Get the Facts Before You Decide

|

Michael G. Branson, CEO of All Reverse Mortgage, Inc., and moderator of ARLO™, has 45 years of experience in mortgage banking, with the past 20 years devoted exclusively to reverse mortgages. A Forbes Real Estate Council member, he developed the industry's first fixed-rate jumbo reverse mortgage and has been featured in Forbes, Kiplinger, the LA Times, and Yahoo Finance. (License: NMLS# 14040) |

|

Cliff Auerswald, President of All Reverse Mortgage, Inc., and co-creator of ARLO™ — the industry's first real-time reverse mortgage pricing engine — has 27 years of experience in mortgage banking, with 20+ years focused exclusively on reverse mortgages. A recognized expert in reverse mortgage technology and consumer education, he has been featured in Kiplinger, Yahoo Finance, Realtor.com, and HousingWire. (License: NMLS# 14041) |

Reverse Mortgage Downsides: 10 Myths vs. Facts 2026

Some reverse mortgage downsides are real: closing costs can run higher than traditional loans, and the loan balance will grow if you don't make interest repayments. Others, like losing the home or leaving heirs in debt, are myths. This guide separates the two, claim by claim.

Reverse mortgages have long been surrounded by misconceptions, leading many to believe they come with significant downsides. In reality, many of these concerns are based on myths or incomplete information. In this guide, we separate fact from fiction in the top 10 most common claims about the downsides of reverse mortgages, drawing on more than 20 years of experience helping homeowners at All Reverse Mortgage, Inc. make informed decisions.

Whether you’re exploring reverse mortgage options for yourself or assisting a loved one, understanding the facts behind these so-called ‘downsides’ will help you make a confident and informed decision.

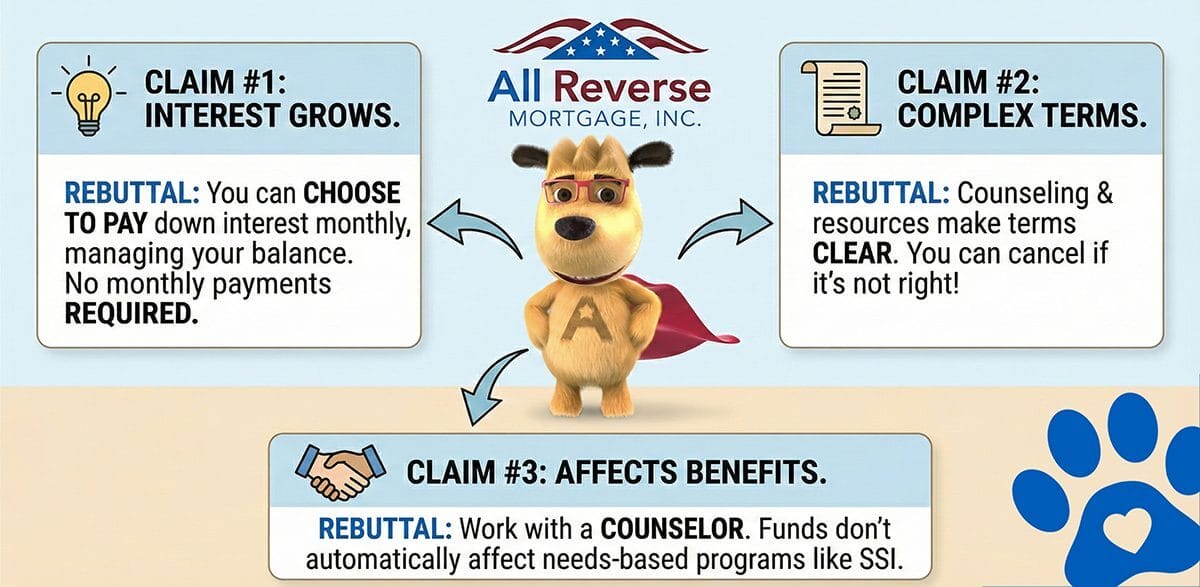

Claim #1: Reverse Mortgages Have Growing Interest and Fees

Concern: Skipping monthly payments may seem like an advantage, but the accumulating interest can significantly increase the total loan balance.

Truth: Like any loan, interest accrues on a reverse mortgage. However, one major benefit is flexibility. You are not required to make monthly payments, but you can choose to pay down the interest whenever you want without penalty. This allows you to manage the loan balance effectively and control how much interest accrues over time.

It’s important to put this in context: if you currently have a traditional mortgage and are making $1,500 or $2,000 per month in payments, a reverse mortgage eliminates that obligation entirely. Yes, interest accrues on the balance — but the cash flow relief can be substantial. Many borrowers use the money they would have spent on mortgage payments to cover healthcare costs, supplement retirement income, or simply reduce financial stress. Some borrowers also choose to make voluntary payments when they can afford to, keeping the balance in check while preserving the option to skip payments when cash flow is tight.

Expert Insight from Michael Branson, CEO: “The growing balance is the concern we hear most often, and it’s a fair one. But the real question is: what’s the alternative? If someone is struggling to make a $1,800 monthly mortgage payment on a fixed income, the cost of keeping that payment may be far greater than the cost of interest accruing on a reverse mortgage. It’s about comparing your actual options, not evaluating the reverse mortgage in a vacuum.”

Claim #2: Reverse Mortgages Have Complex Loan Terms

Concern: Reverse mortgages have complex terms that can lead to unexpected issues with repayment or property use.

Truth: While reverse mortgages have specific terms, they are not inherently confusing. With required counseling, online tools, and supportive lenders, you’ll have the resources to thoroughly understand the details. Plus, you can cancel without penalty if you feel it’s not the right choice for you.

Every HECM borrower is required by federal law to complete a counseling session with a HUD-approved counselor before the loan application can proceed. This counselor is independent of the lender and is required to explain how the loan works, your obligations, all costs and fees, payout options, and any available alternatives. The session typically takes about an hour and can be completed by phone or in person.

After closing, you also have a federally mandated three-day right of rescission — meaning you can cancel the loan for any reason within three business days of closing with no penalty and no obligation.

Claim #3: Reverse Mortgages Affect Needs-Based Programs

Concern: Receiving funds from a reverse mortgage could jeopardize eligibility for programs like Medicaid or Supplemental Security Income (SSI).

Truth: A reverse mortgage doesn’t automatically affect needs-based benefits. These programs don’t count reverse mortgage proceeds as income. The issue arises only if those funds accumulate in your bank account and push you over the program’s asset limit when they evaluate eligibility (SSI’s federal limit is $2,000 for individuals and $3,000 for couples; some Medicaid programs use similar limits). The solution is simple: work with a benefits counselor to understand your state’s rules and make sure any funds you draw don’t sit in your accounts long enough to raise your assets above the allowable threshold.

It is important to note that regular Social Security benefits and Medicare are not affected by obtaining a reverse mortgage under any circumstances. The concern applies only to means-tested programs like Medicaid and SSI. If you receive these benefits, using a line of credit and withdrawing only what you need each month — rather than taking a large lump sum — is typically the best strategy to avoid exceeding asset limits.

Claim #4: Reverse Mortgages Create Repayment Problems for Heirs

Concern: Heirs must sell the property or refinance the loan to keep it, which could cause financial strain.

Truth: Reverse mortgages are not designed to be passed down, but open communication with heirs can prevent complications. Heirs should be informed of their options, such as selling the property or refinancing the loan. Establishing a family trust or consulting an estate attorney can further simplify the process and ensure heirs are prepared.

When the last surviving borrower (or eligible non-borrowing spouse) passes away, heirs have several options. They can sell the home and keep any equity above the loan balance. They can refinance the reverse mortgage into a traditional mortgage if they want to keep the property. Or they can simply walk away — because HECMs are non-recourse loans, heirs are never personally liable for any shortfall if the balance exceeds the home’s value.

HUD also requires servicers to allow heirs reasonable time to sell the property — typically up to 12 months, granted in 90-day increments, as long as good-faith efforts to sell are being made. The process is well-defined, and the most important thing borrowers can do is ensure their heirs understand that the loan exists and know their options.

Claim #5: Reverse Mortgages Mean Rising Debt and Falling Equity

Concern: Home equity decreases as payments are received and interest accumulates, leaving less for heirs.

Truth: While equity can decrease if home values stagnate or interest builds, this isn’t unique to reverse mortgages. Unlike traditional mortgages, reverse mortgages are non-recourse loans, meaning neither you nor your heirs are responsible for any shortfall if the home’s value doesn’t cover the loan balance.

Context matters here. If you’re using a reverse mortgage to eliminate a $1,500 monthly payment you can no longer afford, or to avoid withdrawing from an investment portfolio during a market downturn, or to delay Social Security to lock in a higher lifetime benefit — the net financial impact can be positive even as the loan balance grows. The question isn’t simply whether the balance is increasing; it’s whether the reverse mortgage provides a better overall financial outcome than the alternatives.

Additionally, borrowers can make voluntary payments at any time with no prepayment penalties. Even modest payments can meaningfully slow the balance growth and preserve more equity for heirs over time.

Expert Insight from Michael Branson, CEO: “I’ve worked with borrowers who used a reverse mortgage to delay Social Security by four years, locking in a permanently higher monthly benefit. The additional lifetime income from that strategy far exceeded the interest that accrued on the reverse mortgage. The growing balance is real — but so is the value of what you do with the freed-up cash flow.”

Claim #6: Reverse Mortgages Have Occupancy Restrictions

Concern: Moving permanently, such as to a nursing home, makes the loan due, complicating living situations.

Truth: HECM loans require the home to remain your principal residence, and the loan becomes due and payable if you no longer occupy the home for more than 12 consecutive months. For temporary absences — such as extended travel, visiting family, or short-term medical care — you can be away as long as you maintain the intent to return and the home remains your primary residence. If a medical absence extends beyond 12 consecutive months (such as a permanent move to an assisted living facility), the loan will become due and payable at that point.

This is an important consideration for borrowers whose health may require a future transition to assisted living or long-term care. If a permanent move becomes necessary, the home can be sold and the loan repaid from the proceeds. Any remaining equity belongs to the borrower or their heirs. Planning ahead and discussing potential scenarios with your family and loan officer can help ensure there are no surprises.

Claim #7: Reverse Mortgages Can Be a Burden on Heirs

Concern: Heirs are left to manage repayment and avoid foreclosure under tight deadlines.

Truth: Proper preparation minimizes this burden. By educating heirs on loan terms, authorizing communication with lenders, and establishing clear plans, the process becomes manageable. Early planning ensures heirs know what to expect and how to proceed.

The most important step a borrower can take is to have an open conversation with their heirs about the reverse mortgage — what it is, how it works, and what will happen when the loan becomes due. Many issues heirs face arise not from the loan itself but from not knowing it exists or not understanding their options.

Heirs should know that they will never owe more than the home’s value (non-recourse protection), that they have the right to sell the home and keep any remaining equity, and that HUD requires servicers to provide reasonable time to complete the sale or arrange financing. If heirs want to keep the home, they can pay off the reverse mortgage balance or refinance into a conventional loan. If the balance exceeds the home’s value, heirs can also satisfy the loan by paying just 95% of the current appraised value.

Claim #8: Borrowers Must Maintain Taxes & Insurance

Concern: Failing to keep up with home maintenance, taxes, or insurance could lead to default.

Truth: With any mortgage, you must keep your taxes and insurance current. If you fall behind, HUD requires the lender to declare the loan due and payable, which is why staying on top of these items is so important. If you qualify and have enough available proceeds, your lender can set up a LESA (Life Expectancy Set-Aside). This reserves a portion of your reverse mortgage funds specifically to pay your taxes and insurance, helping prevent future issues and keeping your loan in good standing. It’s a safeguard that many homeowners choose for peace of mind.

This requirement is not unique to reverse mortgages — every homeowner with a mortgage is required to maintain property taxes, insurance, and the condition of the home. The difference is that with a reverse mortgage, you’re not making monthly mortgage payments, so these obligations take on greater importance as the loan’s primary conditions. HUD’s financial assessment at the time of application evaluates your ability to meet these obligations, and the LESA option exists specifically to protect borrowers who may need additional support.

Claim #9: Reverse Mortgages Have a Risk of Negative Equity

Concern: Declining home values may cause the loan balance to exceed the property’s value, resulting in negative equity.

Truth: Reverse mortgages are non-recourse loans, meaning heirs or estates are not responsible for any shortfall. Heirs can repay the loan at 95% of the home’s current market value or choose to walk away without financial liability.

This is one of the most important protections built into the HECM program. The FHA Mortgage Insurance Fund — funded by the mortgage insurance premiums that all HECM borrowers pay — covers the difference if the loan balance exceeds the home’s value at the time of repayment. This means borrowers can live in their home for life without worrying about outliving the equity, and heirs are fully protected from any personal liability.

For example, if your reverse mortgage balance grows to $400,000 but the home is only worth $350,000 when the loan is repaid, neither you nor your heirs owe the $50,000 difference. The FHA insurance covers it. This protection is a fundamental feature of the program and a key reason the upfront mortgage insurance premium exists.

Claim #10: Potential for Scams

Concern: The complexity of reverse mortgages makes them a target for scams.

Truth: Scams typically involve misuse of proceeds rather than the loan itself. Choosing a reputable, HUD-approved lender is key. Open family communication ensures seniors make informed, secure decisions and avoid fraud.

The reverse mortgage itself is a federally insured financial product regulated by HUD. The real risk lies in what happens after the funds are disbursed — unscrupulous individuals may try to convince seniors to invest the proceeds in fraudulent schemes, hand over funds to family members with failing businesses, or make large purchases that aren’t in their best interest.

How to protect yourself:

- Never let anyone pressure you into using reverse mortgage funds for an investment or large purchase you’re not comfortable with

- Be cautious of anyone who contacts you unsolicited offering to help you get a reverse mortgage or “invest” the proceeds

- Take full advantage of your HUD-required counseling session — it’s designed to help you understand the loan before you commit

- Work only with HUD-approved lenders with established track records and verified reviews

- If you suspect financial exploitation, contact your local Area Agency on Aging or call the Eldercare Locator at 1-800-677-1116

Expert Insight from Michael Branson, CEO: “In more than 20 years in this industry, I’ve never seen a borrower harmed by a reverse mortgage itself. The problems I’ve seen come from what someone did with the money — usually at the urging of someone else. The best thing you can do is talk to your family, work with a trusted advisor, and make sure you have a clear plan for how you’ll use the funds before you close.”

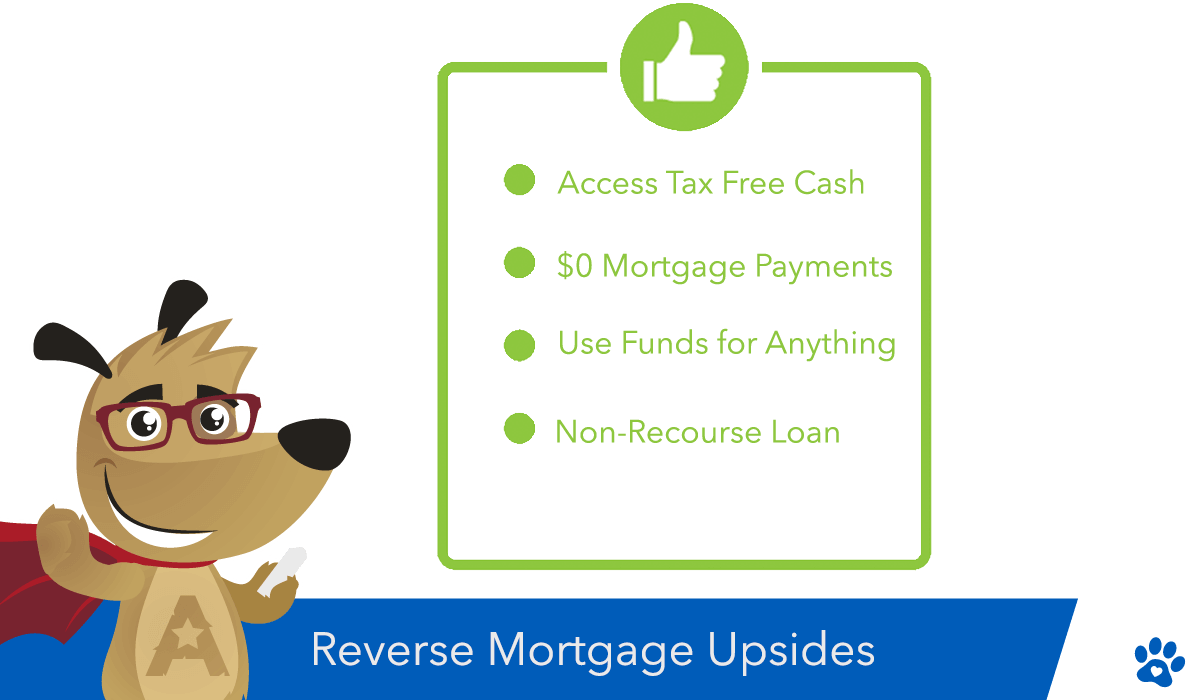

How a Reverse Mortgage Can Enhance Your Retirement

A reverse mortgage offers financial flexibility and security, enabling you to enjoy retirement on your terms:

- Make Your Home Age-Friendly: Fund upgrades like ramps, walk-in tubs, or first-floor bedroom conversions to age in place comfortably.

- Spend How You Wish: Use funds for daily expenses, travel, medical costs, or emergencies — the choice is yours, and the proceeds are tax-free.

- Buy a New Home: The HECM for Purchase program lets you relocate to a retirement-friendly property without monthly mortgage payments.

- Pay for In-Home Care: Cover the cost of in-home caregivers, allowing you to receive assistance while remaining in the comfort of your home.

- Create a Growing Safety Net: Establish a line of credit that increases in availability over time — a financial reserve that grows even when you’re not using it.

- Delay Social Security: Use term payments or line of credit draws to bridge the gap until you can claim Social Security at a higher benefit amount.

Key FHA Protections

- Non-Borrowing Spouse Protections: For HECMs with case numbers assigned on or after August 4, 2014, an eligible non-borrowing spouse can remain in the home after the borrowing spouse passes away, with loan repayment deferred as long as they meet the loan obligations.

- Non-Recourse Protection: Neither you nor your heirs will ever owe more than the home’s value at the time the loan is repaid. The FHA Mortgage Insurance Fund covers any shortfall.

- Guaranteed Access to Funds: As long as you meet your loan obligations, your line of credit or monthly payments remain fully accessible — HUD guarantees them even if your lender goes out of business.

Below is a clear, side-by-side breakdown of the most common reverse mortgage concerns and the facts.

Reverse Mortgage Downsides Explained: Myths vs. Reality (2026)

| Common Concern | What the Facts Show |

|---|---|

| Interest and fees grow over time | Yes, interest accrues over time, like any mortgage. However, borrowers may make voluntary payments at any time to reduce their balance, and there is no prepayment penalty on a HECM. |

| Loan terms feel too complex | Reverse mortgages require independent HUD counseling before you can apply. Lenders must also provide clear disclosures, and you may stop the process at any point before closing. |

| A reverse mortgage could affect Medicaid or SSI | HECM proceeds are not considered income. Benefits may only be affected if unused funds remain in your bank account and push assets over program limits. Planning withdrawals with a benefits counselor helps most borrowers stay eligible. |

| Heirs will struggle with repayment | Your heirs have options. They may sell the home, refinance the loan, or Deed in Lieu of Foreclosure. The loan is typically repaid from the home’s value, not from heirs’ personal assets. |

| Equity will shrink over time | Home equity may decrease over time, but a HECM is a non-recourse loan. You and your heirs are never personally responsible for more than the home’s value at repayment at time of sale. |

| Leaving the home will trigger repayment | A HECM requires the home to remain your primary residence. HUD allows absences up to six months for non-medical reasons and up to twelve months for documented medical reasons. Longer absences may cause the loan to become due. |

| Loved ones will be burdened after death | With advance planning, settling a reverse mortgage is usually straightforward. Heirs receive written guidance from the servicer explaining timelines and available options. |

| You must pay taxes and insurance | Like any mortgage, borrowers must stay current on property taxes and insurance. If eligible, a Life Expectancy Set-Aside (LESA) can be established to pay these expenses automatically. |

| You might owe more than the home is worth | Because the HECM is FHA-insured and non-recourse, borrowers and heirs never owe more than the home’s market value. Heirs may repay at 95% of the appraised value or walk away without liability. |

| Reverse mortgages are tied to scams | Scams involve misuse of funds, not the HECM program itself. Working with a HUD-approved lender, completing counseling, and involving trusted family members reduces risk. |

Frequently Asked Questions

What is the downside of a reverse mortgage?

A reverse mortgage has both advantages and drawbacks. The main downsides include higher upfront closing costs (due to FHA mortgage insurance), a growing loan balance over time as interest and MIP compound monthly, and reduced equity available for heirs. Additionally, the home must remain your primary residence — if you move out for more than 12 consecutive months, the loan becomes due and payable. Taking out a reverse mortgage too early in retirement can also be a concern if your financial needs change or you decide to relocate later, as you may have less available equity for your next home purchase. It’s important to carefully weigh the pros and cons and consult with a trusted financial advisor and your family to determine if it’s the right choice for your long-term plans.

Is a reverse mortgage ever a good idea?

Yes, a reverse mortgage can be a smart option for homeowners 62 and older who plan to stay in their home long-term and want to eliminate monthly mortgage payments, supplement retirement income, or build a growing financial safety net through the line of credit. Common situations where a reverse mortgage makes strong financial sense include: eliminating an existing mortgage payment that’s straining a fixed income, bridging the gap before claiming Social Security at a higher benefit, funding home modifications for aging in place, covering long-term care costs without depleting savings, or establishing a line of credit that grows over time as a reserve for future needs. When used with a clear plan and professional guidance, a reverse mortgage can meaningfully improve retirement security.

Can you lose your home with a reverse mortgage?

To stay in your home, you must meet the terms of your reverse mortgage, including paying property taxes and homeowners insurance, maintaining the home in reasonable condition, and continuing to live there as your primary residence. Failure to meet these obligations can result in the loan becoming due and payable, which could lead to foreclosure if the balance is not repaid. The good news is that HUD requires servicers to follow specific loss mitigation procedures before pursuing foreclosure, and lenders typically work with borrowers to resolve issues. If staying current on taxes and insurance is a concern, a Life Expectancy Set-Aside (LESA) can be established to cover those payments automatically from your loan proceeds. As long as you meet your obligations, you can remain in your home for life.

What happens to a reverse mortgage when you die?

When the last surviving borrower or eligible non-borrowing spouse passes away, the reverse mortgage becomes due and payable. The servicer will contact the heirs to discuss their options:

- Sell the home — the loan is repaid from the sale proceeds, and any remaining equity belongs to the heirs

- Refinance or pay off the loan — heirs can use savings, life insurance proceeds, or a new mortgage to retain the property

- Walk away — because the HECM is a non-recourse loan, heirs are not personally liable for any shortfall if the balance exceeds the home’s value

HUD requires servicers to allow heirs reasonable time to complete the process — typically up to 12 months, granted in 90-day increments, as long as good-faith efforts to sell or settle are being made. If the home’s value exceeds the loan balance, heirs keep the difference. If the balance exceeds the home’s value, heirs can satisfy the loan by paying just 95% of the current appraised value, or walk away with no personal liability.

Is a reverse mortgage a scam?

No. The HECM (Home Equity Conversion Mortgage) is a federally insured financial product regulated by the U.S. Department of Housing and Urban Development (HUD) and insured by the Federal Housing Administration (FHA). It has been available since 1988 and includes multiple consumer protections, including mandatory independent counseling, non-recourse protection, and a three-day right of rescission after closing. Misconceptions about reverse mortgages often stem from outdated information, confusion with older loan products that lacked today’s protections, or commentary from public figures who may not be familiar with the current program rules. The most important step you can take is to educate yourself with accurate, current information and work with a reputable HUD-approved lender. Also see: Are Reverse Mortgages a Scam? Here’s the Facts You Need to Know

Is HUD counseling required before getting a reverse mortgage?

Yes. Federal law requires every HECM borrower to complete a counseling session with a HUD-approved counselor before the loan application can proceed. The counselor is independent of the lender and is required to explain how the loan works, your obligations, all costs and fees, payout options, and any available alternatives. Counseling can be completed by phone or in person, typically takes about an hour, and there is a modest fee (usually around $125, which can be paid from loan proceeds). After completing the session, you receive a counseling certificate that your lender needs before your application can move forward. This requirement serves as a consumer protection measure to ensure every borrower fully understands the loan before committing — and it’s one of the reasons reverse mortgage borrowers tend to be well-informed about their loan terms.

Summary: Making Informed Decisions About Reverse Mortgages

The common “downsides” of reverse mortgages — growing interest, complexity, eligibility concerns, and impact on heirs — are real considerations, but they are manageable with proper planning and a clear understanding of how the loan works. Most of the concerns we’ve addressed in this guide can be mitigated through open family communication, working with trusted advisors, and choosing a reputable lender.

A reverse mortgage is not the right fit for everyone. It works best for homeowners who plan to stay in their home long-term, want to eliminate monthly mortgage payments, and have a clear purpose for the funds. If you’re considering a move in the next few years or need to preserve maximum equity for your heirs, other options may serve you better.

The most important steps you can take are: educate yourself with accurate information, complete your HUD counseling thoroughly, discuss the decision with your family, and work with an experienced loan officer who will walk you through every scenario — including the ones where a reverse mortgage may not be the best choice.

Have Questions About Reverse Mortgage Downsides? At All Reverse Mortgage, Inc., we walk you through every detail — honestly and without pressure. Call us Toll-Free at (800) 565-1722 to speak with our licensed experts, or get an instant quote using our free reverse mortgage calculator — no personal information required.

May 16th, 2024

May 22nd, 2024

March 16th, 2024

March 19th, 2024

December 30th, 2021

January 11th, 2022

June 10th, 2021

August 4th, 2020

August 14th, 2020

June 4th, 2020

June 8th, 2020

May 26th, 2020

June 2nd, 2020

April 24th, 2020

May 3rd, 2020

September 4th, 2019

September 4th, 2019