See How It Works With Your Numbers

How Reverse Mortgages Work in 2026 | Complete HECM Guide

|

Michael G. Branson, CEO of All Reverse Mortgage, Inc., and moderator of ARLO™, has 45 years of experience in mortgage banking, with the past 20 years devoted exclusively to reverse mortgages. A Forbes Real Estate Council member, he developed the industry's first fixed-rate jumbo reverse mortgage and has been featured in Forbes, Kiplinger, the LA Times, and Yahoo Finance. (License: NMLS# 14040) |

|

Cliff Auerswald, President of All Reverse Mortgage, Inc., and co-creator of ARLO™ — the industry's first real-time reverse mortgage pricing engine — has 27 years of experience in mortgage banking, with 20+ years focused exclusively on reverse mortgages. A recognized expert in reverse mortgage technology and consumer education, he has been featured in Kiplinger, Yahoo Finance, Realtor.com, and HousingWire. (License: NMLS# 14041) |

Michael G. Branson

Michael G. Branson Cliff Auerswald

Cliff Auerswald

For more than 20 years, I’ve helped older homeowners understand and use reverse mortgages safely. At All Reverse Mortgage, Inc., we focus on one loan and one purpose — helping you use the equity you’ve built to support your retirement with clear numbers and no pressure.

This guide walks you through the essentials in plain English: what a reverse mortgage is, how it works, what it costs, the different ways you can receive the funds, and what it means for your heirs. My goal is simple — to give you the facts so you can decide whether this loan fits the way you want to live in retirement.

What Is a Reverse Mortgage?

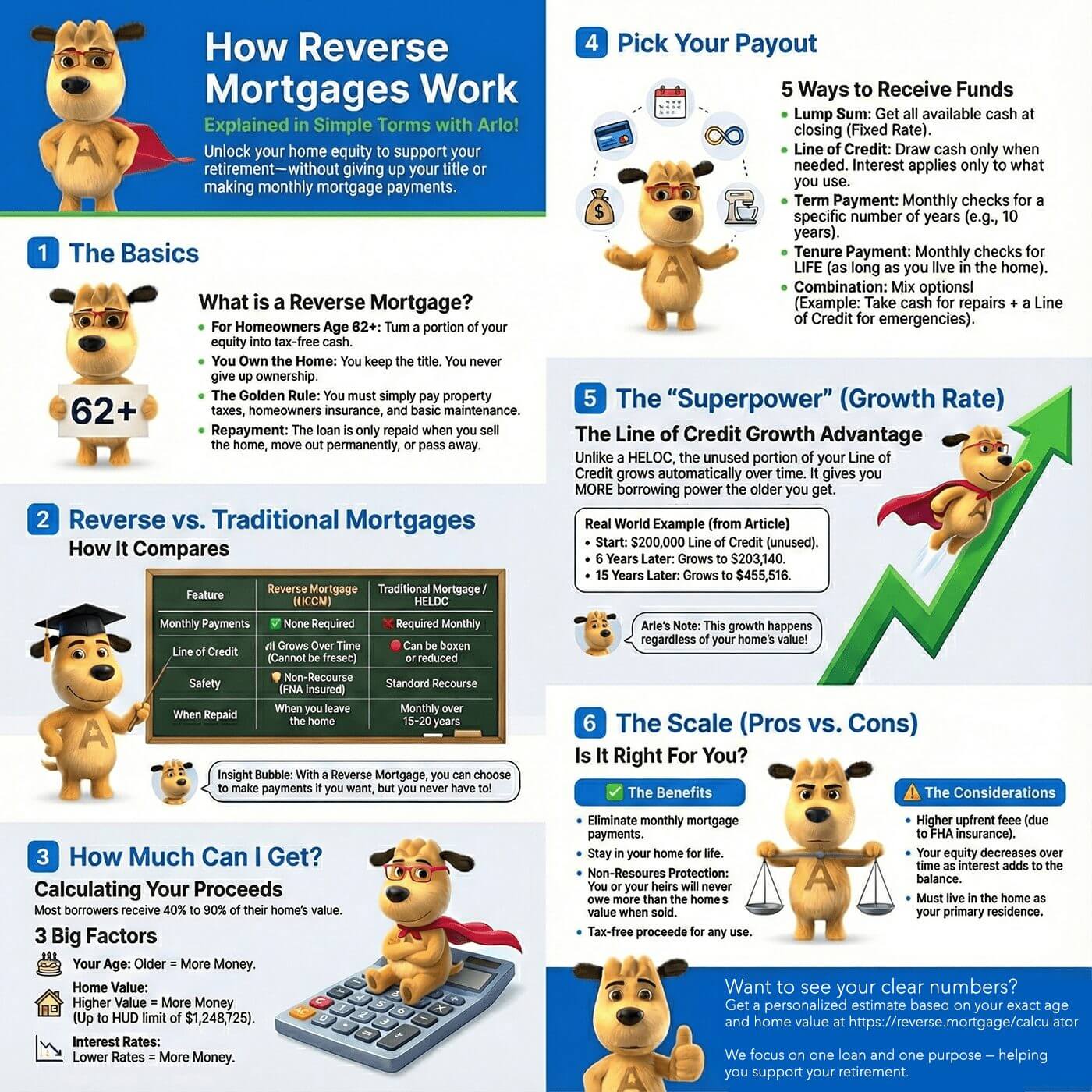

A reverse mortgage is a federally insured home loan designed exclusively for homeowners age 62 or older. It allows you to convert a portion of the equity you’ve built in your home into tax-free loan proceeds — without selling your home, giving up the title, or taking on a required monthly mortgage payment.

The most common type is the Home Equity Conversion Mortgage (HECM), which is insured by the Federal Housing Administration (FHA) and regulated by the U.S. Department of Housing and Urban Development (HUD). HECMs account for the vast majority of reverse mortgages originated today.

As the homeowner, you retain full legal title to the property. The lender places a lien on the home — the same way a traditional mortgage works — but does not take ownership. The loan is repaid when the last surviving borrower (or eligible non-borrowing spouse) sells the home, moves out permanently, or passes away. Until that time, you can live in the home for life, provided you continue to meet three ongoing obligations: paying your property taxes, maintaining homeowners insurance, and keeping the property in reasonable condition.

Eligible property types include: single-family homes, HUD-approved condominiums, FHA-approved manufactured homes (built after June 1976 and meeting HUD standards), and 2–4 unit properties where the borrower occupies one unit as a primary residence.

How Does a Reverse Mortgage Work?

A reverse mortgage works by letting you access part of your home equity without taking on a required monthly mortgage payment. Instead of paying the lender each month, the lender gives you funds — as a lump sum, monthly payments, a line of credit you can tap when needed, or a combination of these choices.

Interest and FHA mortgage insurance charges are added to the loan balance over time rather than being billed to you monthly. This means the amount you owe gradually increases while your remaining equity may decrease, unless property appreciation offsets the balance growth.

The loan becomes due when you no longer live in the home as your primary residence, or if property taxes, homeowners insurance, or basic maintenance requirements are not kept current. As long as those obligations are met, you remain the owner of your home and can live there for life.

The HECM Process: From Application to Funding

Before a HECM can be originated, every borrower must complete a counseling session with a HUD-approved counselor. This is a federal requirement — not optional — and is designed to make sure you fully understand how the loan works, what your obligations are, and what alternatives may be available. The counselor is independent from the lender, and the session can be done in person or by phone. Once counseling is complete, you receive a certificate that your lender needs before your application can move forward.

The general timeline from application to funding typically takes 30 to 45 days, though this can vary depending on the appraisal, title work, and individual circumstances.

Expert Insight from Michael Branson, CEO: “The more money you borrow at the beginning of the loan, the faster the interest will accrue on the larger balance. If you are looking to pass on the largest asset to your heirs, you can significantly reduce the amount of interest that accrues by borrowing smaller amounts and as late in the loan cycle as is comfortable or necessary.”

Reverse Mortgage vs. Traditional Mortgages and Home Equity Loans

When you think about borrowing against your home, you’re usually choosing between a traditional mortgage or a home equity line of credit. A reverse mortgage is fundamentally different. It was built specifically for homeowners age 62 or older and eliminates the requirement for monthly mortgage payments, making it a better fit for retirees living on a fixed income.

With a traditional mortgage or a HELOC, you must make monthly payments or risk default. A HELOC can also be frozen, reduced, or called due by the lender at any time based on market conditions or changes to your financial situation. A reverse mortgage line of credit, by contrast, cannot be frozen or reduced once established — and repayment isn’t required as long as you live in the home and meet your loan obligations.

Here’s How They Compare:

| Feature | Reverse Mortgage (HECM) | Traditional Mortgage | Home Equity Loan / HELOC |

|---|---|---|---|

| Age Requirement | 62 or older | 18 or older | 18 or older |

| Monthly Payments | Not required | Required every month | Required every month |

| How You Receive Funds | Lump sum, monthly payments, line of credit, or a combination | Lump sum at closing | Lump sum (loan) or a revolving line of credit (HELOC) |

| When the Loan Is Repaid | When you sell, move out permanently, or pass away | Paid monthly over 15-30 years | Paid monthly over a set term |

| Impact on Home Equity | Balance increases as interest adds to the loan (unless you make voluntary payments) | Balance decreases as payments are made | Balance decreases as payments are made |

| Borrower Protections | FHA-insured, non-recourse: you never owe more than the home’s value | Standard protections only | Standard protections only |

Key takeaway: With a reverse mortgage, you stay in your home and can choose whether or not to make payments. Unlike a HELOC or cash-out refinance, repayment isn’t required until you move out, sell, or pass away. That flexibility is why many older homeowners use a reverse mortgage to supplement retirement income while preserving monthly cash flow.

Expert Insight from Michael Branson, CEO: “If your goal is flexibility, the reverse mortgage line of credit is unmatched. It grows over time and gives you access to more funds in the future, unlike a HELOC that can be frozen or reduced by the bank.”

How Much You Can Get From a Reverse Mortgage

The amount you can receive from a reverse mortgage typically falls between 40% and 60% of your home’s appraised value. The exact figure depends on three things: your age, your home’s value (up to HUD’s lending limit of $1,249,125), and the interest rate at the time you apply. Older borrowers qualify for a higher percentage because the expected loan duration is shorter, and lower interest rates also increase the available amount because less of the equity needs to be reserved to cover future interest accrual.

HUD publishes Principal Limit Factor (PLF) tables that determine the exact percentage available at every age and interest rate combination. These tables are based on actuarial data and are updated periodically.

Factors That Determine Your Loan Amount:

- Age of the youngest borrower or eligible non-borrowing spouse — older borrowers qualify for a larger percentage of their home’s value.

- Your home’s appraised value or the HUD lending limit, whichever is lower — this is called the Maximum Claim Amount and sets the ceiling for your calculation.

- Current interest rates — the Expected Rate (for adjustable-rate HECMs) or the Note Rate (for fixed-rate HECMs) is used to look up your Principal Limit Factor.

If you’d like a personalized estimate based on your exact age, home value, and today’s rates, you can use our reverse mortgage calculator for an instant, no-obligation calculation.

How Age Affects Your Principal Limit

Your Principal Limit is the maximum amount you can access through a reverse mortgage for your specific situation. It is calculated using the age of the youngest borrower (or eligible non-borrowing spouse), the lesser of your home’s appraised value or HUD’s lending limit, and current interest rates.

Here’s why each factor matters:

- Age: The older you are, the more you receive. HUD’s actuarial tables assign a higher loan-to-value ratio at every age increment because the expected loan duration is shorter.

- Home value: Higher property values mean more available equity, up to HUD’s lending limit of $1,249,125.

- Interest rates: Lower rates mean less equity is reserved for future interest accrual, leaving more funds available to you upfront.

An 85-year-old borrower will qualify for a meaningfully higher percentage than a 62-year-old borrower at the same interest rate — the difference can be 15 to 20 percentage points or more.

Key Point: When a homeowner has a reverse mortgage, they can live in their home for the rest of their life without any monthly mortgage payment being owed, as long as they occupy the home as their primary residence, pay the property taxes, maintain homeowners insurance, and keep up the property.

Pro Tip: If you are within 6 months of your next birthday at the time of loan closing, the calculator will round your age up to the next year. This matters because you are eligible for a slightly higher loan-to-value at every age increment — even one year can make a measurable difference in your available funds.

How You Can Receive the Funds

One of the strongest advantages of a reverse mortgage is the flexibility in how you receive your proceeds. Unlike other loan products that offer a single disbursement method, the HECM program gives you five distinct options:

- Lump Sum: A single, one-time disbursement at closing of all available proceeds. This option is only available with the fixed-rate HECM, and the full draw amount is determined at closing.

- Line of Credit: Draw funds as needed over time. Any unused portion is subject to a growth rate that increases your available borrowing capacity — a feature unique to reverse mortgages. This is the most popular option and is only available with the adjustable-rate HECM.

- Term Payment: Receive equal monthly disbursements for a set number of months — for example, $1,500 per month for 10 years. Available with the adjustable-rate HECM.

- Tenure Payment: Receive equal monthly disbursements for as long as you live in the home and keep the loan in good standing. This option provides guaranteed income for life. Available with the adjustable-rate HECM.

- Combination: Mix two or more of the above options to match your specific financial goals. For example, take a partial lump sum for immediate needs and place the rest in a line of credit for future access.

Scenario Example:

A borrower, aged 66, owns a $500,000 home that is free and clear (no existing mortgage). At current interest rates, they could structure the following combination:

- Take an $80,000 initial draw to complete a full home renovation — updating the kitchen, bathrooms, and accessibility features for aging in place.

- Set up a $1,000 per month term payment for 4 years to supplement income until age 70, when they begin collecting Social Security at a higher monthly benefit amount.

- Leave the remaining ~$60,000 in a line of credit for emergencies. These funds are subject to the growth rate, so the available balance increases each month even if no withdrawals are made.

This kind of strategic planning — using a reverse mortgage to delay Social Security — is one of the ways experienced financial advisors help clients maximize their total retirement income. The combination approach allows the borrower to address an immediate need, create a short-term income stream, and build a growing financial safety net, all from a single loan.

Want to see how each payout option works? Explore real examples and discover which reverse mortgage payment plan best suits your needs. Learn more about Term, Ten-Year, and Tenure payments →Expert Insight from Michael Branson, CEO: “A reverse mortgage can be a smart way to bridge the gap before claiming Social Security. By using monthly term payments or a line of credit to cover expenses, some homeowners delay filing for Social Security until a later age, allowing them to lock in a higher lifetime benefit. This strategy can increase long-term retirement income while still giving you the flexibility to use your home equity on your own terms. Your line of credit grows on the portion of the line you do not use, so you can begin allowing the line to grow, giving you greater borrowing power later if you need it. Be sure to check with your financial advisor to see what is right for you regarding your Social Security and/or pension plans.”

The Line of Credit Growth Advantage

The growth rate feature in the HECM program is one of the most compelling aspects of a reverse mortgage and truly sets it apart from every other home loan product on the market. Here’s how it works: all unused funds in your reverse mortgage line of credit are subject to a growth rate equal to your current loan interest rate plus the HUD mortgage insurance renewal rate (currently 0.50% annually).

This means your available line of credit grows each month — not because you’re earning interest, but because HUD’s program rules increase your borrowing capacity on the unused portion. The growth compounds monthly, and the effect over time is substantial.

Example:

A borrower establishes a line of credit of $200,000 with a growth rate of 5.50% and makes no withdrawals:

- After 5 years: Available credit grows to $263,141

- After 10 years: Available credit grows to $346,215

- After 15 years: Available credit grows to $455,517

These figures are based on monthly compounding at a 5.50% annual growth rate with no withdrawals. In practice, interest rate fluctuations and any withdrawals you make will impact the actual growth, but as long as there are funds available in your line of credit, the growth rate is applied to that remaining amount every single month.

Important distinction: This is not interest that you are earning — it is an increase in borrowing capacity. You are not building a savings account; you are expanding the amount you can access from your home equity in the future.

What makes this feature so unusual is that your available credit can eventually exceed your home’s current market value. Unlike a HELOC, which is capped at a fixed credit limit and can be frozen or reduced by the bank, the reverse mortgage line of credit is guaranteed by HUD and continues to grow regardless of what happens to your property value or the broader housing market.

Expert Insight from Michael Branson, CEO: “Even if your reverse mortgage line of credit eventually grows larger than your home’s value, you can still withdraw every dollar tax-free and remain in your home for life. HUD guarantees full access to your line of credit, even if your lender goes out of business through built-in FHA mortgage insurance protections.”

Comparing Interest Rates and Closing Costs

Not all reverse mortgages are created equal. Interest rates, margins, and closing costs can differ significantly between lenders, and these differences have a direct impact on both how much money you receive upfront and how quickly your loan balance grows over time.

A lender with slightly lower upfront closing costs might appear attractive at first glance, but if their margin is 0.50% higher, it will result in a lower available loan amount and higher interest accrual over the life of the loan. Over 10 or 15 years, that difference in margin can add tens of thousands of dollars to your loan balance.

Conversely, a loan with a slightly higher margin will also produce a higher growth rate on the unused funds in your line of credit. So if maximizing long-term line of credit growth is your primary goal, a slightly higher margin could actually work in your favor — but this is a trade-off that requires careful analysis based on your specific situation.

What to Compare When Shopping for a Reverse Mortgage:

- Interest rate + margin — the margin is the lender’s markup added to the index rate, and it stays fixed for the life of the loan. This is often the single most important number to compare.

- Initial loan amount (Principal Limit) and starting line of credit — a lower margin typically means a higher initial loan amount and more money available to you.

- Closing costs — including the origination fee (capped by HUD), appraisal fee, title insurance, and third-party service provider fees.

- Servicing fees — these are rare in today’s market, but some lenders still charge monthly servicing fees that are added to the loan balance.

Smart Strategy: Choose the option that best achieves your most important goal — whether that is maximizing the available loan amount, preserving as much equity as possible, or building the highest possible line of credit growth over time. A good loan officer will walk you through all of these scenarios side by side.

Expert Insight from Michael Branson, CEO: “Watch your financing terms. Don’t accept a larger margin that can end up costing you thousands of dollars in accrued interest over the years and leave you with less money available at closing, to save a little money on one fee. Look at all the terms offered and compare lenders.”

Reverse Mortgage Costs vs. Benefits in 2026

A reverse mortgage can be a valuable retirement planning tool, but as with any financial decision, there are trade-offs to consider. Here is a balanced look at both sides:

Key Benefits

- No required monthly mortgage payments — frees up monthly cash flow by eliminating the obligation of a mandatory mortgage payment. You can still choose to make voluntary payments at any time with no prepayment penalties.

- Stay in your home for life — as long as you live there as your primary residence, maintain property taxes and insurance, and keep the home in reasonable condition.

- Flexible payout options — choose from a lump sum, monthly payment plan (term or tenure), line of credit, or a combination tailored to your needs.

- FHA non-recourse protection — HECM reverse mortgages are non-recourse loans, meaning neither you nor your heirs can ever owe more than the home is worth at the time the loan is repaid. If the loan balance exceeds the home’s value, the FHA insurance fund covers the difference.

- Use proceeds for virtually any purpose — home improvements, medical expenses, debt consolidation, supplementing retirement income, in-home care, or simply building a financial safety net.

- Line of credit growth — unlike a traditional HELOC, your unused line of credit grows in availability over time and cannot be frozen or reduced due to market conditions or changes in your credit profile.

- Non-borrowing spouse protections — if you have a younger spouse who is not on the loan, HUD’s protections (for HECMs originated after August 4, 2014) allow an eligible non-borrowing spouse to remain in the home after the borrowing spouse passes away, with no immediate repayment required.

Pro Tip: Before deciding on a reverse mortgage, think carefully about your long-term aging-in-place plans. Do you live in a two-story home? Is it fully accessible as you get older? In some cases, downsizing or “right-sizing” with a reverse mortgage for home purchase may be a smarter way to secure both comfort and financial flexibility for the years ahead.

Main Costs & Considerations

- Upfront mortgage insurance premium (MIP) — HECMs require an initial MIP of 2% of the home’s appraised value (up to HUD’s lending limit). This is the cost that funds the FHA insurance pool, which in turn provides the non-recourse protection and guarantees your line of credit access even if your lender goes out of business.

- Ongoing MIP charges — an annual renewal MIP of 0.50% is calculated on the outstanding loan balance and added monthly. This is in addition to the loan interest that accrues on the balance.

- Interest accrual increases your loan balance — because no monthly payments are required, unpaid interest compounds on the balance. Over time, this can reduce the equity remaining in your home, particularly if property values remain flat or decline.

- Potential equity reduction for heirs — as the loan balance grows, the inheritance value of the home may decrease. However, heirs always retain the option to sell the home and keep any equity above the loan balance, or to pay off the loan and keep the property.

- Property obligations remain your responsibility — you must continue to pay property taxes, homeowners insurance, and maintain the home. Failure to do so can trigger a loan default.

- Primary residence requirement — HECMs are only available on your primary residence. Vacation homes and investment properties are not eligible. If you move out of the home for more than 12 consecutive months (including for medical reasons such as assisted living), the loan becomes due and payable.

Pro Tip: If preserving home equity for your heirs is your top priority, consider making optional monthly payments or taking smaller draws to slow balance growth and retain a larger portion of your home’s value.

| Feature | Pro | Con |

|---|---|---|

| Home Equity Access | Tap into your home’s value without selling or moving. | Equity decreases over time as loan balance grows. |

| Monthly Payments | No mortgage payments required. | Must still pay taxes, insurance, and maintenance. |

| Stay in Your Home | Live in your home for life. | Must remain your primary residence. |

| Payout Flexibility | Lump sum, monthly income, line of credit, or combination. | Larger upfront draws may reduce future access. |

| Government-Insured | FHA insurance guarantees borrower protections. | Requires upfront and ongoing MIP. |

| Heir Options | Heirs can sell the home at 95% of market value. | Inheritance may be reduced if balance is high. |

| Non-Recourse | You or heirs never owe more than the home’s value. | Heirs must act quickly to settle the loan after death. |

Frequently Asked Questions

Who owns the home with a reverse mortgage?

How much money can I get from a reverse mortgage?

How is the loan amount determined?

Do I need good credit to qualify?

You do not need perfect credit to get a reverse mortgage. Unlike traditional loans, HECMs are primarily equity-based. However, HUD does require a financial assessment that looks at your credit history and your ability to keep up with property charges like taxes and insurance.If your credit history shows past issues, HUD allows a Life Expectancy Set-Aside (LESA) — a portion of the loan reserved to pay your property taxes and homeowners insurance on your behalf. As long as there is enough room in the loan to cover the LESA and satisfy any existing mortgage, you may still qualify. However, the LESA does reduce your available proceeds.

Is an appraisal required?

Can you make payments on a reverse mortgage?

Yes. While the main advantage of a reverse mortgage is that monthly payments are not required, you absolutely can choose to make voluntary payments at any time — and many borrowers do.Making payments reduces your loan balance and increases the available funds in your line of credit. There are no prepayment penalties, no minimum payment amounts, and no required schedule. You can pay as much or as little as you want, whenever you want.

What is the 95% rule on a reverse mortgage?

The 95% rule is an important HUD protection for heirs. When a reverse mortgage becomes due, if the loan balance exceeds the home’s current market value, the heirs are not required to pay the full balance. Instead, they can satisfy the loan by paying just 95% of the home’s current appraised value.For example, if the loan balance is $400,000 but the home is now worth $350,000, the heirs can keep the property by paying $332,500 (95% of $350,000) — saving $67,500 compared to the full balance. This protection exists because HECMs are non-recourse loans backed by FHA insurance.

What are the downsides of a reverse mortgage?

Reverse mortgages are a valuable tool for many homeowners, but there are real downsides to consider:

- Higher upfront costs — HECMs include a one-time Mortgage Insurance Premium of 2% of the home’s value (up to HUD’s lending limit of $1,249,125), plus standard closing costs. These fees are higher than a typical refinance.

- Growing loan balance — because monthly payments aren’t required, interest and MIP charges compound on the balance each month. Over many years, this can significantly reduce the equity remaining in your home.

- Impact on means-tested benefits — while reverse mortgage proceeds are not taxable income, large lump-sum withdrawals that remain in your bank account could potentially affect eligibility for Medicaid or Supplemental Security Income (SSI). Careful planning with a financial advisor can help avoid this issue.

A reverse mortgage generally works best as a long-term solution. If you’re only planning to stay in your home for a few years, the upfront costs may outweigh the benefits.

Can I lose my home with a reverse mortgage?

Yes. Just like with any mortgage, you could lose your home if you don’t meet the loan requirements. With a reverse mortgage, you must:

- Live in the home as your primary residence

- Stay current on property taxes and homeowners insurance

- Keep the home in reasonable repair

If these obligations aren’t met, the lender can call the loan “due and payable.” At that point, the balance must be repaid either by refinancing, selling the home, or paying it off with other funds. If the loan is not repaid, foreclosure is possible.

The good news: as long as you follow the occupancy, tax, insurance, and maintenance requirements, you remain the owner of your home and can stay there for life. Lenders also typically work with borrowers to resolve issues before pursuing foreclosure, and HUD requires servicers to follow specific loss mitigation procedures.

What if I outlive my home’s value?

This is one of the most important protections of a reverse mortgage: it’s a non-recourse loan. You can never owe more than your home is worth at the time the loan is repaid, no matter how long you live there or how much your loan balance grows.For example, if your reverse mortgage balance reaches $500,000 but your home is only worth $450,000 when you leave, neither you nor your heirs are responsible for the $50,000 difference. The FHA Mortgage Insurance Fund — funded by the MIP premiums paid by all HECM borrowers — covers that shortfall.

You can stay in your home for life without worrying about outliving its value, and your heirs’ other assets are fully protected.

How does a reverse mortgage get repaid?

A reverse mortgage is typically repaid when the borrower permanently leaves the home, but repayment can happen at any time since there are no prepayment penalties. The most common repayment methods are:

- Selling the home — the loan is paid from the sale proceeds, and any remaining equity belongs to the homeowner or their heirs.

- Refinancing — the borrower or heirs can refinance into a traditional mortgage or a new reverse mortgage if it makes financial sense.

- Paying with other funds — borrowers or heirs may use savings, life insurance proceeds, or other assets to pay off the balance and retain the property.

In most cases, repayment occurs through the sale of the home after the borrower passes away or moves to a care facility. If the sale price exceeds the loan balance, the remaining equity goes to the heirs. If the balance exceeds the home’s value, heirs owe nothing beyond the home’s worth — the FHA insurance covers the shortfall.

How long do you have to pay back a reverse mortgage?

A reverse mortgage does not need to be repaid until a maturity event occurs. This typically means:

- The last surviving borrower (or eligible non-borrowing spouse) permanently leaves the home, either by moving out or passing away.

- The borrower fails to meet the loan obligations — such as paying property taxes, maintaining insurance, or keeping the home in good repair.

Once the loan becomes due and payable, the servicer will contact the borrower or heirs to discuss repayment options. If heirs plan to sell the property, servicers generally allow extensions of up to 1 year, granted in 90-day increments, as long as good-faith efforts to sell are being made. HUD requires servicers to follow specific timelines and procedures before pursuing foreclosure, and the exact process varies by state law.

Is HUD counseling required before getting a reverse mortgage?

Yes. Federal law requires every HECM borrower to complete a counseling session with a HUD-approved counselor before the loan application can proceed. The counselor is independent from the lender and is required to cover how the loan works, what your obligations are, costs and fees, payout options, and what alternatives to a reverse mortgage may be available.Counseling can be done by phone or in person, typically takes about an hour, and there is a modest fee (usually around $125, which can be paid from loan proceeds). After completing the session, you receive a counseling certificate that your lender needs to move forward with your application. This requirement exists as a consumer protection to ensure every borrower fully understands the loan before committing.

Key Takeaways: How Reverse Mortgages Work in 2026

- A reverse mortgage lets you convert home equity into tax-free loan proceeds without required monthly mortgage payments.

- The most common program is the Home Equity Conversion Mortgage (HECM), insured by the FHA and regulated by HUD.

- You must be 62 or older and live in the home as your primary residence.

- Loan amount depends on your age, home value (up to $1,249,125), and current interest rates.

- HUD-approved counseling is required before your application can proceed.

- You choose how to receive funds: lump sum, line of credit, monthly payments, or a combination.

- Repayment is only due when you sell, move out permanently, or pass away.

- Non-recourse protection means you and your heirs can never owe more than the home’s value.

- You keep full ownership of your home and can sell or pay off the loan at any time with no prepayment penalties.

Expert Insight from Michael Branson, CEO: The biggest advantage of a reverse mortgage is flexibility. You’re not locked into monthly payments, but you can still make them if preserving equity is your goal.Need Personalized Answers? All Reverse Mortgage, Inc. (ARLO™) is here to help. Access our reverse mortgage calculator to estimate your lending limit, or call us Toll-Free at (800) 565-1722. We’re here to help you make informed decisions so you can continue enjoying your retirement.

September 19th, 2025

September 20th, 2025

July 1st, 2025

July 1st, 2025

You can pay it off using your own available funds,You can refinance it with another loan of your choosing,Or you can sell the home and use the proceeds to repay the reverse mortgage.

There is never a prepayment penalty, so you're free to choose whichever option works best for you.Please let us know if you'd like help exploring the next steps.May 13th, 2024

May 13th, 2024

April 29th, 2024

May 5th, 2024

March 7th, 2023

March 7th, 2023

January 8th, 2023

January 12th, 2023

July 21st, 2022

July 21st, 2022

May 17th, 2022

May 17th, 2022

December 30th, 2021

January 11th, 2022

October 27th, 2020

October 27th, 2020

You can take a lump sum of cash (lump sum option).You can take a set payment for life (tenure option).You can determine the payment you wish to take until you exhaust the funds (term payment).You can leave the money in a line of credit and draw from the line as you wish (line of credit option).

Or you can mix the line of credit with the tenure or term options to have both a payment for life or of your choosing and that would be either a modified tenure or modified tenure. In your case, you could choose the line of credit option, draw the amount you want, and the other funds would remain in the line, available to you. If you never draw the money, you never accrue any interest on the funds and you, or your heirs do not need to repay them. You only pay back what you use (plus any interest that accrues on those funds). In addition, the line of credit grows in availability on the unused funds over time. This means that the longer you have funds available on the line, the more money will be available to borrow later should you need them. Again, if you never need them you are not required to repay them but if you ever do need them for any reason, they are always available unlike a Home Equity Line of Credit that the bank can close at their discretion or that goes into a repayment period after 10 years.July 25th, 2020

July 27th, 2020

July 7th, 2020

July 7th, 2020