Reverse Mortgages in Austin

|

Michael G. Branson, CEO of All Reverse Mortgage, Inc., and moderator of ARLO™, has 45 years of experience in mortgage banking, with the past 20 years devoted exclusively to reverse mortgages. A Forbes Real Estate Council member, he developed the industry's first fixed-rate jumbo reverse mortgage and has been featured in Forbes, Kiplinger, the LA Times, and Yahoo Finance. (License: NMLS# 14040) |

|

Cliff Auerswald, President of All Reverse Mortgage, Inc., and co-creator of ARLO™ — the industry's first real-time reverse mortgage pricing engine — has 27 years of experience in mortgage banking, with 20+ years focused exclusively on reverse mortgages. A recognized expert in reverse mortgage technology and consumer education, he has been featured in Kiplinger, Yahoo Finance, Realtor.com, and HousingWire. (License: NMLS# 14041) |

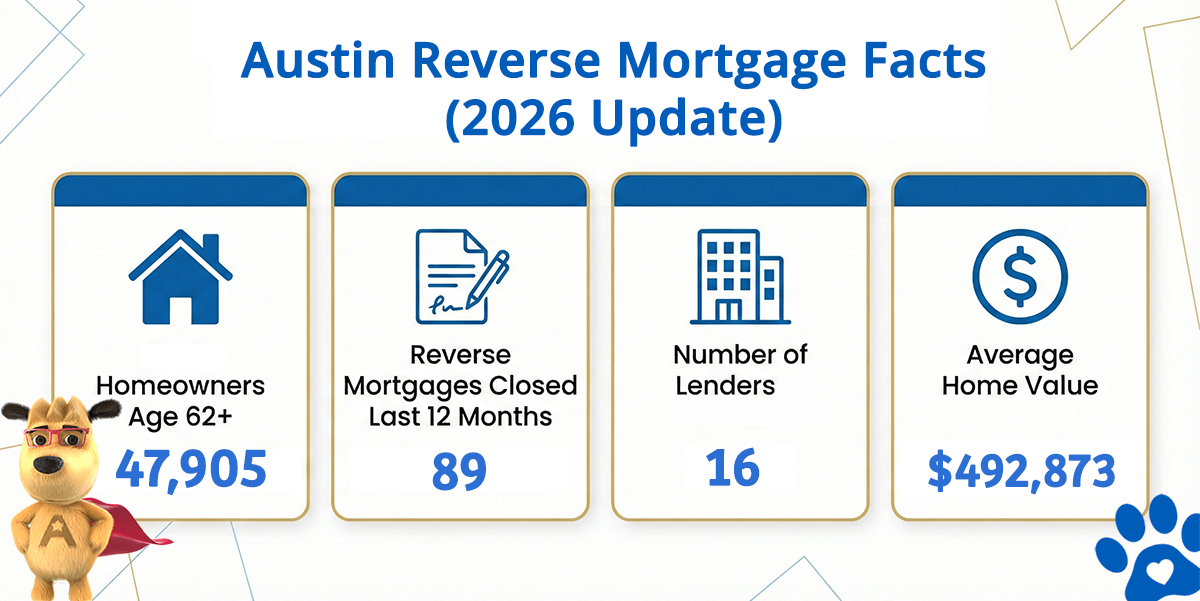

Austin Reverse Mortgage Market at a Glance

Austin Reverse Mortgage Facts (2026 Update)

| City | Homeowners Age 62+ | Reverse Mortgages Closed Last 12 Months | Lenders in Austin (est) | Avg. Home Value |

|---|---|---|---|---|

| Austin | 54,675 | 228 | 13 | $625,705 |

What the Numbers Tell Us About Reverse Mortgages in Austin

Austin is Texas’s fastest-growing major metropolitan area, with just over one million residents and a median age that skews younger due to its tech-driven economy. However, the city is home to nearly 55,000 owner-occupied households headed by residents age 62 and older, many of whom built substantial equity in their homes over decades of ownership. The average home value in Austin has climbed to $625,705, reflecting the city’s status as a coveted destination for entrepreneurs, remote workers, and retirees alike. This robust housing market, combined with the FHA lending limit of $1,249,125, means that many Austin homeowners, particularly those in central, northwest, and southwest neighborhoods, have homes that exceed FHA caps and may benefit from proprietary reverse mortgage programs.

Austin’s neighborhoods tell the story of a city reinventing itself while preserving character. South Congress (SoCo) and Hyde Park blend historic charm with rising values, attracting educated professionals and empty-nesters. Mueller, a master-planned mixed-use district, appeals to downsizers seeking modern urban living. Tarrytown and Barton Hills remain exclusive residential enclaves with custom homes built in the 1950s through 1980s, while Travis Heights offers established mid-century character homes. Circle C Ranch and Steiner Ranch are newer suburban communities with homes constructed in the 2000s and beyond, appealing to younger retirees. This diverse housing stock means reverse mortgage borrowers in Austin range from those in modest 1960s ranch homes to owners of premium properties that command premium prices.

Austin’s economy is uniquely positioned to build long-term home equity. Dell Technologies, headquartered in Round Rock just outside the city, anchors a sprawling tech corridor that includes major offices for Apple, Samsung, Oracle, and Google. The University of Texas contributes thousands of stable, long-career jobs in education and research, while Tesla’s Gigafactory expansion nearby signals continued tech investment. State government agencies and the Texas Legislature employ thousands more. Unlike cities tied to single industries, Austin’s diversified employer base has created multiple waves of wealth-building for homeowners. Many are retiring after 30+ years in tech, government, or education sectors, with fully paid-off homes or minimal remaining mortgages. This explains the strong reverse mortgage activity: borrowers want to access their equity while staying put in a community they love.

How a Reverse Mortgage Works for Austin Homeowners

A reverse mortgage is a loan secured by your home that allows homeowners age 62 and older to convert a portion of their equity into usable funds. The most common type is the Home Equity Conversion Mortgage (HECM), which is insured by the Federal Housing Administration and regulated by HUD.

With a HECM, you retain full ownership of your home. No monthly mortgage payments are required as long as you continue living in the property, maintain it, and stay current on property taxes and homeowners insurance. The loan balance is repaid when you sell, move out permanently, or pass away, and FHA insurance guarantees you will never owe more than the home is worth.

Common Uses in Austin

- Eliminating an existing mortgage payment — Many Austin homeowners refinanced or purchased homes during the 2010s tech boom and still carry 15-20 year mortgages; a reverse mortgage at age 62+ can eliminate monthly payments and free up cash flow for travel, hobbies, and grandchildren.

- Supplementing retirement income — A growing line of credit can serve as inflation protection for Austin retirees whose fixed pensions and Social Security may not keep pace with the city’s rising cost of living, healthcare, and property taxes.

- Funding multigenerational family time — Austin attracts adult children back to the region for tech jobs; retirees use reverse mortgage proceeds to host family gatherings, help with grandchildren’s education, or renovate homes to accommodate visiting relatives and longer-term stays.

- Accessing equity above FHA limits — For Austin homeowners with higher-value properties above the HECM cap, proprietary reverse mortgage programs allow access to more equity without the FHA ceiling.

Austin Reverse Mortgage Eligibility

| Requirement | Details |

|---|---|

| Age | 62 or older (at least one borrower) |

| Property | Primary residence — single-family, condo, or manufactured home on permanent foundation |

| Equity | Sufficient equity in the home (typically 50% or more) |

| Counseling | HUD-approved reverse mortgage counseling session required before application |

| Financial Assessment | Lender evaluates income, credit history, and ability to maintain property obligations |

Use our free reverse mortgage calculator to estimate how much you may qualify for based on your Austin home’s current value and your age.

Understanding the Costs

Reverse mortgage costs include an origination fee, FHA mortgage insurance premium, third-party closing fees, and interest that accrues over the life of the loan. These are comparable to a traditional refinance in structure but differ in timing, as most costs can be financed into the loan rather than paid upfront.

For a full breakdown of what to expect, review our guide to reverse mortgage closing costs. Borrowers should also weigh the benefits against the long-term impact on home equity, which we cover in our pros and cons overview.

Is a Reverse Mortgage Right for You?

A reverse mortgage works best for homeowners who plan to stay in their home long-term and want to improve monthly cash flow or create a financial safety net without selling. It is not ideal for those planning to move within a few years or who need to preserve every dollar of equity for heirs.

Our guide on how reverse mortgages work explains the full process from application to funding.

HUD-Approved Direct Lender Serving Austin

All Reverse Mortgage, Inc. (ARLO) is a HUD-approved direct lender, not a broker or lead generator. We originate, process, and fund reverse mortgages in-house, giving Austin homeowners a single point of contact from first conversation through closing.

You can verify our credentials through the HUD lender lookup tool or review our BBB profile, which reflects more than two decades of client feedback. For homeowners whose property value exceeds FHA limits, we also offer jumbo reverse mortgage programs with no mortgage insurance requirement.

All Reverse Mortgage, Inc. is fully licensed by the Texas Department of Savings & Mortgage Lending (License #84280), ensuring that you receive expert guidance every step of the way.

Get a Reverse Mortgage Quote for Your Austin Home

Use the ARLO calculator for an instant quote with real-time rates — no personal information required.

Related Resources