Reverse Mortgages in Sun Lakes

|

Michael G. Branson, CEO of All Reverse Mortgage, Inc., and moderator of ARLO™, has 45 years of experience in mortgage banking, with the past 20 years devoted exclusively to reverse mortgages. A Forbes Real Estate Council member, he developed the industry's first fixed-rate jumbo reverse mortgage and has been featured in Forbes, Kiplinger, the LA Times, and Yahoo Finance. (License: NMLS# 14040) |

|

Cliff Auerswald, President of All Reverse Mortgage, Inc., and co-creator of ARLO™ — the industry's first real-time reverse mortgage pricing engine — has 27 years of experience in mortgage banking, with 20+ years focused exclusively on reverse mortgages. A recognized expert in reverse mortgage technology and consumer education, he has been featured in Kiplinger, Yahoo Finance, Realtor.com, and HousingWire. (License: NMLS# 14041) |

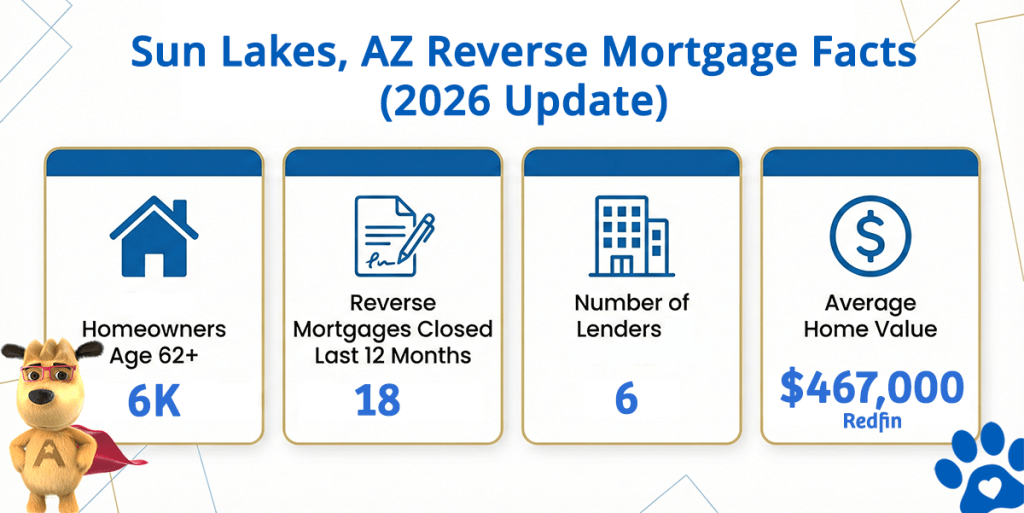

Sun Lakes Reverse Mortgage Market at a Glance

Sun Lakes Reverse Mortgage Facts (2026 Update)

| City | Homeowners Age 62+ | Reverse Mortgages Closed Last 12 Months | Lenders in Sun Lakes (est) | Avg. Home Value |

|---|---|---|---|---|

| Sun Lakes | ~6,000 | 18 | 6 | $467,000 |

Data sources: U.S. Census Bureau (demographic and household data), Zillow (home values), and HUD HECM database (lending activity and lender participation).

What the Numbers Tell Us About Sun Lakes

Sun Lakes, located in the Southeast Valley 55+ community region, commands a median home value of $467,000, representing substantial equity accessible to qualifying homeowners. With approximately 6,000 households age 62 and older, and six active reverse mortgage lenders serving the area, Sun Lakes demonstrates robust market depth. The $1,249,125 HECM limit represents meaningful borrowing capacity for most Sun Lakes residents seeking to tap their home equity strategically.

The demographics matter significantly: as a 55+ community, Sun Lakes naturally aligns with reverse mortgage borrower profiles. Nearby communities—Chandler, Gilbert, and Mesa—add regional context, as residents often consider equity access strategies alongside broader financial planning. Home values in this established community have appreciated steadily, building equity for long-term residents.

For Sun Lakes homeowners, reverse mortgages frequently address three primary needs: consolidating existing debt, funding healthcare or long-term care expenses, and supplementing retirement income through disciplined access to home equity.

Sun Lakes Market Strength: With six active HECM lenders and a substantial age-62+ population, Sun Lakes offers competitive loan terms, specialized servicing, and lending professionals experienced with Southeast Valley borrower profiles.

How a Reverse Mortgage Works for Sun Lakes Homeowners

A reverse mortgage allows homeowners age 62 and older to access home equity as cash without monthly payment obligations. You retain full home ownership, maintain occupancy, and continue paying property taxes, insurance, and maintenance. HUD’s HECM program is the federally-insured reverse mortgage available in Sun Lakes, featuring consumer protections, standardized underwriting, and mandatory borrower counseling.

The loan becomes due when the last borrower permanently relocates, passes away, or sells the property. Heirs retain non-recourse protection—if the home sells for less than the loan balance, your heirs owe nothing beyond the sale proceeds.

Common Uses in Sun Lakes

- Paying off existing mortgages: Use loan proceeds to eliminate monthly mortgage payments and free up retirement income.

- Funding healthcare transitions: Access capital for in-home care, medical equipment, or assisted living expenses.

- Covering home modifications: Finance accessibility upgrades, safety improvements, or aging-in-place enhancements.

- Establishing a financial cushion: Create a line of credit for unexpected expenses or lifestyle flexibility.

Sun Lakes Reverse Mortgage Eligibility

| Requirement | Details |

|---|---|

| Minimum Age 62 | All borrowers must satisfy the minimum age requirement. Most Sun Lakes residents already qualify by age. |

| Primary Residence Status | The home must be your primary residence. Second homes, investment properties, and rental units are ineligible. |

| Sufficient Home Equity | Own the home outright or carry minimal mortgage debt. The property must meet FHA standards for structural condition and safety. |

| Financial Capacity Assessment | No minimum credit score exists. Lenders evaluate your ability to cover property taxes, insurance, and HOA dues. |

| HUD Counseling Completion | A HUD-approved counseling session is mandatory before proceeding with loan approval. |

| Professional Home Appraisal | A licensed appraisal verifies property value and confirms FHA compliance. |

Use the reverse mortgage calculator to estimate how much you could borrow based on your age, home value, and current interest rates.

Understanding the Costs

Closing costs include origination fees (up to 2% of home value), property appraisal, title insurance, recording fees, and survey costs if needed. Most lenders allow you to finance these costs within the loan, reducing upfront cash requirements from your pocket.

Ongoing costs—property taxes, homeowners insurance, HOA fees, and home maintenance—remain your responsibility throughout the loan. You have no monthly payment obligation. Interest accrues on borrowed amounts and is repaid when the loan concludes, whether through home sale, relocation, or transfer to your heirs.

FHA mortgage insurance protects both you and the lender, ensuring funds remain available if the lender fails and capping your repayment obligation at the home’s value—your heirs keep any remaining equity.

Is a Reverse Mortgage Right for You?

Review the complete list of advantages and disadvantages. A reverse mortgage works well for some households but may not suit others. Consider how long you plan to stay in the home, your immediate funding needs, your broader financial situation, and your goals for leaving an inheritance.

If a reverse mortgage doesn’t fit your situation, other home equity solutions are available, including traditional home equity lines of credit, second mortgages, and cash-out refinances. Comparing a HELOC against a reverse mortgage helps you determine which approach best matches your financial objectives.

HUD-Approved Direct Lender Serving Sun Lakes

Partner with HUD-approved HECM lenders holding current Arizona licensing. The Arizona Department of Financial Institutions oversees all residential mortgage lenders. Confirm your lender’s state license (DIFI License #BK0934287 for regulated lenders) and active HUD approval status before proceeding.

When evaluating lenders, request current interest rates from multiple providers, verify their reputation and customer satisfaction ratings, and confirm they offer jumbo reverse mortgages if your Sun Lakes home value exceeds HECM limits.

Get Your Sun Lakes Reverse Mortgage Consultation

Connect with a reverse mortgage specialist familiar with Sun Lakes’ market, homeowner demographics, and available product options.

Related Resources

Detailed walkthrough of the reverse mortgage mechanics and process flow.

Clarify misconceptions with evidence-based information about reverse mortgages.

In-depth overview of eligibility criteria and underwriting evaluation factors.

Learn what happens during appraisal and how valuation affects borrowing capacity.

Statewide HECM limits, lending trends, and active lender network information.

Insights into the Scottsdale metro area and lending activity patterns.

This information is educational in nature and should not be construed as financial or legal advice. Reverse mortgage products, terms, rates, and availability vary by lender and individual borrower circumstances. All products are subject to credit approval. Arizona Licensed Lender DIFI License #BK0934287. For current HUD HECM information and to verify lender status, visit HUD’s HECM resource center.