|

Michael G. Branson, CEO of All Reverse Mortgage, Inc., and moderator of ARLO™, has 45 years of experience in mortgage banking, with the past 20 years devoted exclusively to reverse mortgages. A Forbes Real Estate Council member, he developed the industry's first fixed-rate jumbo reverse mortgage and has been featured in Forbes, Kiplinger, the LA Times, and Yahoo Finance. (License: NMLS# 14040) |

|

Cliff Auerswald, President of All Reverse Mortgage, Inc., and co-creator of ARLO™ — the industry's first real-time reverse mortgage pricing engine — has 27 years of experience in mortgage banking, with 20+ years focused exclusively on reverse mortgages. A recognized expert in reverse mortgage technology and consumer education, he has been featured in Kiplinger, Yahoo Finance, Realtor.com, and HousingWire. (License: NMLS# 14041) |

Dave Ramsey Offering Bad Advice on Reverse Mortgages

Does Dave Ramsey know much about reverse mortgages? Dave does a hit piece on reverse mortgages, pointing out some of the less popular aspects of the loan. However, he is either OK with exaggerating the truth or reveals his ignorance about how reverse mortgages work.

Is Dave Right About Reverse Mortgages?

Firstly, let’s give Dave his due when he tells the truth. He is right when he says a reverse mortgage operates in reverse of a standard or forward loan.

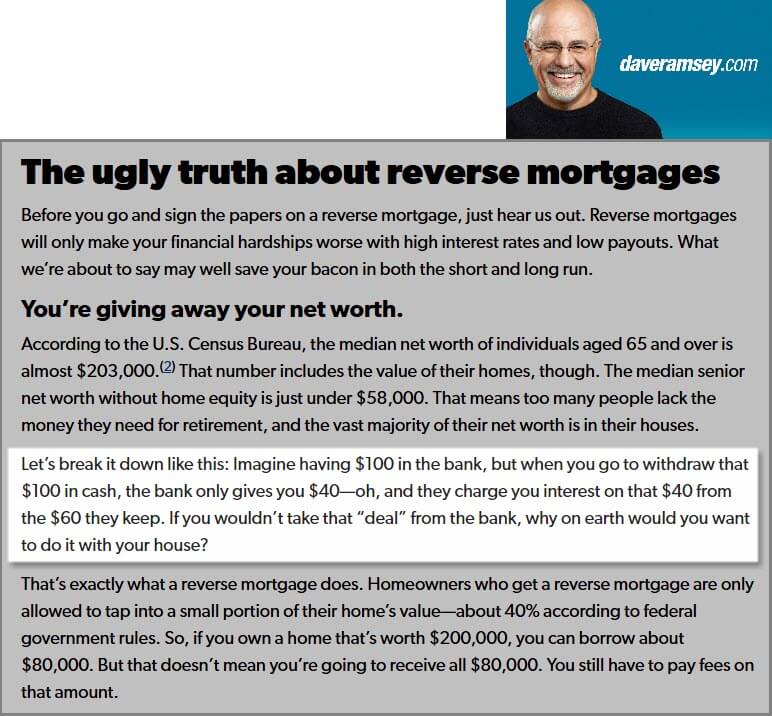

Instead of a rising equity, falling debt scenario, the reverse mortgage is a rising debt, falling equity loan. However, he uses an example where you put $100 in the bank, get $40 back, and they take the interest from the $60.00 you have remaining in the bank, and claim that no one would do this.

How Debt Works

Dave doesn’t tell you that all debt works in much the same way. You use a small amount of the funds and pay much more back in payments. If you have a credit card and make a purchase, you then make monthly payments of $50.00, of which only $5.00 goes toward paying off the amount you borrowed.

Examine the disclosures for standard 30-year mortgages, which typically require monthly payments. After 30 years, you probably paid 2½ times more than you borrowed on those as well. So yeah, Dave, people take that “deal” day in and day out when they want or need something and don’t have the cash to pay for it outright.

I see ads for 30-year fixed-rate loans with low down payments or even no down payments for veterans, and think, what happens when they have no equity, AND they have been paying through the nose each month, so they have no cash either?

Dave, Where Are You Getting Your Info?

Dave says homes above $679,650 don’t qualify for a reverse mortgage. Fact: The FHA lending limit is $1,249,125 for 2026 — and higher-value homes can still use a HECM.

Dave mistakes the HUD lending limit (now $1,249,125 for 2026) with the maximum your home can be worth. You could always have a home valued higher than the limit and still qualify for the loan; however, there were no additional benefits for homes valued above the maximum limit.

Dave thinks you can’t owe any federal debts, which is inaccurate, but you may be required to pay them at closing in some cases. Dave thinks heirs have two options when the borrowers pass: pay the loan off at the full amount or give the house to the lender.

This, again, is either false or misleading at best.

Dave tells listeners heirs must either pay off the full loan or give up the house. Fact: Heirs can refinance or pay just 95% of the current appraised value, or walk away with no debt if the home is underwater.

Heirs can choose several options. If you want to keep the home, you may pay off the amount owed, or 95% of the current appraised value, whichever is less. This is usually achieved by a new refinance loan in the heirs’ name if they want to keep the home.

If they do not want to keep the home and there is still equity in the property, they can sell the house and pocket the equity. Finally, if they do not want to sell the home because there is no equity remaining and do not wish to be involved in the property disposal, they can walk away and owe nothing, regardless of the value and loan balance.

Reverse Mortgages Are Insured, Unlike Bank HELOCs

Dave claims FHA insurance doesn’t benefit borrowers. Fact: FHA insurance guarantees borrowers get every penny promised and protects heirs from owing more than the home is worth at the time of sale.

The loan is a non-recourse loan, and the lender and HUD cannot look to any other assets of the borrower or the borrower’s estate for repayment of any shortfall.

The insurance covers this, the borrower received with the loan – oh, that Dave said doesn’t cover the borrower. Still, here we see that the borrower’s estate and heirs benefit from the insurance, other than just the availability of the loan itself.

The insurance also guarantees that, regardless of what happens to lenders in the future, borrowers will always receive all funds due to them, and the loan will never be closed, unlike HELOCs, which are often terminated when banks decide they no longer want the product due to declining values.

Dave talks about a reverse mortgage, giving away your net worth. He provides the example of the average net worth of senior borrowers being almost $203,000, but under $58,000 without home equity.

And this is where we encourage borrowers to consult with their financial advisors and families to determine what’s right for them. If they can’t afford to stay home without help, the family may work out their own “reverse mortgage” arrangement to help the senior homeowner.

But if it comes down to a reverse mortgage or a move, you must do all the math and consider the emotional aspects, which Dave doesn’t even mention.

Reverse Mortgages Aren’t for Everyone — and We Agree!

Here are some things we agree with Dave, but he only shows one side of the coin in this part of his pitch. Reverse mortgages are not for all senior borrowers. If you cannot pay taxes, insurance, and all other obligations even after you obtain your reverse mortgage, then it is not the right loan for you.

It is a default under the terms of the loan if you do not pay your taxes and insurance on time or if you let the property fall into serious disrepair, so we advise borrowers to bring family members into the discussion and to be sure that this loan makes their finances secure enough that payment of these obligations is never in question.

You should consider other options if you still cannot afford to live comfortably with all obligations after a reverse mortgage.

Dave Thinks Selling Your Home Is a Cheaper Alternative

Costs Compared Unfairly: Dave says selling is cheaper than a reverse mortgage. Reality Check: Realtor commissions, closing fees, and moving expenses can easily add up to $17,000 or more on a $200,000 home, before even paying for a new place.

And yes, the loan with the insurance is costly. However, neither is selling a house with 3–6% commissions. Rent in most areas of the country these days is not cheap either if you don’t have the income and credit to purchase again under Dave’s plan and can’t pay cash!

With Dave’s example: a $200,000 house with a 6% real estate commission ($12,000), miscellaneous closing costs ($2500), and moving expenses ($2500), you can easily “give away” (his words) $17,000 on the sale of and move from a $200,000 home and that doesn’t include any expenses at the new place, especially if you are buying there!

We recognize that this loan is not intended for multi-generational use. If you have family living with you who need to stay after you pass, and you don’t think they can refinance the loan (even after years of no payments), this may not be a good option for them if they can’t save up enough to move later.

We always advise borrowers and heirs to discuss future options and plans before it is too late.

What Dave Ramsey Doesn’t Tell You About Reverse Mortgages

Dave warns you could “lose your home” if taxes or insurance aren’t paid. Truth: That’s true for any mortgage, even a regular forward loan.

Finally, the one thing that Dave doesn’t tell you is that although there are no monthly mortgage payments due on a reverse mortgage, there is no prepayment penalty, so that you can make a payment in any amount at any time without penalty.

Dave says you can lose your home if you don’t pay your taxes, insurance, and HOA dues, but he doesn’t tell you that with a regular mortgage, the exact verbiage is also in their loan documents. You can lose any home with any mortgage (and even without a loan if you wait long enough) by not paying due assessments on your home.

Dave further points out all the steps you can take to create budgets and make payments, save money with a regular mortgage, and direct you to a forward mortgage lender with whom he may or may not have an affiliation. Still, if you can make those payments, you can do it with a reverse mortgage.

How can paying the same assessments plus a mortgage payment possibly be less risky if you run into trouble?

Is Dave Ramsey Biased Against Reverse Mortgages Because of Financial Interest?

I don’t want to cast any aspersions on Dave because I have no actual knowledge of the matter. Still, since Dave has a link to an intake form with his name on it and the name of another lender, I strongly suspect that Dave is acting as a lead generation source for the lender he names for compensation (he can’t originate the loan because he is not a licensed originator, so he has to send them your information as a lead if this is what he is doing).

If so, it stands to reason that this would incentivize Dave to push forward mortgages (specifically, their mortgages) because it brings him income. I’m not accusing Dave of anything; this is not illegal.

However, you won’t find us promoting other programs on our website to participate in a lead generation system. If Dave is doing this, as it strongly appears that he is, I think he should be a little more honest about that in his article and tell you from the start that a forward mortgage lender is compensating him for all the leads he generates.

What do you think about it, Dave? Is this the case?

I Come at This from a Different Perspective Than Dave

I had been a mortgage banker for many years and had never originated a reverse mortgage or even known what they were until my mother came to me, told me she was considering one, and asked for my thoughts on the idea.

This being almost 20 years ago, I told her I had to investigate them and would let her know. For her, it was the greatest thing we could have done. She fixed up her home, had a line of credit for other expenses that arose, and enjoyed a steady stream of additional income each month with the modified tenure loan.

We had to move Mom into assisted living a little under a year ago and sell the home she had owned for 55 years. Because the loan was used judiciously, she had the income she needed to do what she wanted; the house was in great shape, and with the repairs she had made, it sold quickly. Additionally, there was still significant equity in the home when we sold it.

But the biggest thing was that she could stay in the home she loved all those years.

For the last 20 years, I have originated only reverse mortgages, saving numerous borrowers from foreclosure, including some just hours before their homes were scheduled to be sold. I had counseled borrowers against the loan when it didn’t make sense and advised them to explore other options, even when I knew it meant I would not be able to originate the loan.

We give borrowers all the information (not half-truths, as I read here), and that, Dave, is no scam!

Confused by Dave Ramsey’s Reverse Mortgage Advice? Get the real facts with a free quote from All Reverse Mortgage, Inc. (ARLO™) — America’s #1 Rated Reverse Lender with a 4.99/5-star rating! Call (800) 565-1722 or click here for an instant quote.

Top FAQs

What does Dave Ramsey say about reverse mortgages?

Will you owe more than the home is worth?

Can you lose your home if you have a reverse mortgage?

Are reverse mortgages scams?

Is a reverse mortgage a good idea?

Also See: What Suze Orman Says About Reverse Mortgages (2011-Present)

May 10th, 2021

May 10th, 2021

May 15th, 2021

May 15th, 2021

May 15th, 2021

May 15th, 2021

December 9th, 2020

December 9th, 2020

April 14th, 2020

April 20th, 2020

March 17th, 2021

March 19th, 2021

March 22nd, 2020

March 30th, 2020