 | 189 | 14 | $429,662 |

| San Tan Valley | 6,314 | 12 | 5 | $432,118 |

| Sedona | 5,287 | 4 | 3 | $793,200 |

| Scottsdale | 38,118 | 41 | 10 | $793,200 |

| Sun City | 31,884 | 9 | 5 | $347,115 |

| Sun Lakes | 9,442 | 6 | 4 | $478,221 |

| Surprise | 15,229 | 19 | 7 | $409,884 |

| Tucson | 72,418 | 60 | 10 | $327,904 |

How this data was derived: Reverse mortgage counts reflect FHA-insured HECM loans endorsed over a rolling 12-month period (Dec 2024–Nov 2025) using HUD HECM Snapshot data. Active lenders represent unique FHA sponsor numbers with at least one endorsed loan during this period. Estimated homeowners age 62+ are based on U.S. Census ACS 5-year owner-occupied households age 65+ as a conservative proxy. Home values are sourced from Zillow’s Home Value Index (latest available).

Top 20 Reverse Mortgage Lenders in Arizona

| Lender | BBB Rating | Accredited | Years in Business | Customer Rating (0–5) | % Positive Reviews | Complaints | Source |

|---|---|---|---|---|---|---|---|

| All Reverse Mortgage, Inc. (ARLO) | A+ | YES | 21 | 4.94/5 | 99.0% | 0 | Source |

| American Pacific Mortgage | F | NO | 28 | 1.75/5 | 35.0% | 6 | Source |

| CrossCountry Mortgage, LLC. | F | YES | 22 | 1.43/5 | 29.0% | 303 | Source |

| Fairway Independent Mortgage | A+ | YES | 29 | 4.51/5 | 90.0% | 26 | Source |

| Finance of America Reverse LLC (FAR) | A+ | YES | 22 | 3.71/5 | 74.0% | 36 | Source |

| Goodlife Home Loans | A+ | YES | 13 | N/A (Not enough reviews) | N/A (Not enough reviews) | 1 | Source |

| Guaranteed Rate | A+ | YES | 26 | 2.25/5 | 45.0% | 45 | Source |

| Guild Mortgage Company LLC | A+ | NO | 65 | 1.55/5 | 31.0% | 73 | Source |

| HighTechLending Inc | A+ | YES | 19 | 4.94/5 | 99.0% | 1 | Source |

| Liberty Home Equity Solutions Inc. | A+ | NO | 22 | 1.00/5 | 20.0% | 1 | Source |

| Longbridge Financial LLC | A+ | YES | 13 | 3.77/5 | 75.0% | 34 | Source |

| Luminate Bank | NR | NO | 84 | NA | NA | NA | Source |

| MCM Holdings | A+ | YES | 27 | NA | NA | NA | Source |

| The Money House | NR | NO | 28 | NA | NA | 0 | Source |

| Movement Mortgage, LLC | A+ | NO | 18 | 4.43/5 | 89.0% | 92 | Source |

| Mutual of Omaha Mortgage | A+ | YES | 12 | 3.31/5 | 66.0% | 65 | Source |

| New American Funding | A+ | YES | 26 | 4.65/5 | 93.0% | 147 | Source |

| Plaza Home Mortgage Inc | A+ | YES | 24 | 2.67/5 | 53.0% | 6 | Source |

| Smartfi Home Loans | A+ | YES | 6 | N/A (Not enough reviews) | N/A (Not enough reviews) | 0 | Source |

| South River Mortgage, LLC | A+ | NO | 6 | 3.79/5 | 76.0% | 14 | Source |

Arizona Reverse Mortgage Lending Limits

Arizona is home to over 7.6 million people, and nearly 1.4 million residents may be eligible for a reverse mortgage, offering a valuable financial option for many.

As of January 2026, Arizona’s average home value is $448,500 — well below the HECM reverse mortgage lending limit of $1,249,125. This makes Arizona an attractive place for homeowners considering a reverse mortgage.

Arizona is the sixth-largest state in the U.S. by area and ranks 14th in population, with Phoenix as its capital. As one of the “Four Corners” states, Arizona shares borders with New Mexico, Utah, Nevada, California, and Mexico and has a rich history dating back to its early Spanish settlers in the 1500s.

Over the centuries, Arizona has evolved from its days of gold and silver rushes to become a major copper mining hub, now producing half of the nation’s newly mined copper. The state’s unique climate and geography have made it a popular retirement destination, offering both hot desert climates and cooler, forested areas.

Today, one-quarter of Arizona’s land is made up of Indian reservations, home to 27 federally recognized Native American tribes, including the Navajo Nation, the largest Native American tribe in the country.

Whether you’re drawn to the sunny deserts of Southern Arizona or the cooler forests of the north, if you’re a homeowner aged 62 or older, a reverse mortgage could be a smart financial tool to enhance your retirement. At All Reverse Mortgage, Inc. (ARLO™), we’re here to answer your questions and help you explore your options.

Arizona Reverse Mortgage FAQs

I’m a snowbird who spends summers in another state. Can I still get a reverse mortgage on my Arizona home?

Can a reverse mortgage help me afford rising air conditioning costs during Arizona summers?

I live in Sun City/Sun Lakes/another age-restricted community with HOA fees. Can I use reverse mortgage funds to pay these?

I own a manufactured home in a retirement park. Does it qualify?

Can I get a reverse mortgage on property located on tribal land or a reservation?

How does Arizona’s community property law affect my reverse mortgage if I’m married?

Can I use reverse mortgage funds to install solar panels or a pool to increase my home’s value?

What happens to my reverse mortgage during monsoon season if my home is damaged?

How do property taxes factor in? I heard Arizona has relatively low property taxes for seniors.

HUD-Approved Reverse Mortgage Counseling Agencies in Arizona

| Name | Agency ID | Address | Phone | Web Site |

|---|---|---|---|---|

| ADMINISTRATION OF RESOURCES AND CHOICES (ARC) | 81809 | 1625 N Alvernon Way Ste 101, Tucson, Arizona, 85712-3370 | (602) 374-2226 | arc-az.org |

| ADMINISTRATION OF RESOURCES AND CHOICES (ARC) | 81052 | 5800 W Glenn Dr Ste 275, Glendale, Arizona, 85301-2499 | (520) 623-9383 | arc-az.org |

| CREDIT.ORG - GOODYEAR, AZ BRANCH | 90589 | 15150 W Park Pl, Goodyear, Arizona, 85395-2385 | (480) 542-1865 | credit.org |

Did you know? Arizona does not mandate in-person counseling. Visit our counseling page for a list of phone-based counseling agencies and conduct your required counseling from the comfort of your home.

Ready to Unlock Your Home’s Equity?

As Arizona’s #1 Rated Reverse Mortgage Lender, All Reverse Mortgage, Inc. (ARLO™) is here to provide trusted guidance, real-time rates, and expert support to help you make informed decisions.

✔ No obligations. Just real-time rates and expert advice.

✔ Instant quote. No personal info required.

✔ Licensed experts. Get clear, honest answers.

All Reverse Mortgage, Inc. is fully licensed by the Arizona Department of Insurance and Financial Institutions (License #0934287), ensuring that you receive expert guidance every step of the way.

Get Your Reverse Mortgage Quote from Arizona’s #1 Rated Reverse Mortgage Lender, or call (800) 565-1722 to speak with a licensed expert.

Other Areas of Interest in Arizona

Buckeye Chandler Gilbert Glendale Goodyear Lake Havasu City Mesa Oro Valley Peoria Phoenix San Tan Valley Sedona Scottsdale Sun City Sun Lakes Surprise Tucson

Additional Resources: