Reverse Mortgages in Surprise

|

Michael G. Branson, CEO of All Reverse Mortgage, Inc., and moderator of ARLO™, has 45 years of experience in mortgage banking, with the past 20 years devoted exclusively to reverse mortgages. A Forbes Real Estate Council member, he developed the industry's first fixed-rate jumbo reverse mortgage and has been featured in Forbes, Kiplinger, the LA Times, and Yahoo Finance. (License: NMLS# 14040) |

|

Cliff Auerswald, President of All Reverse Mortgage, Inc., and co-creator of ARLO™ — the industry's first real-time reverse mortgage pricing engine — has 27 years of experience in mortgage banking, with 20+ years focused exclusively on reverse mortgages. A recognized expert in reverse mortgage technology and consumer education, he has been featured in Kiplinger, Yahoo Finance, Realtor.com, and HousingWire. (License: NMLS# 14041) |

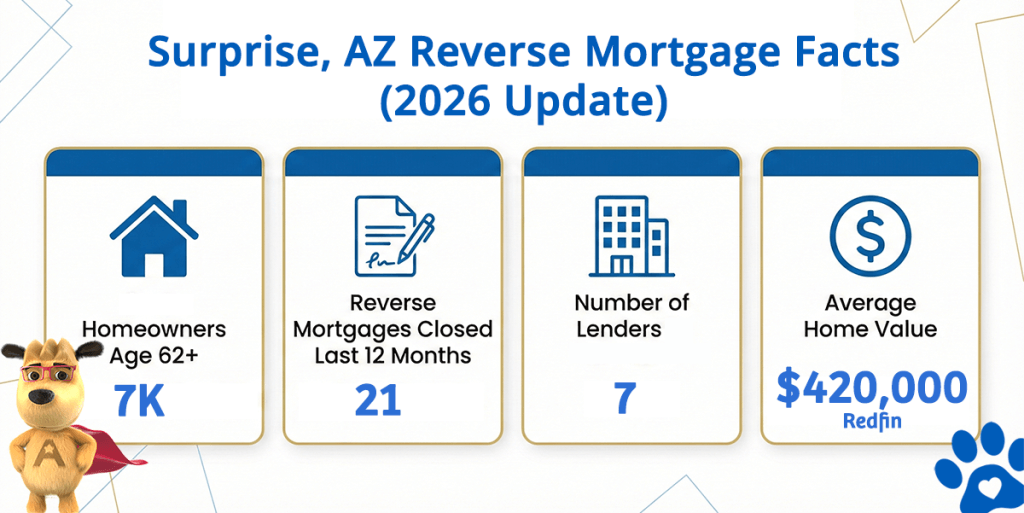

Surprise Reverse Mortgage Market at a Glance

Surprise Reverse Mortgage Facts (2026 Update)

| City | Homeowners Age 62+ | Reverse Mortgages Closed Last 12 Months | Purchase Reverse Mortgages Closed Last 12 Months | Lenders in Surprise (est) | Avg. Home Value |

|---|---|---|---|---|---|

| Surprise | ~7,000 | 21 | 7 | 7 | $420,000 |

Data sources: U.S. Census Bureau (population and demographic data), Zillow (home values), and HUD HECM database (lending volume and lender activity).

What the Numbers Tell Us About Surprise

Surprise, one of Arizona’s fastest-growing communities in the Northwest Valley, presents a strong reverse mortgage market. With a population exceeding 150,000 and a median home value of $450,612, Surprise homeowners command substantial equity positions. The $1,249,125 HECM limit translates to meaningful borrowing capacity for qualifying residents seeking to convert home equity into accessible funds.

This Northwest Valley city attracts both young families and established retirees, creating a diverse demographic base. Unlike age-restricted communities, Surprise’s broader population means reverse mortgage borrowers represent a segment within the overall market rather than the predominant demographic. This diversity creates a stable housing market with strong appreciation trends and abundant community resources.

For Surprise homeowners age 62 and older with significant equity, reverse mortgages frequently serve three core purposes: eliminating existing mortgage obligations, addressing healthcare and long-term care expenses, or establishing accessible capital reserves for retirement flexibility.

Surprise’s Growth Advantage: Rapid community development means modern infrastructure, expanding healthcare options, and abundant services—factors that support aging-in-place strategies and home equity access decisions.

How a Reverse Mortgage Works for Surprise Homeowners

A reverse mortgage allows homeowners age 62 and older to access home equity without monthly payment obligations. You remain the home’s owner and maintain full occupancy while continuing to pay property taxes, insurance, and maintenance costs. HUD’s HECM program is the federally-insured reverse mortgage available in Surprise, featuring mandatory consumer counseling and standardized underwriting protections.

The loan becomes due when you permanently leave the home, sell the property, or pass away. Heirs retain non-recourse protection—meaning if your home sells for less than the loan balance, your estate owes nothing beyond the sale proceeds.

Common Uses in Surprise

- Eliminating mortgage payments: Access proceeds to pay off existing mortgages and reduce monthly housing expenses in retirement.

- Funding healthcare needs: Finance in-home care, medical equipment, or transitions to assisted living.

- Making home improvements: Invest in accessibility modifications, safety upgrades, or aging-in-place enhancements.

- Creating retirement flexibility: Establish a flexible line of credit for ongoing expenses or discretionary spending.

Surprise Reverse Mortgage Eligibility

| Requirement | Details |

|---|---|

| Age 62 or Older | All borrowers must meet the minimum age requirement of 62 years. |

| Primary Residence | The home must be your primary residence. Investment properties, rental units, and second homes don’t qualify. |

| Substantial Home Equity | Own the home outright or carry minimal debt. The property must meet FHA standards for structural integrity and safety. |

| Financial Assessment Review | No minimum credit score required. Lenders evaluate your ability to maintain property taxes, insurance, and HOA obligations. |

| HUD-Approved Counseling | Mandatory completion of a HUD-approved counseling session is required before moving forward. |

| Property Valuation Appraisal | A professional appraisal determines current home value and verifies FHA compliance. |

Use the reverse mortgage calculator to estimate your borrowing potential based on your age, home value, and prevailing interest rates.

Understanding the Costs

Closing costs typically consist of origination fees (up to 2% of home value), appraisal and title insurance fees, recording charges, and related underwriting costs. Most lenders permit financing these costs within the loan itself, minimizing upfront out-of-pocket expenses.

Ongoing costs—property taxes, homeowners insurance, HOA fees, and routine maintenance—remain your responsibility throughout the loan term. You incur no monthly loan payments. Interest accrues on borrowed funds and is repaid when the loan terminates, whether through home sale, relocation, or inheritance by your heirs.

FHA mortgage insurance protects both you and the lender, ensuring borrowing capacity even if the lender becomes insolvent and capping repayment obligations at the home’s sale value—your heirs retain any remaining equity.

Is a Reverse Mortgage Right for You?

Carefully weigh the advantages and disadvantages before committing. A reverse mortgage works well for some households but may not suit everyone. Consider your expected length of home occupancy, your specific funding needs, your overall financial position, and your intentions regarding inheritance.

If a reverse mortgage doesn’t align with your goals, alternative home equity options exist, including HELOCs, second mortgages, and cash-out refinances. Comparing HELOC options with reverse mortgages helps clarify which solution best addresses your circumstances.

HUD-Approved Direct Lender Serving Surprise

Work exclusively with HUD-approved HECM lenders maintaining current Arizona state licensing. The Arizona Department of Financial Institutions regulates all residential mortgage lenders operating in the state. Verify your lender’s current license status (DIFI License #BK0934287 for regulated lenders) and active HUD approval before signing any documents.

When comparing lenders, obtain current interest rates from multiple providers, confirm their credibility and customer satisfaction records, and inquire whether they offer jumbo reverse mortgage products if your Surprise home value exceeds HECM program limits.

Get Your Surprise Reverse Mortgage Quote Today

Speak with a reverse mortgage specialist who understands Surprise’s dynamic real estate market and can guide you through your available options.

Related Resources

Comprehensive explanation of reverse mortgage mechanics from origination through loan resolution.

Factual corrections to widespread myths and misunderstandings about reverse mortgages.

Complete review of eligibility factors and what lenders assess during application processing.

What appraisal evaluations involve and how they influence your borrowing amount.

Arizona-specific HECM program details, limits, and comprehensive lender directory.

Phoenix metro market analysis and active lending trends.

This information is educational in nature and should not be construed as financial or legal advice. Reverse mortgage products, terms, rates, and availability vary by lender and borrower circumstances. All products are subject to credit approval. Arizona Licensed Lender DIFI License #BK0934287. For current HUD HECM information and lender verification, visit HUD’s HECM resource center.