|

Michael G. Branson, CEO of All Reverse Mortgage, Inc., and moderator of ARLO™, has 45 years of experience in mortgage banking, with the past 20 years devoted exclusively to reverse mortgages. A Forbes Real Estate Council member, he developed the industry's first fixed-rate jumbo reverse mortgage and has been featured in Forbes, Kiplinger, the LA Times, and Yahoo Finance. (License: NMLS# 14040) |

|

Cliff Auerswald, President of All Reverse Mortgage, Inc., and co-creator of ARLO™ — the industry's first real-time reverse mortgage pricing engine — has 27 years of experience in mortgage banking, with 20+ years focused exclusively on reverse mortgages. A recognized expert in reverse mortgage technology and consumer education, he has been featured in Kiplinger, Yahoo Finance, Realtor.com, and HousingWire. (License: NMLS# 14041) |

Why Reverse Mortgages Have 2 Notes & 2 Trust Deeds — The 150% Rule Explained

Borrowers often experience confusion as they approach the final step of signing their reverse mortgage documents. They are introduced to a First and Second Trust Deed Note and Two Deeds of Trust (or mortgages, depending on the applicable state laws for the property).

Complicating matters, the amounts specified in the Note and Deed of Trust can be substantially higher than the amount the borrowers agreed to borrow. This discrepancy has led some borrowers to hesitate or even refuse to sign the closing documents, primarily because they were not previously informed of the existence of multiple documents and the discrepancies in the stated amounts.

In this article, we aim to clarify the rationale for the requirement of two deeds and two notes in the reverse mortgage process. Understanding the need for multiple documents and the rationale for the differing amounts can significantly ease borrowers’ concerns.

Continue reading to explore the intricacies of these requirements and how they serve to protect the interests of all parties involved in a reverse mortgage transaction.

How Reverse Mortgages Are Recorded

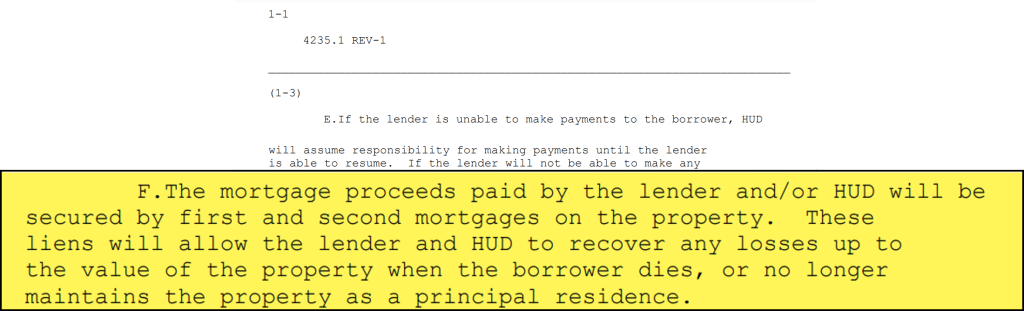

When reading the manual on reverse mortgages, HUD explains that every reverse mortgage shall have both a First and Second Note, and while the borrower does not have to receive a copy of the Second Note before closing, its existence and relationship should be fully explained to the borrower (and thus this explanation to you).

The Second Note is not a separate loan encumbering the property as a traditional first and second loan. Instead, it secures any payments HUD makes to the borrower under the borrower’s reverse mortgage. It “picks up,” if you will, where payments to the borrower, or on the borrower’s behalf, by the lender left off, and where HUD payments begin.

HUD Uses the Second Note for Your Protection

HUD can step into a reverse mortgage in a couple of instances and may advance funds on the borrower’s behalf. If the lender cannot make payments under the Loan Agreement, HUD would step in to ensure the borrower is paid.

When a lender becomes insolvent, and borrowers rely on their reverse mortgage funds, HUD steps in and pays those funds to borrowers. This is one reason reverse mortgages carry insurance.

HUD requires lenders to assign loans to them when the loan-to-value ratio reaches 95%. From then on, HUD would make all future advances to the borrowers and may sometimes have to advance funds for taxes or insurance.

The second Note and Deed of Trust ensure that HUD’s position is protected in these circumstances, allowing it to continue making any necessary advances to borrowers without the security it could not otherwise obtain.

How the HECM Note & Deed Are Calculated

Next is the issue of the loan amount listed on the documents. HUD does not require a maximum mortgage amount to be stated on the mortgage because no payments are required. Many reverse mortgages include growth features in the available lines, and the balance owed increases when borrowers make no payments.

However, most states require that an amount be stated on the documents, creating a dilemma for HUD. They cannot simply state the beginning balance, as is the case with a typically amortizing loan, or where a borrower’s borrowing power may increase with a growth rate on the line of credit, or no amounts higher than this balance could be advanced to or on behalf of the borrower.

In cases such as tenure loans (payments for life), where borrowers live in the home longer than the anticipated timeframe, this would result in an abrupt stoppage of payments, which would be unsuitable for borrowers who rely on those monthly payments to live. Also, as with a line of credit that grows over time on the unused portion, HUD states that a maximum amount set at the beginning balance would prevent borrowers from using the line’s growth balance.

For this reason, the amount you will see on the Note and Deed (or Mortgage) will equal 150% of the Maximum Claim Amount, the total value of the property, or the HECM Lending Limit, whichever is less.

For example, if your home is worth $200,000, then the amount on the Deed would be $300,000 ($200,000 x 150%). If your home is worth $800,000, the amount on the Deed would currently be $1,200,000, and if your home value were to be at or above the current lending limit of $1,249,125, the amount on the deed would be $1,249,125 x 150%.

Bottom Line: You Only Owe What You Borrow

This concept is the same as a Home Equity Line of Credit (HELOC). When you close the loan, you sign documents for the entire amount. Still, you only have to repay the amount you borrow plus interest on that amount, not the entire line, if you use only some of it. The key difference is that with a reverse mortgage, there is an additional Note and Deed if HUD must also advance funds.

But it’s still the same — you only repay what you borrow plus the fees and interest that you financed (and any funds that the lender or HUD have to advance on your behalf, such as taxes, insurance, etc., if those are not paid in a timely manner).

So these are the things you need to know about reverse mortgage documents before it’s time to sign:

- There will be 2 Notes and 2 Deeds of Trust (or Mortgages).

- They do not secure a First and Second Lien. The second Note and Deed secure only any advances HUD may make to you after the lender stops and HUD begins.

- The loan amount on the documents will either be blank, total 150% of your property value or 150% of the HUD Lending Limit, whichever is less, depending on the state in which you live and their laws affecting the mortgage documents, but if an amount is stated, it will be higher than the amount of cash you are receiving at the close.

Regardless of the amount stated on the loan documents, just like HELOC documents, you only owe what you borrow plus applicable interest, mortgage insurance, financing fees, and any amounts the lender or HUD has to advance on your behalf.

You will receive a sample copy of the Note, the Deed of Trust, or the Mortgage and Security Agreement in your loan package. If you have any questions, please do not hesitate to ask so that you are not surprised at your closing.

Top FAQs

Why are there two deeds of trust on a reverse mortgage?

A reverse mortgage has two deeds of trust because it involves two parties. One secures the amount owed to the lender. The second secures any funds that HUD may advance on your behalf.

HUD insures the HECM program. If they ever have to step in and pay property charges like taxes or insurance for you, those advances are tracked separately. That is why you see two documents. It is simply a matter of how the loan is structured and insured.

Who holds the deed on a reverse mortgage?

You do.

A reverse mortgage does not transfer ownership to the lender. Your name stays on the title just like it would with any other mortgage. The lender records a lien against the property to secure repayment, but you remain the owner.

Does a reverse mortgage have a note?

Yes. In fact, there are two notes.

The first note is between you and the lender. The second note relates to HUD’s insurance backing. The HUD note would only increase if HUD had to advance funds on your behalf. For example, if property taxes or insurance were unpaid and HUD intervened, those amounts would be added to the HUD account.

Most borrowers never see activity on the second note. It exists because the loan is federally insured.

Can you transfer the deed if you have a reverse mortgage?

Yes, but there are important rules.

You can add someone to the title. You can remove someone from title. The loan remains in place as long as at least one original borrower remains on title and continues to live in the home as their primary residence.

You can also sell the home at any time with no prepayment penalty.

However, if all original borrowers leave the property or are removed from title, the loan becomes due and payable. That is the key point to understand.

Does a reverse mortgage show up on the title?

Yes.

Just like any mortgage, it is recorded with the county recorder’s office. Anyone pulling the title will see the lien. That is completely normal.

Can you get a second mortgage after getting a reverse mortgage?

The reverse mortgage itself does not prohibit secondary financing.

That said, most lenders are reluctant to place a second lien behind a reverse mortgage. Because the reverse mortgage balance grows over time if no payments are made, it creates risk for a second lender.

It is possible, but not common.

Is there a waiting period after putting the deed in my name before I can get a reverse mortgage?

No.

If you own the home and it is your primary residence, there is no minimum ownership period required. As long as you meet the age and property requirements, you can apply right away.

Have Questions About Your Reverse Mortgage Documents? Get clear answers from All Reverse Mortgage, Inc. (ARLO™) — America’s #1 Rated Lender with a 4.99/5-star rating! Call (800) 565-1722 or click here for your free quote — simple, trusted, 100% secure!

ARLO recommends these helpful resources:

Have a Question About Reverse Mortgages?

Over 2000 of your questions answered by ARLO™

Ask your question now!

November 7th, 2024

November 7th, 2024

March 22nd, 2024

March 25th, 2024

December 26th, 2023

December 28th, 2023

December 8th, 2023

December 8th, 2023

November 24th, 2023

December 4th, 2023

November 22nd, 2023

November 22nd, 2023

September 29th, 2023

September 29th, 2023

August 30th, 2023

September 3rd, 2023

July 13th, 2023

July 14th, 2023

June 9th, 2023

June 9th, 2023

May 2nd, 2023

May 6th, 2023

October 24th, 2022

October 30th, 2022

October 4th, 2022

October 4th, 2022

September 6th, 2022

September 6th, 2022

April 2nd, 2022

April 2nd, 2022

January 25th, 2021

January 25th, 2021

November 11th, 2020

November 11th, 2020

October 22nd, 2020

October 22nd, 2020

June 25th, 2020

June 26th, 2020

June 2nd, 2020

June 3rd, 2020

April 20th, 2020

April 20th, 2020

March 15th, 2020

March 19th, 2020

March 9th, 2020

March 9th, 2020

August 25th, 2019

August 25th, 2019

March 30th, 2019

March 30th, 2019

January 1st, 2019

January 2nd, 2019

June 7th, 2024

June 8th, 2024

February 11th, 2017

February 13th, 2017

November 10th, 2016

June 21st, 2012

April 25th, 2012