REAL-TIME REVERSE MORTGAGE RATES

|

Michael G. Branson, CEO of All Reverse Mortgage, Inc., and moderator of ARLO™, has 45 years of experience in mortgage banking, with the past 20 years devoted exclusively to reverse mortgages. A Forbes Real Estate Council member, he developed the industry's first fixed-rate jumbo reverse mortgage and has been featured in Forbes, Kiplinger, the LA Times, and Yahoo Finance. (License: NMLS# 14040) |

|

Cliff Auerswald, President of All Reverse Mortgage, Inc., and co-creator of ARLO™ — the industry's first real-time reverse mortgage pricing engine — has 27 years of experience in mortgage banking, with 20+ years focused exclusively on reverse mortgages. A recognized expert in reverse mortgage technology and consumer education, he has been featured in Kiplinger, Yahoo Finance, Realtor.com, and HousingWire. (License: NMLS# 14041) |

Current Reverse Mortgage Rates: Today’s Rates, APR | ARLO™

HECM Reverse Mortgage Rates

The Home Equity Conversion Mortgage (HECM) is the most widely used reverse mortgage in the United States, insured by the FHA and backed by HUD. It is available to homeowners age 62 or older and offers the widest range of payment options, including lump sum, line of credit, term, and tenure, up to the 2026 lending limit of $1,249,125.

| Fixed Rate (APR) | Adjustable Rate (Margin) | 2026 Lending Limit |

|---|---|---|

| 7.680% (9.191%e APR) | 5.875% (1.750 Margin) | $1,249,125 |

| 7.810% (9.339%e APR) | 6.125% (2.000 Margin) | $1,249,125 |

APR Disclosure (Fixed Rate) ▼ click to expand

The Annual Percentage Rate (APR) figures shown are estimates calculated in accordance with Regulation Z (12 CFR Part 1026) and are provided for comparison purposes only. APR figures are based on the following assumed scenario: borrower age 70 | loan amount $250,000 | located in California. Finance charges included in the APR calculation: upfront Mortgage Insurance Premium (2.00% of the Maximum Claim Amount), annual Mortgage Insurance Premium (0.50% per year), estimated origination fee, and standard third-party closing costs (title insurance, appraisal, escrow, and recording fees). A loan term of 2 years is assumed per Regulation Z. Fixed-rate payment option: Lump Sum only. Actual APR will vary. This is not a commitment to lend.

Adjustable-Rate APR Notice ▼ click to expand

Adjustable-rate HECM products do not have a fixed APR; the rate will change based on the 12-Month CMT index plus the applicable margin shown above. The lifetime interest rate cap is 5% over the initial start rate. Adjustable-rate payment options: Line of Credit, Term, Tenure, or Combination. HECM adjustable rates are rounded to the nearest 1/8th.

Adjustable-Rate Note ▼ click to expand

On adjustable-rate HECM products, the interest rate adjusts monthly. The fully indexed note rate is calculated by adding the current 12-Month CMT index value to the applicable margin at the time of each adjustment. As the index rises or falls, the note rate, and the rate at which interest accrues on the loan balance, will change accordingly, subject to the periodic and lifetime caps disclosed above.

Index: 12-Mo. CMT | Lifetime Cap: 5% Over Start Rate | 2026 HECM Lending Limit: $1,249,125

Rates are subject to change without notice. Last updated: 08/06/2026

HECM for Purchase Reverse Mortgage Rates

The HECM for Purchase program allows homebuyers age 62 or older to purchase a new primary residence using a reverse mortgage. This combines a one-time down payment with no required monthly mortgage payments. Rates are identical to those of the standard HECM program and are subject to the same 2026 lending limit of $1,249,125. Use our HECM for Purchase calculator to estimate your required down payment.

| Fixed Rate (APR) | Adjustable Rate (Margin) | 2026 Lending Limit |

|---|---|---|

| 7.680% (9.297%e APR) | 5.875% (1.750 Margin) | $1,249,125 |

| 7.810% (9.446%e APR) | 6.125% (2.000 Margin) | $1,249,125 |

APR Disclosure (Fixed Rate) ▼ click to expand

The Annual Percentage Rate (APR) figures shown are estimates calculated in accordance with Regulation Z (12 CFR Part 1026) and are provided for comparison purposes only. APR figures are based on the following assumed scenario: borrower age 70 | loan amount $250,000 | located in California. Finance charges included in the APR calculation: upfront Mortgage Insurance Premium (2.00% of the Maximum Claim Amount), annual Mortgage Insurance Premium (0.50% per year), estimated origination fee, and standard third-party closing costs (title insurance, appraisal, escrow, and recording fees). A 2-year loan term is assumed per Regulation Z. Fixed-rate payment option: Lump Sum only. Actual APR will vary. This is not a commitment to lend.

Adjustable-Rate APR Notice ▼ click to expand

Adjustable-rate HECM for Purchase products do not have a fixed APR; the rate will change based on the 12-Month CMT index plus the applicable margin shown above. The lifetime interest rate cap is 5% over the initial start rate. Adjustable-rate payment options: Line of Credit, Term, Tenure, or Combination. HECM adjustable rates are rounded to the nearest 1/8th.

Adjustable-Rate Note ▼ click to expand

On adjustable-rate HECM for Purchase products, the interest rate adjusts monthly. The fully indexed note rate is calculated by adding the current 12-Month CMT index value to the applicable margin at each adjustment. As the index rises or falls, the note rate, and the rate at which interest accrues on the loan balance, will change accordingly, subject to the periodic and lifetime caps disclosed above.

HECM for Purchase (H4P) Notice ▼ click to expand

The HECM for Purchase program allows borrowers age 62 or older to purchase a new primary residence using a reverse mortgage. The buyer makes a one-time down payment at closing, typically 29% to 63% of the purchase price depending on age, interest rate, and property value. No monthly mortgage payments are required. Use our HECM for Purchase calculator to estimate your required down payment. The loan becomes due when the last borrower permanently leaves the home. Borrowers remain responsible for property taxes, homeowner’s insurance, and home maintenance.

Index: 12-Mo. CMT | Lifetime Cap: 5% Over Start Rate | 2026 HECM Lending Limit: $1,249,125

Rates are subject to change without notice. Last updated: 08/06/2026

Jumbo Reverse Mortgage Rates

Designed for homes exceeding the HECM lending limit, jumbo reverse mortgages (also called proprietary reverse mortgages) offer loan amounts up to $4,000,000 with no FHA mortgage insurance premiums.

| Rate Type | Fixed Rate (APR) / Adjustable Rate (Margin) | Lending Limit |

|---|---|---|

| Fixed | 7.990% (8.069%e APR) | $4,000,000 |

| Fixed | 8.950% (8.957%e APR) | $4,000,000 |

| Fixed | 8.980% (9.134%e APR) | $4,000,000 |

| Fixed | 8.990% (9.218%e APR) | $4,000,000 |

| Adjustable | 9.705% (5.625 Margin) | $4,000,000 |

APR Disclosure (Fixed Rate) ▼ click to expand

The Annual Percentage Rate (APR) figures shown are estimates calculated in accordance with Regulation Z (12 CFR Part 1026) and are provided for comparison purposes only. APR figures are based on the following assumed scenario: borrower age 70 | loan amount $1,000,000 | located in California. Finance charges included in the APR calculation: estimated origination fee and standard third-party closing costs (title insurance, appraisal, escrow, and recording fees). Jumbo reverse mortgage products are not FHA-insured and do not carry mortgage insurance premiums. A 2-year loan term is assumed per Regulation Z. Fixed-rate payment option: Lump Sum only. Actual APR will vary. This is not a commitment to lend.

Adjustable-Rate APR Notice ▼ click to expand

Adjustable-rate Jumbo reverse mortgage products do not have a fixed APR; the rate will change based on the applicable index plus the margin shown above. Because the rate is variable, a single APR cannot be stated. The rate and margin shown reflect current market conditions as of the date last updated above and are subject to change without notice. On adjustable-rate Jumbo products, the interest rate adjusts monthly. The fully indexed note rate is determined by adding the current applicable index value to the margin at the time of each adjustment, and the rate at which interest accrues on the loan balance will change accordingly. Adjustable-rate payment options: Lump Sum or Line of Credit.

Jumbo Reverse Mortgage Notice ▼ click to expand

Jumbo reverse mortgage products (also called proprietary reverse mortgages) are privately insured loan products not backed by the FHA or HUD. They are designed for borrowers with higher-value homes that exceed the HECM lending limit of $1,249,125. Loan amounts up to $4,000,000 may be available, depending on the borrower’s age, property value, and lender guidelines. No monthly mortgage payments are required. The outstanding loan balance, including all accrued interest and applicable fees, becomes due and payable in full upon the occurrence of a maturity event, which includes: the sale or transfer of the property; the death of the last surviving borrower; or the borrower’s failure to occupy the property as their principal residence. Borrowers remain responsible for property taxes, homeowner’s insurance, and home maintenance.

Jumbo Lending Limit: up to $4,000,000 | Fixed: Lump Sum only | Adjustable: Lump Sum or Line of Credit

Rates are subject to change without notice. Last updated: 08/06/2026

Disclosure: Interest rates, APR figures, and loan terms referenced anywhere on this website are triggering terms under Regulation Z (12 CFR §1026.24). Any such references on other pages of this site are provided for general informational purposes only and do not constitute complete disclosures. Consumers are directed to this rates page for full disclosures of rates, APRs, terms, and programs. Rates are subject to change without notice and may not be available in all states. All Reverse Mortgage, Inc. is a HUD-approved lender (NMLS# 13999). View licensed states.

How Interest Rates Affect Your Available Loan Amount

The amount of home equity available through a reverse mortgage is directly tied to the interest rate at the time of your loan. This is one of the most important, and most commonly overlooked, aspects of reverse mortgage planning. Unlike a traditional mortgage where the rate determines your monthly payment, the reverse mortgage rate determines how much of your equity you can access.

All HECM (Home Equity Conversion Mortgage) reverse mortgages use a standardized table published by the Department of Housing and Urban Development to calculate your loan amount. This amount, known as the principal limit, depends on three primary factors: your age (or the age of your spouse, if younger), your appraised home value (or the lending limit, whichever is lower), and the current expected interest rate.

The basic rule: when interest rates are lower, you qualify for a higher percentage of your home’s value. When rates are higher, the available percentage decreases. The percentage of home equity you can access currently ranges from approximately 35.1% to 71.3%, depending on age and rate. Older homeowners qualify for a larger share than younger ones.

2026 HECM Reverse Mortgage LTV by Age Chart

| Age of Borrower | Principal Limit Factor (PLF) | Current Lending Limit |

|---|---|---|

| 62 | 35.1% | $1,249,125 |

| 65 | 37.2% | $1,249,125 |

| 70 | 40.9% | $1,249,125 |

| 75 | 43.8% | $1,249,125 |

| 80 | 48.2% | $1,249,125 |

| 85 | 54.4% | $1,249,125 |

| 90 | 61.4% | $1,249,125 |

| Note: Principal Limit Factors (PLF) sourced from HUD.gov, based on an expected rate of 5.875%. Net PLF requires deducting costs, including upfront insurance (~3%). | ||

See what today’s rates mean for your specific situation. Call (800) 565-1722 or use our reverse mortgage calculator for real-time rates and side-by-side comparisons →

Reverse Mortgage Payment Options by Rate Type

Fixed-Rate HECM

- Payment option: Single lump-sum disbursement at closing.

- Interest rate: Locked at closing and does not change for the life of the loan.

The fixed rate is generally best if you need most or all of your available funds at closing, typically to pay off an existing mortgage balance or to fund a reverse mortgage home purchase. Be aware that the 60% disbursement rule limits how much can be drawn in the first 12 months unless the funds are being used to pay off an existing lien.

Adjustable-Rate HECM

- Payment options: Single lump sum, line of credit, term, tenure, or any combination.

- Interest rate: Adjusts monthly based on the 12-Month CMT index plus the applicable margin, with a periodic cap of 2% per adjustment and a lifetime cap of 5% over the initial start rate.

Adjustable rates offer more flexibility in how funds are accessed. See our fixed vs. adjustable rate comparison for a detailed breakdown.

Fixed-Rate vs. Adjustable-Rate: Key Considerations

Choosing between a fixed rate and an adjustable rate is one of the biggest decisions in the reverse mortgage process, and the right answer depends entirely on how you plan to use the funds.

A fixed-rate HECM requires you to take the entire loan amount as a lump sum at closing. If you’re paying off a large existing mortgage, this works well because the funds are immediately applied. If you have little or no existing mortgage debt, taking the full amount at closing means receiving funds you may not need right away, while interest begins accruing on the entire balance from day one.

An adjustable-rate HECM allows you to draw funds over time as a line of credit, monthly payments, or a combination. Interest accrues only on the amount you actually draw, not on the full available balance. If you want ongoing access to funds rather than a single disbursement, the adjustable rate often costs less over the life of the loan.

The adjustable rate carries the risk of future rate increases (the lifetime cap is 5% above the initial start rate), but this is offset by the line of credit growth feature and the ability to control how much you draw and when. If you’re unsure which option fits your situation, a HUD-approved counselor can walk you through the numbers at no cost.

How the Line of Credit Growth Feature Works

The HECM line of credit works differently from the Home Equity Lines of Credit (HELOCs) available from traditional lenders, and that difference can affect your retirement planning.

Unlike a HELOC, which a bank can freeze, reduce, or cancel at any time, the HECM line of credit is guaranteed by the FHA. Once established, the unused portion of your line cannot be frozen or reduced, regardless of changes in the housing market or your financial situation. For a direct comparison, see Reverse Mortgage vs. HELOC: which is smarter for retirees?

The unused portion of your line grows at a rate equal to the current interest rate plus the annual mortgage insurance premium (0.50%). For example, if you establish a $100,000 line, use $45,000 to pay off an existing mortgage and closing costs, and leave the remaining $55,000 untouched, that unused portion grows at the compounding rate. At a note rate of 5% plus the 0.50% MIP, the growth rate would be 5.5%, adding approximately $3,025 in available credit in the first year alone.

Credit line growth is not income and is not taxable. It simply represents an increase in your available borrowing capacity. If you never draw the funds, no interest accrues on the growth. It’s simply more credit available to you if you need it.

Monthly Payment Plans

You can also receive reverse mortgage proceeds as monthly payments. These can be structured as tenure payments (paid every month for as long as you live in the home, even if you outlive your life expectancy), term payments (paid for a specified number of months), or a combination. Learn more about term, ten-year, and tenure payment options.

Any of these payment structures can be combined into a modified plan. For example, you could take a partial lump sum to pay off an existing mortgage, establish a line of credit for future needs, and receive monthly tenure payments for ongoing income. The allocation depends on your age, interest rate, and total available principal limit.

How Interest Rates and Margins Affect the Principal Limit

The expected interest rate is the key variable that determines how much of your equity you can access. On adjustable-rate products, the expected rate is derived from a 10-year Treasury index plus the lender’s margin, which means that when margins are lower, you qualify for a higher principal limit.

This is why most people who run the numbers end up with a higher available balance on the adjustable-rate program than on the fixed-rate option, because the expected rate calculation typically produces a more favorable result.

The margin also affects the rate at which interest accrues on the outstanding balance over the life of the loan. A higher margin means less money available at closing and faster interest accumulation over time. When comparing lenders, the margin on an adjustable-rate product and the note rate on a fixed-rate product are the most important figures to evaluate, along with origination fees and closing costs.

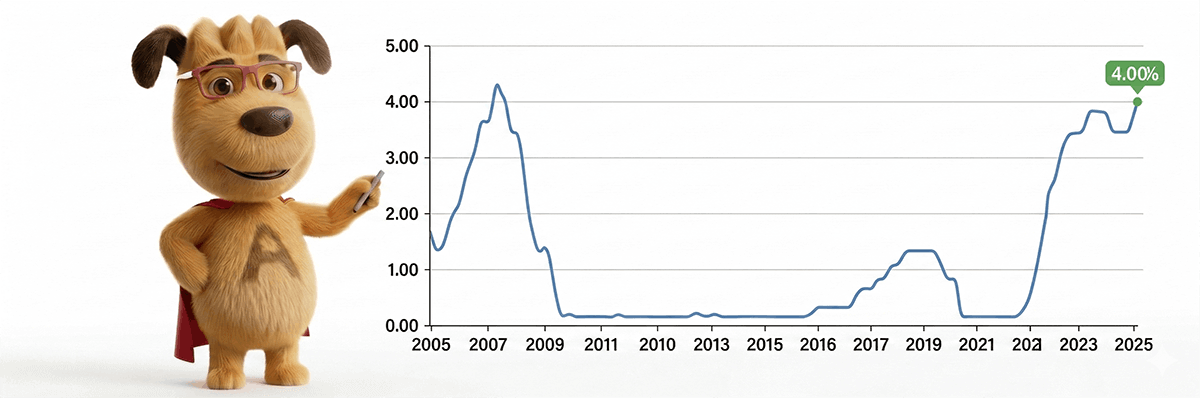

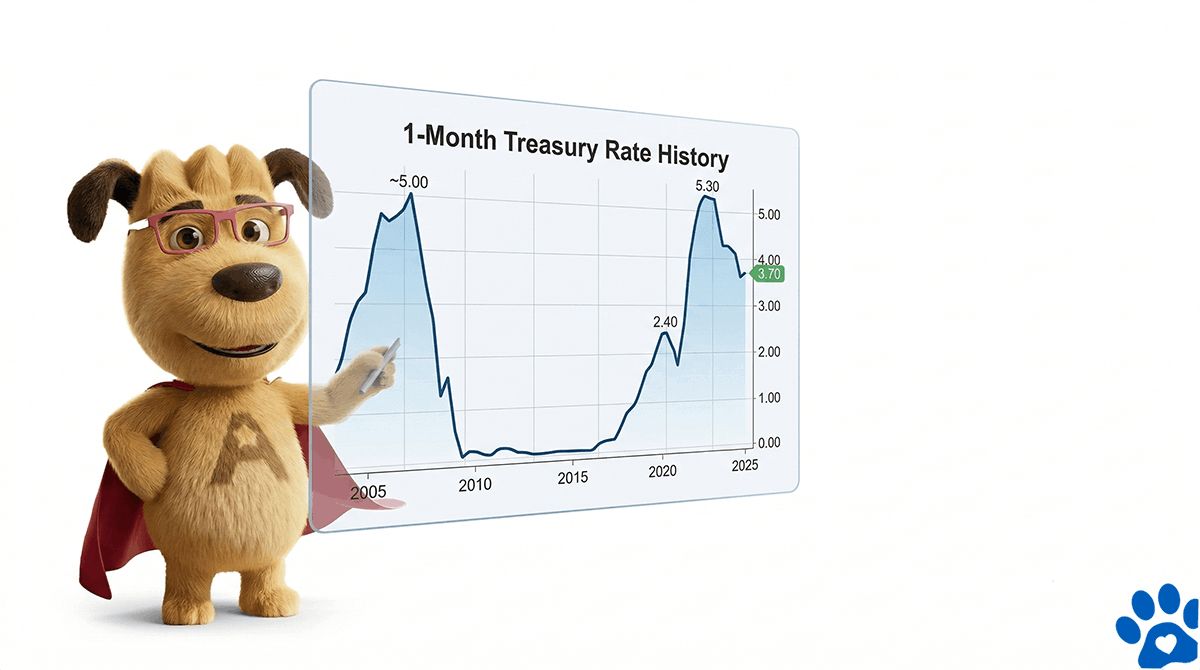

Treasury Index History

The CMT Index (Constant Maturity Treasury Index) is based on the average monthly yield of Treasury Securities adjusted to a constant maturity equivalent of one year. GNMA announced in September 2020 that it would no longer allow LIBOR to be used for HECM loans, effective February 2021. The long-term goal was to transition to the SOFR index (Secured Overnight Financing Rate), which unlike LIBOR is based on actual transaction data. The CMT has remained in place as the standard HECM index.

Index Rate Resource: 1 Month Treasury Chart (Last 20 Years)

Interest Rate FAQs

What is the current interest rate for a reverse mortgage?

How do interest rates affect how much I can borrow?

How does the margin work on an adjustable-rate reverse mortgage?

When is the interest rate locked on a reverse mortgage?

Can I make monthly payments on a reverse mortgage?

Is a reverse mortgage right for me?