Reverse Mortgages in Longmont

|

Michael G. Branson, CEO of All Reverse Mortgage, Inc., and moderator of ARLO™, has 45 years of experience in mortgage banking, with the past 20 years devoted exclusively to reverse mortgages. A Forbes Real Estate Council member, he developed the industry's first fixed-rate jumbo reverse mortgage and has been featured in Forbes, Kiplinger, the LA Times, and Yahoo Finance. (License: NMLS# 14040) |

|

Cliff Auerswald, President of All Reverse Mortgage, Inc., and co-creator of ARLO™ — the industry's first real-time reverse mortgage pricing engine — has 27 years of experience in mortgage banking, with 20+ years focused exclusively on reverse mortgages. A recognized expert in reverse mortgage technology and consumer education, he has been featured in Kiplinger, Yahoo Finance, Realtor.com, and HousingWire. (License: NMLS# 14041) |

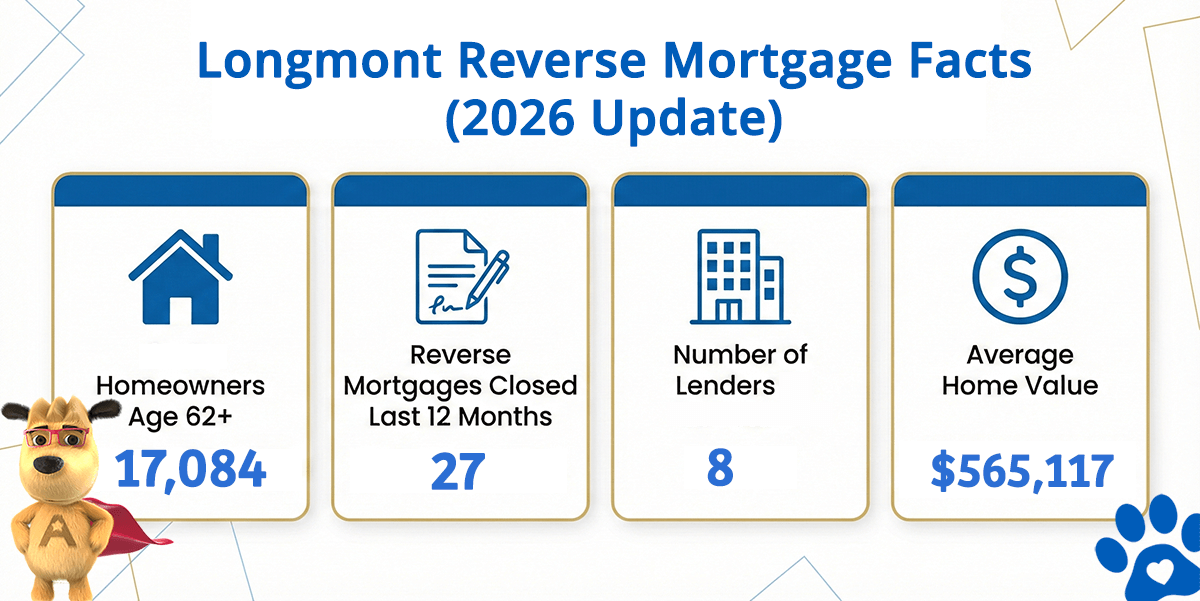

Longmont Reverse Mortgage Market at a Glance

Longmont Reverse Mortgage Facts (2026 Update)

| City | Homeowners Age 62+ | Reverse Mortgages Closed Last 12 Months | Lenders in Longmont (est) | Avg. Home Value |

|---|---|---|---|---|

| Longmont | 17,084 | 27 | 8 | $565,117 |

What the Numbers Tell Us About Reverse Mortgages in Longmont

Longmont positions itself as Boulder County’s dynamic tech corridor, bridging Denver’s urban energy and Fort Collins’ academic influence. With median home values near $565,117 and a robust population of 17,084 residents age 62 and older, Longmont homeowners command meaningful equity across diverse neighborhoods. At the current FHA lending limit of $1,249,125, the majority of Longmont properties unlock substantial borrowing capacity, giving retirees genuine access to their equity for strategic purposes.

Longmont’s reputation as a tech hub attracts entrepreneurial retirees, university staff, and professionals seeking Colorado mountain living without isolation. The community blends outdoor recreation emphasis with growing urban amenities, creating appeal across diverse life stages. With 17,084 residents age 62 and older, Longmont represents a significant demographic segment actively transitioning into retirement years, many carrying substantial home equity after decades of ownership.

The Boulder County lending market includes active FHA-approved lenders serving the tech-forward community. This competitive dynamic ensures meaningful options and genuine pricing leverage when evaluating reverse mortgage partners.

Longmont’s residential character spans tech-forward northwest neighborhoods, historic downtown revitalization areas, and established south Longmont communities. Many residents relocated to Longmont specifically for outdoor access, community values, and quality of life—factors strongly correlated with long-term residence and aging-in-place planning. This genuine community commitment, paired with solid home equity positions, positions many Longmont homeowners as natural candidates for reverse mortgage exploration.

How a Reverse Mortgage Works for Longmont Homeowners

A reverse mortgage is an FHA-insured loan exclusively for homeowners age 62 and older. Unlike traditional mortgages, you make no monthly payments. Instead, the lender advances funds based on your home equity, and repayment occurs when you sell, relocate, or pass away. The HUD HECM program has provided this structure consistently since 1989, with robust consumer protections and comprehensive federal regulatory frameworks.

For Longmont homeowners, the mechanism prioritizes flexibility and control: you keep full ownership, maintain complete decision-making authority, and benefit from FHA insurance guarantees. Understanding your mortgage reversal options helps you choose your funding method—lump sum, monthly payments, line of credit, or strategic combinations—aligned with your personal financial situation.

Common Uses in Longmont

- Tech Industry Transition Planning — Longmont residents frequently use reverse mortgage proceeds to fund entrepreneurial projects, consulting ventures, or sabbaticals during active retirement. Explore case examples of how professionals have strategically used funds.

- Healthcare and Wellness Investment — Those prioritizing active aging use proceeds for fitness programs, wellness facilities, healthcare transitions, or in-home health support, maintaining independence. Learn guidelines for healthcare-focused fund deployment.

- Recreation and Outdoor Adventure Funding — Many leverage reverse mortgages to pursue outdoor passions—hiking expeditions, climbing trips, or second-home adventures near Colorado’s mountains. Review property qualification standards for your Longmont home.

- Educational Support and Grandchild Goals — Tech-oriented families use proceeds to fund educational opportunities, support talented grandchildren, or pursue personal learning goals. Understand non-recourse benefits and estate protection features.

Longmont Reverse Mortgage Eligibility

| Requirement | Details |

|---|---|

| Age | Must be at least 62 years old; examine comprehensive age requirements for married couples and non-borrowing spouse options. |

| Home Ownership | You must own your Longmont home outright or hold substantial equity (typically 50%+). Condominiums require FHA project certification. |

| Primary Residence | The home must be your primary place of residence; rental properties and second residences are not eligible. |

| Property Type | Single-family homes, townhomes, and FHA-approved condos qualify. Manufactured homes have specialized eligibility rules. |

| Financial Assessment | Lenders conduct a financial assessment to verify your capacity to maintain property taxes, insurance, and applicable HOA fees. |

| Counseling | A HUD-approved counseling session (free and independent) is required before loan closing. |

Use our free reverse mortgage calculator to estimate your borrowing capacity based on your Longmont home value and age.

Understanding the Costs

Reverse mortgages involve legitimate expenses: origination fees, appraisal charges, title insurance, and FHA mortgage insurance (both upfront and annual elements). Typical costs range from 2% to 5% of your loan amount, with interest accruing and compounding until you vacate your home. Examine closing cost breakdowns in detail and carefully weigh them against the documented benefits and limitations for your specific financial circumstances.

Is a Reverse Mortgage Right for You?

A reverse mortgage isn’t appropriate for everyone—it’s a specialized financial tool with distinct benefits and constraints. If you intend to remain in your Longmont home long-term, want to avoid monthly mortgage payments, and need accessible funds, this strategy may suit your situation. If your primary goal is maximizing inheritance left to heirs, or if you’re uncertain about long-term housing plans, a home equity line of credit might offer advantages. Worried about predatory lender tactics? Review reverse mortgage scam awareness and thoroughly examine potential drawbacks before deciding.

HUD-Approved Direct Lender Serving Longmont

All Reverse Mortgage Inc. is an FHA-approved HECM lender serving Longmont and the entire Boulder County region with direct lending authority. We guide Colorado retirees through the decision process with transparent communication, detailed fee discussions, and comprehensive support. Verify our BBB standing for independent reviews and accreditation. Check our HUD lender status anytime. For homes exceeding FHA lending limits, we offer jumbo reverse mortgage products.

All Reverse Mortgage Inc. maintains licensure from the Colorado Department of Regulatory Agencies (DORA) (License #100032569), meeting all Colorado and federal standards for reverse mortgage lending operations.

Get a Reverse Mortgage Quote for Your Longmont Home

Use the ARLO™ calculator for an instant quote with real-time current rates — no personal information required.

Related Resources

Foundational overview of Home Equity Conversion Mortgage program, mechanisms, funding options, and repayment terms.

Complete eligibility requirements including age minimums, equity thresholds, property types, and financial assessment criteria.

Discover credit line features, growth mechanics, flexibility advantages, and applications for evolving financial needs.

Understand what lenders evaluate during financial assessments and property reviews for loan eligibility determination.

Statewide directory of FHA-approved HECM lenders, market activity statistics, and provider information.

Denver to Boulder corridor market overview, HECM lending trends, and regional homeowner resources.