America's #1 Rated Reverse Mortgage Lender*

|

Michael G. Branson, CEO of All Reverse Mortgage, Inc., and moderator of ARLO™, has 45 years of experience in mortgage banking, with the past 20 years devoted exclusively to reverse mortgages. A Forbes Real Estate Council member, he developed the industry's first fixed-rate jumbo reverse mortgage and has been featured in Forbes, Kiplinger, the LA Times, and Yahoo Finance. (License: NMLS# 14040) |

|

Cliff Auerswald, President of All Reverse Mortgage, Inc., and co-creator of ARLO™ — the industry's first real-time reverse mortgage pricing engine — has 27 years of experience in mortgage banking, with 20+ years focused exclusively on reverse mortgages. A recognized expert in reverse mortgage technology and consumer education, he has been featured in Kiplinger, Yahoo Finance, Realtor.com, and HousingWire. (License: NMLS# 14041) |

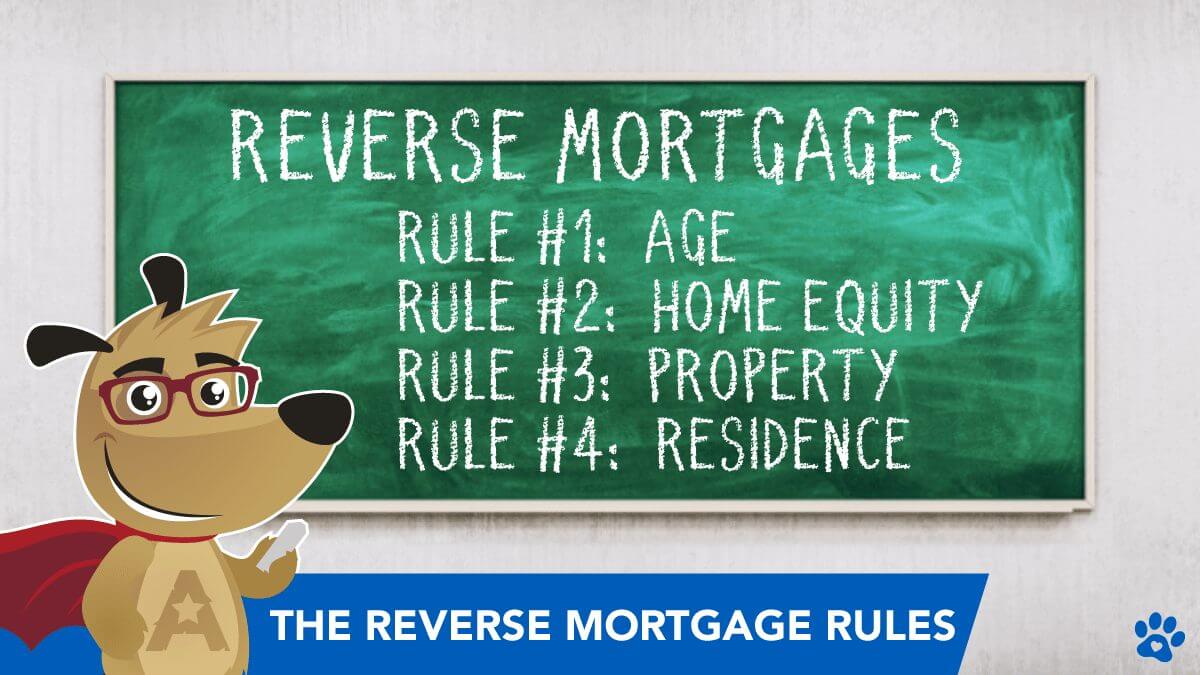

5 Rules for Getting a Reverse Mortgage — Eligibility, Counseling, Property & Payment Options

Reverse mortgages can provide older homeowners with financial flexibility, but navigating the rules doesn’t have to be daunting. As of 2026, important updates to reverse mortgage guidelines have been introduced, making it crucial for those 62 and older to stay informed.

If you’re considering tapping into your home equity, this guide simplifies the five essential rules for reverse mortgages. From eligibility requirements to key protections, we’ll cover everything in clear, straightforward language to help you make a confident decision about your future.

Let’s explore these rules step by step so you can unlock the potential of your home with peace of mind.

Key Criteria for Qualifying

| Rule | Detail |

|---|---|

| Borrower Age Requirement | Borrowers must be at least 62 years old. |

| Primary Residence | The property must be the borrower's primary residence. |

| Equity Requirement | Borrowers must have substantial equity in their home (typically at least 50%). |

| Financial Assessment | Lenders conduct a financial assessment to ensure the borrower can afford taxes, insurance, and home maintenance. |

| Loan Repayment | The loan becomes due when the borrower sells the home, moves out, or passes away. |

| Counseling Requirement | Borrowers must undergo counseling from a HUD-approved agency. |

| Property Eligibility | Eligible properties include single-family homes, FHA-approved condominiums, and certain manufactured homes. |

#1. Limit on How Much You Can Borrow with a Reverse Mortgage

While it might be ideal to borrow as much as you need, reverse mortgages have strict borrowing limits set by the government. For 2026, the maximum amount you can borrow through a Home Equity Conversion Mortgage (HECM) is $1,249,125. However, it’s important to note that most borrowers will not qualify for the full amount.

The exact amount you can borrow depends on several factors:

- Your Age: Specifically, the age of the youngest homeowner or eligible non-borrowing spouse.

- Your Home’s Value: The loan is calculated based on your home’s value, but only up to the 2026 lending limit of $1,249,125.

- Current Interest Rates: Lower interest rates often allow for a higher loan amount, while higher rates can reduce it.

These rules are designed to ensure that your loan aligns with your unique situation and provides financial security for both you and the lender.

#2. Required Counseling for a Reverse Mortgage

Before securing a reverse mortgage, you’ll need to complete a mandatory counseling session. This session ensures you fully understand the process, responsibilities, and implications of the loan, empowering you to make an informed decision about your financial future.

During the session, you’ll meet with an independent HUD-approved counselor who will:

- Explain how reverse mortgages (HECM loans) work.

- Answer any questions you may have about the loan process.

- Discuss your financial situation to ensure a reverse mortgage is a suitable option for your needs.

You’ll also learn about ongoing responsibilities that come with the loan. Even after obtaining a reverse mortgage, you’ll need to cover:

- Property Taxes: Keeping these up to date is essential.

- Homeowners Insurance: Required to protect your property.

- HOA Fees (if applicable): These must also remain current.

Additionally, you must not have overdue federal debts to qualify. Examples include:

- Outstanding student loans.

- Government direct loans.

- HUD-insured loans.

- Small Business Administration loans.

Once you’ve completed the session, you’ll receive a certificate of completion, which must be included with your loan application. This step ensures you’re well-informed and prepared before moving forward.

#3. Qualifying Property Types for a Reverse Mortgage

Not every property qualifies for a reverse mortgage, so it’s important to understand the property requirements before applying.

Here’s what you need to know:

General Ownership Requirements

- You must either own your home outright or have a small remaining mortgage balance that the reverse mortgage can pay off.

- The property must serve as your primary residence — vacation homes or second homes are not eligible.

Eligible Property Types

- Single-Family Homes: These are the most common properties eligible for a reverse mortgage.

- Multi-Family Homes (Up to 4 Units): Eligible if you live in one of the units as your primary residence.

- Condominiums: Must meet FHA approval standards.

- Manufactured Homes: Must meet specific criteria, such as being permanently fixed to a foundation and meeting HUD standards.

Ineligible Properties

- Vacation homes or second homes.

- Co-ops (cooperative housing units).

Meeting these requirements ensures your property is eligible for a reverse mortgage, helping you access the financial benefits of your home’s equity.

#4. Non-Borrowing Spouse Protections May Apply

A non-borrowing spouse (NBS) is a spouse who is not listed on the home’s title or the reverse mortgage loan. This can happen if the spouse is under 62 years old or for other personal reasons. While non-borrowing spouses are not considered borrowers, changes introduced by the Department of Housing and Urban Development (HUD) in 2014 provide important protections.

Key Protections for Non-Borrowing Spouses

If the borrowing spouse passes away, the non-borrowing spouse may be allowed to remain in the home, provided they meet specific conditions, such as:

- The home remains the non-borrowing spouse’s primary residence.

- The loan obligations, such as property taxes, homeowners insurance, and maintenance, continue to be met.

- The non-borrowing spouse married the borrower when the reverse mortgage was taken out.

Why This Matters

Including your spouse in the reverse mortgage process is essential, even if they are not listed on the loan. By discussing these protections with your lender and HUD-approved counselor, you can ensure that both you and your spouse are prepared and secure.

Proactive Steps to Take

- Involve Your Spouse Early: Make sure your spouse participates in all discussions about the reverse mortgage.

- Understand the Rules: Ask your lender about non-borrowing spouse protections and how they apply to your specific situation.

- Include Your Spouse in the Contract: Whenever possible, ensure your spouse is included to avoid potential issues in the future.

These steps can help protect your spouse’s right to remain in the home, giving you both peace of mind as you move forward with a reverse mortgage.

#5. Payment Options for Reverse Mortgages

When choosing a reverse mortgage, homeowners with an adjustable interest rate can select from several flexible payment options. Each option is designed to fit different financial needs and goals:

Payment Options for Adjustable Interest Rate Loans

- Line of Credit:

- Withdraw funds as needed, either in scheduled installments or unscheduled payments at your discretion.

- Offers flexibility to cover unexpected expenses or ongoing needs.

- Modified Tenure:

- Combines a line of credit with steady monthly payments for as long as at least one borrower lives in the home.

- Modified Term:

- Similar to Modified Tenure, but the monthly payments are made for a specific, predetermined number of months.

- Tenure:

- Provides fixed monthly payments for as long as one borrower continues to live in the home.

- Term:

- Offers monthly payments for a set period, defined in months, based on your preferences and financial plans.

Payment Options for Fixed-Interest Rate Loans

- Lump Sum Payment:

- Funds are disbursed as a single payment at the loan’s closing, giving you immediate access to your equity.

Popular Choices

The line of credit and tenure options are among the most popular for their flexibility and reliability, allowing homeowners to customize how they access their home equity.

Maximizing Retirement Income

For older homeowners looking to supplement their retirement income, a reverse mortgage can be a powerful tool. By leveraging your home equity, you can cover essential expenses, enhance financial security, or address unexpected needs — all while staying in your home.

WARNING: Serious Consequences for Breaking These 3 Reverse Mortgage Rules

A reverse mortgage can be a powerful financial tool, but there are critical rules you must follow to keep your loan in good standing. Breaking these rules can have serious consequences, including the loan becoming due and payable. Here’s what you need to know:

1. Occupancy

- You must live in the home as your primary residence.

- If you permanently move out or leave the home for more than 12 consecutive months (e.g., to an assisted living facility or nursing home), the loan must be repaid.

2. Tax and Insurance Obligations

- You’re required to pay property taxes and maintain an active homeowner’s insurance policy.

- Failing to meet these obligations will result in the loan becoming due, potentially putting your home at risk.

3. Maintaining the Home

- The property must be kept in good condition to meet the loan servicer’s requirements.

- This includes regular maintenance to ensure the home doesn’t deteriorate, protecting its value for you and the lender.

By following these guidelines, you can avoid the risk of foreclosure and continue enjoying your home throughout retirement.

Top FAQs

What are the basic rules of a reverse mortgage?

What happens when someone dies with a reverse mortgage?

What are some specific requirements for reverse mortgages in California?

What are some specific requirements for reverse mortgages in Texas?

What are some specific requirements for reverse mortgages in Florida?

Ready to Unlock Your Home’s Equity? Get a free, custom quote from All Reverse Mortgage, Inc. (ARLO™) — America’s #1 Rated Lender with a 4.99/5-star rating! Call (800) 565-1722 or click here for your free quote — simple, trusted, 100% secure!

August 1st, 2024

August 6th, 2024

August 6th, 2024

April 6th, 2024

April 8th, 2024

September 2nd, 2022

September 6th, 2022

August 7th, 2021

August 10th, 2021

June 16th, 2021

June 18th, 2021

June 1st, 2021

June 2nd, 2021

November 25th, 2020

November 26th, 2020

September 14th, 2020

September 14th, 2020

November 17th, 2019

November 25th, 2019