Reverse Mortgages in Buckeye

|

Michael G. Branson, CEO of All Reverse Mortgage, Inc., and moderator of ARLO™, has 45 years of experience in mortgage banking, with the past 20 years devoted exclusively to reverse mortgages. A Forbes Real Estate Council member, he developed the industry's first fixed-rate jumbo reverse mortgage and has been featured in Forbes, Kiplinger, the LA Times, and Yahoo Finance. (License: NMLS# 14040) |

|

Cliff Auerswald, President of All Reverse Mortgage, Inc., and co-creator of ARLO™ — the industry's first real-time reverse mortgage pricing engine — has 27 years of experience in mortgage banking, with 20+ years focused exclusively on reverse mortgages. A recognized expert in reverse mortgage technology and consumer education, he has been featured in Kiplinger, Yahoo Finance, Realtor.com, and HousingWire. (License: NMLS# 14041) |

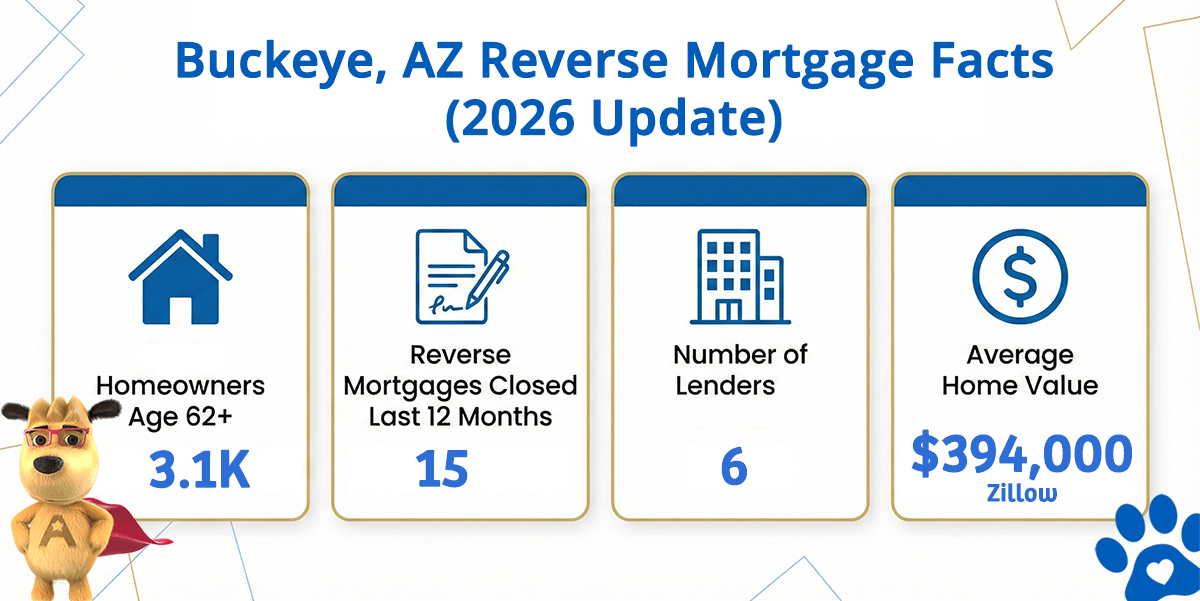

Buckeye Reverse Mortgage Market at a Glance

Buckeye Reverse Mortgage Facts (2026 Update)

| City | Homeowners Age 62+ | Reverse Mortgages Closed Last 12 Months | Lenders in Buckeye (est) | Avg. Home Value |

|---|---|---|---|---|

| Buckeye | 3,100 | 15 | 5 | ~$464,000 (Zillow) |

What the Numbers Tell Us About Reverse Mortgages in Buckeye

Buckeye represents one of Arizona’s fastest-growing communities in the West Valley, with a population exceeding 108,000 and a median home value around $464,000. For homeowners age 62 and older who’ve built equity over decades, a reverse mortgage can provide meaningful financial flexibility. At the FHA lending limit of $1,249,125, most Buckeye homes qualify for substantial borrowing capacity, making this an accessible option for retirees seeking to optimize their wealth.

The West Valley region’s appeal to active adults and families means a steady stream of homeowners entering their retirement years with significant home equity. Buckeye’s growth trajectory has attracted younger families alongside established residents, creating a diverse demographic landscape. Many are exploring ways to tap their home’s value without selling, whether to fund healthcare, supplement fixed income, or remain independent in their current homes longer.

The reverse mortgage market in Buckeye reflects this demographic shift. With several FHA-approved lenders serving the West Valley, homeowners have legitimate options to evaluate. The key is understanding whether a reverse mortgage aligns with your personal financial picture—not every option works for everyone.

Buckeye’s neighborhoods range from master-planned communities like Verrado to more established residential areas, each with distinct character and price points. Many residents relocated from other states during Arizona’s economic boom, bringing diverse financial backgrounds and retirement planning approaches. The area’s family-friendly reputation and newer infrastructure appeal to those planning to age in place, making equity-release strategies increasingly relevant for this demographic.

How a Reverse Mortgage Works for Buckeye Homeowners

A reverse mortgage is an FHA-insured loan designed exclusively for homeowners age 62 and older. Unlike a traditional mortgage, you make no monthly payments. Instead, the lender advances funds based on your home equity, and you repay the loan when you sell, move, or pass away. The HUD HECM program has provided this option to seniors since 1989, with built-in consumer protections and transparent regulation.

For Buckeye homeowners, the mechanics are straightforward: you retain full ownership of your home, maintain control of all decisions, and benefit from FHA insurance protecting against lender default. A HECM (Home Equity Conversion Mortgage) lets you choose how to receive your funds—lump sum, monthly payments, line of credit, or a combination—based on your financial situation.

Common Uses in Buckeye

- Healthcare and In-Home Care — Buckeye residents often use reverse mortgage proceeds to fund aging-in-place modifications, skilled nursing care, or medical equipment while staying in their long-time homes. See how real homeowners have used reverse mortgages to accomplish this.

- Bridging Retirement Income Gaps — Those with modest Social Security or pension income tap their home equity to supplement monthly expenses, eliminating or reducing the need for traditional employment. Understanding income requirements helps you prepare.

- Large Home Repairs and Improvements — Arizona’s heat and age mean major systems (AC, roofing, plumbing) need replacement. Reverse mortgage funds provide a non-invasive way to address these without draining savings. Learn about property requirements to ensure your home qualifies.

- Debt Consolidation and Legacy Planning — Many use the proceeds to eliminate credit cards, property taxes, or medical debt while preserving their inheritance plans. Explore non-recourse benefits to understand how this protects heirs.

Buckeye Reverse Mortgage Eligibility

| Requirement | Details |

|---|---|

| Age | At least 62 years old; see age requirements for full details on spousal considerations. |

| Home Ownership | You must own your Buckeye home outright or have substantial equity (typically 50%+). Condominiums must be FHA-approved. |

| Primary Residence | The home must be your primary residence; investment properties and second homes do not qualify. |

| Property Type | Single-family homes, townhomes, and condos (if approved) qualify. Manufactured homes have specific FHA guidelines. |

| Financial Assessment | Lenders conduct a financial assessment to ensure you can meet property tax and insurance obligations. |

| Counseling | HUD-approved counseling session (free, independent) is required before closing. |

Use our free reverse mortgage calculator to estimate how much you may qualify for based on your Buckeye home’s current value and your age.

Understanding the Costs

Reverse mortgages carry meaningful costs: origination fees, appraisal, title insurance, and FHA mortgage insurance (both upfront and annual). The total typically ranges from 2% to 5% of your loan amount. Rather than monthly payments, interest accrues and compounds until you leave the home. Learn about closing costs in detail to make an informed decision, and compare this against the pros and cons specific to your situation.

Is a Reverse Mortgage Right for You?

A reverse mortgage isn’t universally recommended—it’s a tool with clear benefits and trade-offs. If you plan to stay in your Buckeye home long-term, want to avoid monthly payments, and need liquidity, it may fit. If you’re concerned about leaving a larger estate to heirs or unsure about long-term care, a HELOC may be an alternative worth exploring. Those worried about scams should review the truth about reverse mortgages and common myths to separate fact from fiction.

HUD-Approved Direct Lender Serving Buckeye

All Reverse Mortgage Inc. is an FHA-approved HECM lender serving Buckeye and the West Valley with direct lending authority. We specialize in helping Arizona retirees understand whether a reverse mortgage fits their retirement strategy. Our team provides transparent guidance, honest cost discussions, and patient answers to your questions—no pressure, no surprises. Check our BBB profile for reviews and accreditation details. Verify our HUD lender status anytime. We also offer jumbo reverse mortgages for higher-value homes beyond the FHA limit.

All Reverse Mortgage Inc. is licensed by the Arizona Department of Financial Institutions (License #BK0934287), ensuring compliance with all state and federal regulations governing reverse mortgages.

Get a Reverse Mortgage Quote for Your Buckeye Home

Use the ARLO™ calculator for an instant quote with real-time rates — no personal information required.

Related Resources

Step-by-step explanation of the mechanics, funding options, and repayment structure for seniors considering this loan type.

Detailed breakdown of age, home equity, property type, and financial assessment criteria to determine your eligibility.

Compare the two most popular funding strategies and understand which cash distribution method aligns with your retirement goals.

Critical information on how reverse mortgage proceeds may affect your eligibility for need-based government benefits.

Statewide program data, lending limits, and HUD-approved lender resources

Phoenix metro market data and HECM activity for the greater Valley area