Reverse Mortgages in Tampa

|

Michael G. Branson, CEO of All Reverse Mortgage, Inc., and moderator of ARLO™, has 45 years of experience in mortgage banking, with the past 20 years devoted exclusively to reverse mortgages. A Forbes Real Estate Council member, he developed the industry's first fixed-rate jumbo reverse mortgage and has been featured in Forbes, Kiplinger, the LA Times, and Yahoo Finance. (License: NMLS# 14040) |

|

Cliff Auerswald, President of All Reverse Mortgage, Inc., and co-creator of ARLO™ — the industry's first real-time reverse mortgage pricing engine — has 27 years of experience in mortgage banking, with 20+ years focused exclusively on reverse mortgages. A recognized expert in reverse mortgage technology and consumer education, he has been featured in Kiplinger, Yahoo Finance, Realtor.com, and HousingWire. (License: NMLS# 14041) |

Tampa’s Reverse Mortgage Market and Opportunity

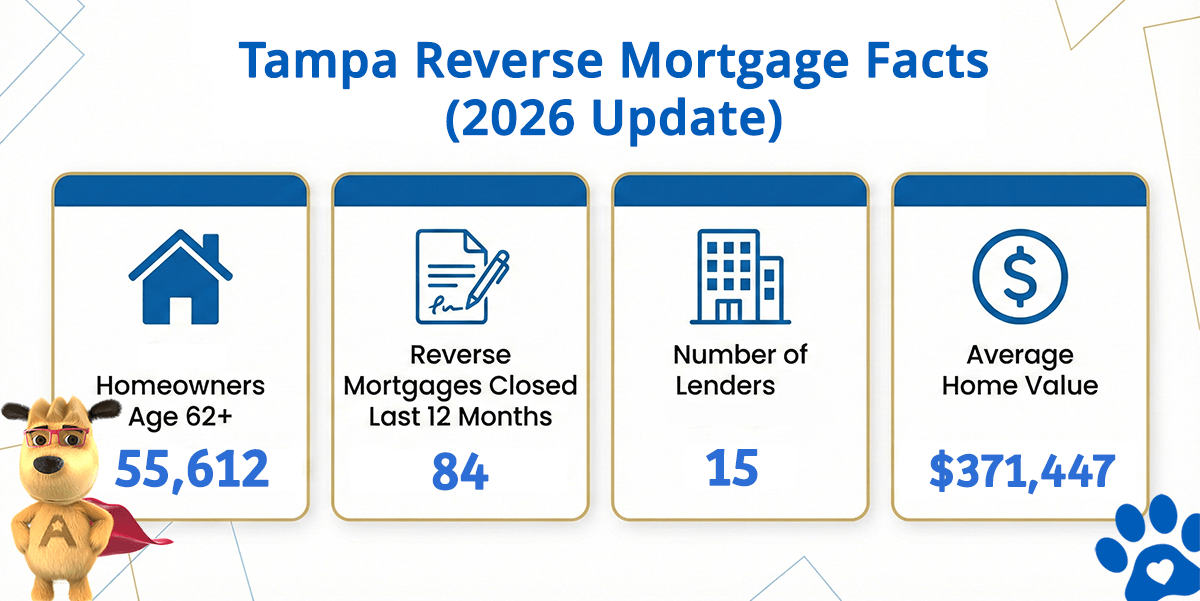

Tampa Reverse Mortgage Facts (2026 Update)

| City | Homeowners Age 62+ | Reverse Mortgages Closed Last 12 Months | Active Lenders | Avg. Home Value |

|---|---|---|---|---|

| Tampa | 55,612 | 84 | 15 | $371,447 |

Why Tampa Stands Out for Reverse Mortgages

Tampa is Florida’s industrial and commercial powerhouse—not a retirement destination by design, but rather a major metropolitan economy where career-focused professionals happened to build lives and raise families, then age in place. The city’s 55,612 homeowners age 62+ represent the state’s single largest concentration of older residents, many the product of stable, long-term employment in military, healthcare, government, finance, and industrial sectors. Home values average $371,447, accessible enough that most qualify within the $1,249,125 FHA lending limit. With 84 HECM loans executed in the past year and 15 active lenders, Tampa’s reverse mortgage market reflects the sheer volume of equity-rich homeowners seeking strategic access to their accumulated assets.

Tampa’s neighborhoods each tell stories of waves of economic expansion. South Tampa’s Hyde Park preserves early-1900s grandeur with substantial equity homes. Ballast Point and Davis Islands offer waterfront premium properties. Central Tampa’s historic Ybor City district appeals to cultural retirees and walkability seekers. North Tampa’s Carrollwood and Citrus Park represent suburban expansion zones with diverse price points and equity positions. East and West Tampa feature older, affordable stock that built long-term equity for working-class residents. Each neighborhood represents different household profiles with distinct financial circumstances, all accessing equity through reverse mortgages for different purposes.

Tampa’s economy is fundamentally diversified and stable. MacDill Air Force Base generates military employment and attracts defense contractors, retirees, and technical specialists. USF Health, Bayfront Health, and specialty hospitals employ thousands in healthcare roles, attracting long-career professionals. Finance and business services maintain regional headquarters. Technology has expanded rapidly with major corporate offices. Retail, hospitality, and tourism support service employment. This occupational diversity means Tampa’s reverse mortgage borrowers bring varied backgrounds—military careers, healthcare professions, finance leadership, government service, small business ownership—all unified by decades of equity-building employment. They’re accessing that equity through financial assessment processes that evaluate their capacity to maintain homes while unlocking proceeds for travel, healthcare, family support, and emergency reserves without forced sale.

How a Reverse Mortgage Works for Tampa Homeowners

A reverse mortgage is a loan secured by your home that allows homeowners age 62 and older to convert a portion of their equity into usable funds. The most common type is the Home Equity Conversion Mortgage (HECM), which is insured by the Federal Housing Administration and regulated by HUD.

With a HECM, you retain full ownership of your home. No monthly mortgage payments are required as long as you continue living in the property, maintain it, and stay current on property taxes and homeowners insurance. The loan balance is repaid when you sell, move out permanently, or pass away — and FHA insurance guarantees you will never owe more than the home is worth.

Common Tampa Reverse Mortgage Uses

- Establishing emergency reserves and healthcare funding for aging-related care needs and medical expenses

- Using a credit line option to maintain hurricane recovery liquidity and handle unexpected property repairs

- Supporting multi-generational family needs and military-connected relatives in government service

- Funding family reunions and travel without selling the home or reducing fixed retirement income

Tampa Reverse Mortgage Eligibility

| Requirement | Details |

|---|---|

| Age | 62 or older (at least one borrower) |

| Property | Primary residence — single-family home, townhome, condo, or approved dwelling |

| Equity | Sufficient equity in the home (typically 50% or more) |

| Counseling | HUD-mandated counseling with an independent, FHA-approved advisor mandatory before submission |

| Financial Assessment | Lender evaluates income, credit history, and ability to maintain property obligations |

Tampa homeowners: see your estimated proceeds in about 30 seconds — our calculator uses your home value, age, and current rates with no personal information required.

Managing Program Costs

The program incorporates origination fees, FHA insurance premiums, third-party closing charges, and accruing interest. Structurally parallel to traditional refinancing, but with key timing advantages: most costs can be financed into the loan balance instead of paid from cash on hand.

For comprehensive breakdown of expenses, review our guide on closing fee details and financial assessment processes to understand how lenders evaluate your circumstances.

Evaluating Whether a Reverse Mortgage Suits Your Needs

Reverse mortgages benefit homeowners planning to stay long-term who want to boost monthly cash flow, manage healthcare expenses, or build financial cushions without forced home sale. They don’t suit those expecting to relocate soon or treating maximum heir inheritance as the overriding financial priority.

Get full details by reading about what a reverse mortgage is and isn’t and exploring options for reverse mortgage refinance should your circumstances shift.

HUD-Approved Direct Lender Serving Tampa

All Reverse Mortgage, Inc. (ARLO) is a HUD-approved direct lender — not a broker or lead generator. We originate, process, and fund reverse mortgages in-house, giving Tampa homeowners a single point of contact from first conversation through closing.

You can verify our credentials through the HUD lender lookup tool or review our BBB profile, which reflects more than two decades of client feedback. For homeowners whose property value exceeds FHA limits, we also offer jumbo reverse mortgage programs with no mortgage insurance requirement.

All Reverse Mortgage, Inc. is fully licensed by the Florida Office of Financial Regulation (License #MLD874), ensuring that you receive expert guidance every step of the way.

Get a Reverse Mortgage Quote for Your Tampa Home

The ARLO™ calculator delivers personalized quotes with current current reverse mortgage rates — completely private, no data sharing required.

Related Resources

Pinellas County market information for the greater Tampa Bay area