Reverse Mortgages in Corona

|

Michael G. Branson, CEO of All Reverse Mortgage, Inc., and moderator of ARLO™, has 45 years of experience in mortgage banking, with the past 20 years devoted exclusively to reverse mortgages. A Forbes Real Estate Council member, he developed the industry's first fixed-rate jumbo reverse mortgage and has been featured in Forbes, Kiplinger, the LA Times, and Yahoo Finance. (License: NMLS# 14040) |

|

Cliff Auerswald, President of All Reverse Mortgage, Inc., and co-creator of ARLO™ — the industry's first real-time reverse mortgage pricing engine — has 27 years of experience in mortgage banking, with 20+ years focused exclusively on reverse mortgages. A recognized expert in reverse mortgage technology and consumer education, he has been featured in Kiplinger, Yahoo Finance, Realtor.com, and HousingWire. (License: NMLS# 14041) |

Corona Reverse Mortgage Market at a Glance

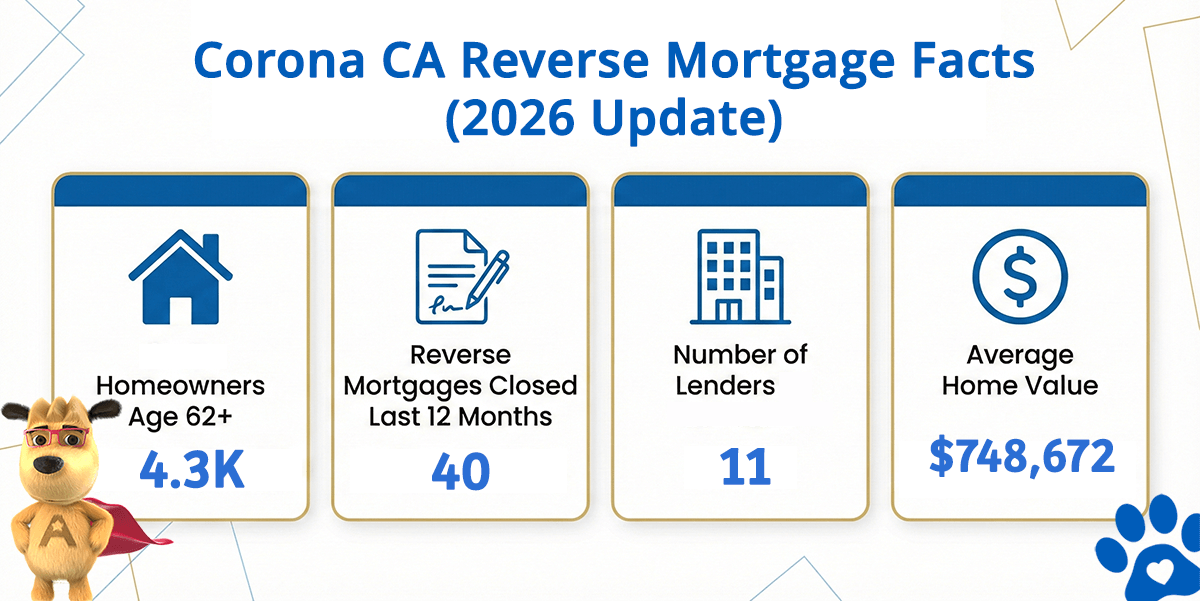

Corona Reverse Mortgage Facts (2026 Update)

| City | Homeowners Age 62+ | Reverse Mortgages Closed Last 12 Months | Lenders in Corona (est) | Avg. Home Value |

|---|---|---|---|---|

| Corona | 4,343 | 40 | 11 | $748,672 |

What the Numbers Tell Us About Reverse Mortgages in Corona

Corona is a mid-sized city in western Riverside County, California, located in a natural circular valley surrounded by the Santa Ana Mountains — a geographic feature that gave the city its original name, the “Circle City.” Situated along the 91 Freeway corridor between Orange County and the Inland Empire, Corona has experienced significant residential growth over the past several decades, attracting families and retirees drawn to its more affordable housing compared to coastal Orange County communities while maintaining reasonable access to employment, healthcare, and cultural amenities.

Corona’s housing stock includes a mix of established homes from the city’s earlier decades and newer developments built during the Inland Empire’s residential expansion. Many of the city’s senior homeowners purchased during earlier phases of this growth, building meaningful equity as the region has appreciated. For retirees on fixed incomes, managing Riverside County property taxes, insurance, and daily expenses can strain a budget — making the conversion of built-up equity into retirement income an increasingly relevant option.

Because most Corona home values fall within the federal HECM lending limit of $1,249,125, the standard FHA-insured program covers the vast majority of properties. Homeowners with higher-value properties in premium neighborhoods — particularly homes near the Corona Hills or newer luxury developments — may want to explore jumbo reverse mortgage programs, but most Corona residents will find the standard HECM provides the strongest combination of protections and available proceeds.

How a Reverse Mortgage Works for Corona Homeowners

A reverse mortgage is a loan secured by your home that allows homeowners age 62 and older to convert a portion of their equity into tax-free funds — without making monthly mortgage payments. The most common type is the Home Equity Conversion Mortgage (HECM), which is insured by the Federal Housing Administration and regulated by HUD.

The loan becomes due when the last borrower permanently leaves the home — whether through sale, relocation, or passing. Until then, borrowers retain full title and may continue living in the property as long as they meet standard obligations including property taxes, homeowners insurance, and home maintenance.

Common Uses in Corona

- Eliminating an existing mortgage payment to reduce monthly fixed costs — particularly valuable for Corona retirees on fixed incomes managing Riverside County property taxes and insurance in a market that continues to appreciate

- Establishing a line of credit that grows over time — a flexible reserve for healthcare expenses, home maintenance, or long-term care planning that grows regardless of home value fluctuations

- Supplementing Social Security or pension income to maintain quality of life in western Riverside County without selling a home that has appreciated meaningfully since purchase

- Funding home improvements or accessibility modifications — helping long-term Corona homeowners age in place safely in a community with convenient access to both Inland Empire and Orange County services

Corona Reverse Mortgage Eligibility

| Requirement | Details |

|---|---|

| Age | 62 or older (both spouses if applicable) |

| Property Type | Primary residence — single-family, townhome, FHA-approved condo, or 2–4 unit (owner-occupied) |

| Equity | Sufficient equity in the home (typically 50% or more) |

| Counseling | Must complete a HUD-approved counseling session before application |

| Financial Assessment | Demonstrated ability to maintain property taxes, insurance, and home upkeep |

For a personalized estimate based on your Corona home value, try our free reverse mortgage calculator — no personal information required.

Understanding the Costs

Reverse mortgages carry upfront and ongoing costs that borrowers should understand before proceeding. These typically include an origination fee, FHA mortgage insurance premium (MIP), third-party closing costs, and interest that accrues over the life of the loan.

Because interest compounds over time, the loan balance grows — meaning more equity is used the longer the loan remains in place. This is an important consideration for homeowners who plan to leave the property to heirs or who may need to sell in the near term. A thorough review of the pros and cons is essential to making an informed decision.

Is a Reverse Mortgage Right for You?

A reverse mortgage is not the right solution for every homeowner. It works best for those who plan to remain in their home long-term, have substantial equity, and want to improve cash flow or eliminate existing mortgage payments during retirement.

It may not be ideal if you plan to move within a few years, want to preserve maximum equity for heirs, or are uncomfortable with a rising loan balance. Understanding how a reverse mortgage works from the outset — including what happens when the last borrower leaves the home and whether refinancing makes sense down the road — helps ensure the decision aligns with your long-term goals.

HUD-approved counseling is a required step in the process, and for good reason: it provides an independent review of your financial situation and ensures you fully understand the terms before committing.

HUD-Approved Direct Lender Serving Corona

All Reverse Mortgage, Inc. (ARLO™) is a HUD-approved direct lender specializing exclusively in reverse mortgages since 2004 and maintains an A+ rating with the Better Business Bureau. We are proud to be California’s #1 Rated Reverse Mortgage Lender.

Our leadership team was involved in the introduction of the first fixed-rate jumbo reverse mortgage in 2008, giving us deep experience across both FHA-insured HECM loans and proprietary programs. While most Corona properties fall within the standard HECM limit, our familiarity with both program types ensures homeowners receive guidance tailored to their specific property value and financial goals — particularly relevant in the transition zone between Orange County and the Inland Empire.

All Reverse Mortgage, Inc. is fully licensed by the California Department of Financial Protection and Innovation (License #DFPI #4131292). We invite you to compare our reviews, rates, and closing costs with those of any other lender.

See today’s rates with no obligation — view current rates or call (951) 298-9008 to speak with a licensed specialist.

Related Resources