Reverse Mortgages in Georgetown

|

Michael G. Branson, CEO of All Reverse Mortgage, Inc., and moderator of ARLO™, has 45 years of experience in mortgage banking, with the past 20 years devoted exclusively to reverse mortgages. A Forbes Real Estate Council member, he developed the industry's first fixed-rate jumbo reverse mortgage and has been featured in Forbes, Kiplinger, the LA Times, and Yahoo Finance. (License: NMLS# 14040) |

|

Cliff Auerswald, President of All Reverse Mortgage, Inc., and co-creator of ARLO™ — the industry's first real-time reverse mortgage pricing engine — has 27 years of experience in mortgage banking, with 20+ years focused exclusively on reverse mortgages. A recognized expert in reverse mortgage technology and consumer education, he has been featured in Kiplinger, Yahoo Finance, Realtor.com, and HousingWire. (License: NMLS# 14041) |

Georgetown’s Active Adult Reverse Mortgage Market

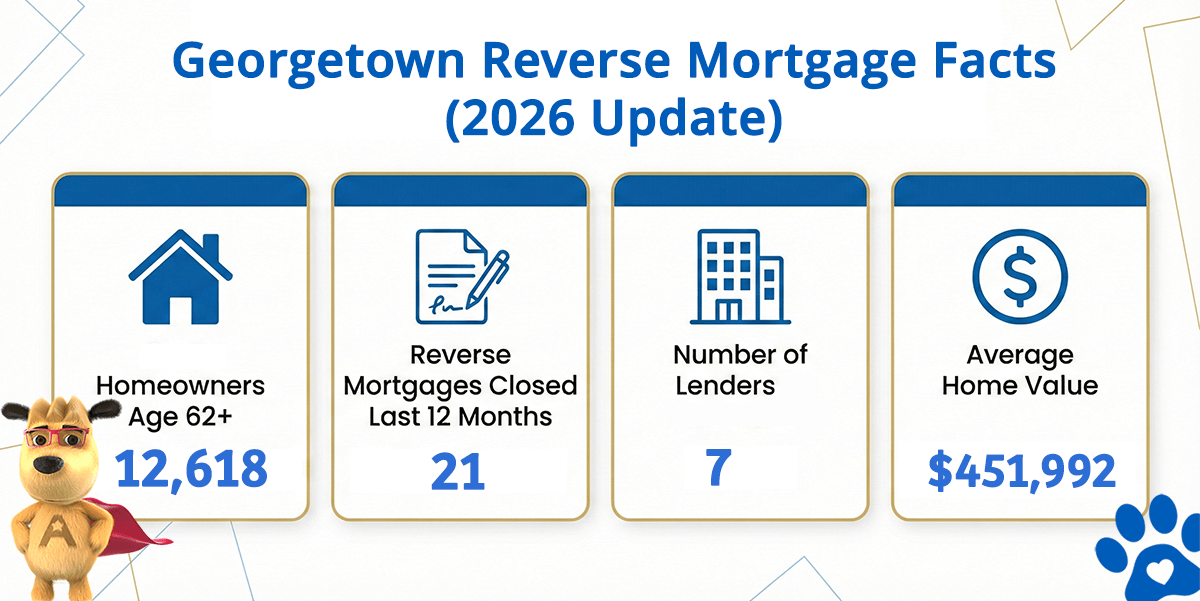

Georgetown Reverse Mortgage Facts (2026 Update)

| City | Homeowners Age 62+ | Reverse Mortgages Closed Last 12 Months | Lenders in Georgetown (est) | Avg. Home Value |

|---|---|---|---|---|

| Georgetown | 12,618 | 21 | 7 | $451,992 |

Georgetown: Texas’s Fastest-Growing Retirement Destination

Georgetown has emerged as one of Central Texas’s most dynamic and appealing communities for active adults and retirees. The city’s explosive growth over the past decade reflects a powerful combination of affordable housing, excellent quality of life, and intentional community planning that attracts 55+ households from across the nation. Unlike typical Texas cities where reverse mortgage populations are scattered across decades-old neighborhoods, Georgetown’s market is increasingly anchored by purpose-built active adult communities that bring together thousands of homeowners age 55 and older.

The crown jewel of Georgetown’s active adult landscape is Sun City by Del Webb, a master-planned community that has become one of Texas’s premier 55+ destinations. Sun City brings together over 2,100 homes, extensive recreation facilities, golf courses, resort-style amenities, and a vibrant social calendar designed around the interests of active retirees. Residents of Sun City come from across the United States—former Californians, New Yorkers, and retirees from high-cost markets seeking to stretch their retirement dollars while enjoying a planned community built specifically for their lifestyle. This concentration of affluent, relocating retirees distinguishes Georgetown from Texas cities where reverse mortgage borrowers are primarily long-term, multi-generational residents.

Beyond Sun City, Georgetown proper attracts retirees seeking small-town charm combined with proximity to Austin’s amenities. Williamson County’s growing economy, anchored by technology companies expanding north from Austin, has attracted younger professionals who are purchasing homes and building equity—a demographic wave that will age into reverse mortgage eligibility over the coming decade. The city’s downtown revival, excellent schools (even if most residents have empty nests), and strong property appreciation make Georgetown an attractive relocation destination for empty-nesters and early retirees from higher-cost states.

Home values in Georgetown remain accessible compared to Austin and the broader Austin metro, allowing retirees relocating from expensive states to downsize, reduce their monthly housing costs, and still purchase quality homes in planned communities. This market dynamic creates unique reverse mortgage opportunities: borrowers who have sold high-value properties in California, Colorado, or the Northeast and purchased Georgetown homes for cash or with minimal financing, and who now have substantial equity available through reverse mortgages if cash flow needs arise.

How Reverse Mortgages Work for Georgetown Homeowners

A reverse mortgage enables homeowners age 62 and older to access home equity without monthly mortgage payments—an ideal structure for Georgetown retirees living on fixed Social Security and pensions who want to manage unexpected expenses or fund travel and family activities without depleting investment portfolios.

With a reverse mortgage, you maintain ownership and can live in your home as long as you choose. Funds come to you—as a lump sum, regular monthly advances, a line of credit that grows over time, or a combination. You decide when and how to draw on the equity. Repayment occurs when you sell, move out permanently, or pass away. FHA insurance protects you from ever owing more than the home sells for—a valuable safety net.

Common Uses in Georgetown

- Funding retirement lifestyle activities and travel — Georgetown’s Sun City residents relocate specifically for active retirement; reverse mortgage proceeds enable extended family visits, RV travel, golf memberships, and hobby pursuits without impacting retirement savings.

- Managing the transition from working life to full retirement — Retirees relocating to Georgetown often arrive at traditional retirement age; a reverse mortgage provides income bridging while transitioning from paychecks to Social Security and pension income.

- Using HECM for Purchase to buy into active adult communities — HECM for Purchase lets you buy in Georgetown without monthly payments, allowing borrowers to relocate to Sun City or another community without the burden of a traditional mortgage payment during early retirement years.

- Simplifying finances while supporting adult children or grandchildren — Retirees relocating to Georgetown often wish to help fund grandchildren’s education, weddings, or other milestone events; reverse mortgage proceeds provide this flexibility without selling the primary residence.

Georgetown Reverse Mortgage Eligibility

| Requirement | Details |

|---|---|

| Age | 62 or older (at least one borrower must be 62+) |

| Home Type | Primary residence (single-family, condo, townhouse, or manufactured home on permanent foundation) |

| Home Value | Home value must fall within the FHA lending limit of $1,249,125 for FHA-insured loans |

| Equity Requirement | Sufficient home equity (typically 50% or more of current market value) |

| HUD Counseling | Required HUD counseling from an approved agency before application |

Calculate your estimate using your Georgetown home’s current value — it takes about 30 seconds and requires no contact information.

Understanding Georgetown Reverse Mortgage Costs

Reverse mortgages carry costs similar to traditional refinances: origination fees, FHA mortgage insurance premiums (MIP), third-party closing fees (appraisal, title, recording), and accruing interest. The key advantage is financing most costs into the loan itself rather than paying upfront—a feature that preserves your liquidity and allows you to maintain the financial flexibility retirement demands.

For complete details, review our guides on understanding reverse mortgage costs and benefits and considerations to ensure you understand the full financial picture before committing.

Is a Reverse Mortgage Right for Your Georgetown Home?

A reverse mortgage makes excellent sense if you relocated to Georgetown for active retirement and plan to remain in your community for many years. It works well for accessing equity to fund travel, grandchildren support, or unexpected expenses while preserving your primary residence. It may be less suitable if you anticipate moving again within 5 years or if maximizing equity for heirs is your primary financial goal.

Learn more by exploring our resources on reverse mortgage rules and refinancing options if your situation changes — important information for Georgetown retirees managing long-term financial plans.

Serving Georgetown’s Active Adult Communities

All Reverse Mortgage, Inc. (ARLO) specializes in serving retirement and active adult communities across Central Texas. We understand the unique circumstances of 55+ communities and retirees relocating to Georgetown, and we structure reverse mortgages to fit these specific situations. Our team works with retirees daily and understands the income, lifestyle, and legacy goals that matter to Georgetown homeowners.

Verify our credentials with the HUD lender lookup tool and review our BBB profile for client feedback spanning two decades. We are fully licensed by the Texas Department of Savings & Mortgage Lending (License #84280).

Get Your Georgetown Reverse Mortgage Estimate

Call our team today to discuss how a reverse mortgage can enhance your Georgetown retirement. We’ll show you today’s reverse mortgage rates.

Related Resources

HECM for Purchase lets you buy in Georgetown without monthly payments