Reverse Mortgage Calculator

|

Michael G. Branson, CEO of All Reverse Mortgage, Inc., and moderator of ARLO™, has 45 years of experience in mortgage banking, with the past 20 years devoted exclusively to reverse mortgages. A Forbes Real Estate Council member, he developed the industry's first fixed-rate jumbo reverse mortgage and has been featured in Forbes, Kiplinger, the LA Times, and Yahoo Finance. (License: NMLS# 14040) |

|

Cliff Auerswald, President of All Reverse Mortgage, Inc., and co-creator of ARLO™ — the industry's first real-time reverse mortgage pricing engine — has 27 years of experience in mortgage banking, with 20+ years focused exclusively on reverse mortgages. A recognized expert in reverse mortgage technology and consumer education, he has been featured in Kiplinger, Yahoo Finance, Realtor.com, and HousingWire. (License: NMLS# 14041) |

Reverse mortgage proceeds run from roughly 35% of a home's value at age 62 to more than 60% at age 90. Three factors set the amount: the age of the youngest borrower, the home's value, and current interest rates. The FHA-insured HECM calculates on home value up to $1,249,125. Homes worth more qualify under our jumbo programs, which lend up to $4 million.

A reverse mortgage calculator estimates how much equity a homeowner aged 62 or older can access through a HECM or jumbo reverse mortgage. Results are based on age, home value, ZIP code, existing mortgage balance, and current interest rates.

Most reverse mortgage calculators are run by lead-generation sites — not the lender who would actually fund your loan. All Reverse Mortgage is a HUD-approved direct lender (NMLS #13999), so your numbers come straight from ARLO™, the same pricing engine our loan officers use to quote. You’ll see today’s real rates and the actual title, appraisal, and recording fees for your ZIP code — not a rough estimate. What you see is what we’d actually quote you today.

No personal information required. The calculator does not ask for your Social Security number, does not pull your credit, and does not require contact information to view results. You see your full numbers on screen — name, email, and phone are never required.

How Our Calculator Is Different from Other Free Tools

Most online reverse mortgage calculators return a generic loan-to-value estimate based on national-average assumptions. Real numbers depend on your ZIP code, current daily pricing, the lender’s margin tied to today’s index, and the specific fees in your state.

Our calculator pulls all of those in real time:

- Real-time interest rates and APR — updated daily for both fixed and adjustable options.

- ZIP-code-accurate closing costs — actual title, appraisal, and recording fees for your state and county, not national estimates.

- HECM and Jumbo side-by-side — see how payouts, rates, and costs differ across HUD-insured and proprietary programs for higher-value homes.

- Goal-based comparison views — isolate the program that best matches your goals of maximizing proceeds, preserving equity, or minimizing closing costs.

- Full amortization schedule — see how the loan balance and your remaining equity change year by year.

Direct Lender Calculator vs. a Lead Generation Calculator

| What matters | All Reverse (direct lender) | Typical lead-gen calculator |

|---|---|---|

| Who's behind the numbers | HUD-Approved lender that would fund your loan (HUD lender ID #26031-0007) | A marketing site that sells your info to lenders |

| Where the rates come from | ARLO™ — the live pricing engine our underwriters quote from | National-average assumptions |

| Closing costs | Actual title, appraisal & recording fees for your ZIP | Generic estimate, if shown at all |

| Your contact info | Never required to see results — no name, email, or phone | Often required before any number appears |

| HECM + Jumbo | Both, side by side | Usually HECM only |

How to Use the Calculator

- Enter your ZIP code and click “Show My Options.” The calculator pulls the $1,249,125 HUD lending limit and state-specific fees for your area.

- Enter your street address and click “Look Up My Home.” ARLO™ retrieves your home’s estimated value from public property records (provided by Estated.com) — no credit check and no commitment.

- Confirm your home value. The starting estimate comes from public data, but you can adjust it up or down since automated valuations are not always accurate; a HUD-approved appraisal confirms the final value if you move forward. Enter any existing mortgage balance, then click “Calculate My Options.”

- Add your date of birth (and your spouse’s if married). Age is one of the largest factors in how much you qualify for. Borrowers within six months of their next birthday round up. Click “See My Options.”

- Review your results. You can adjust any input as many times as you want. If you would like a copy emailed to you, add your contact information — but this step is optional. Results are visible without it.

What Your Results Show

As soon as you finish, ARLO™ displays a personalized summary at the top: your estimated home value, the maximum equity you can access, any required mortgage payoff, and the number of programs you qualify for. Below that, ARLO™ gives a plain-English recommendation for your situation — for example, on a higher-value home it shows in dollars how a jumbo reverse mortgage compares to a standard HECM. A full comparison table then lists every eligible program side by side with the total funds available, mortgage payoff, net cash to you, and the interest rate for each. From the same screen you can open the line-of-credit draw options or the year-by-year amortization schedule, change any input, and re-run as many scenarios as you like — all without entering a name, email, or phone number.

Compare Reverse Mortgage Options Side by Side

The calculator runs multiple scenarios at once so you can decide which option fits your retirement plan. You can model lump-sum payouts, term payments, and line-of-credit options with a growth rate, then compare each against the others.

Three quick-view tabs isolate the product best matched to a specific goal:

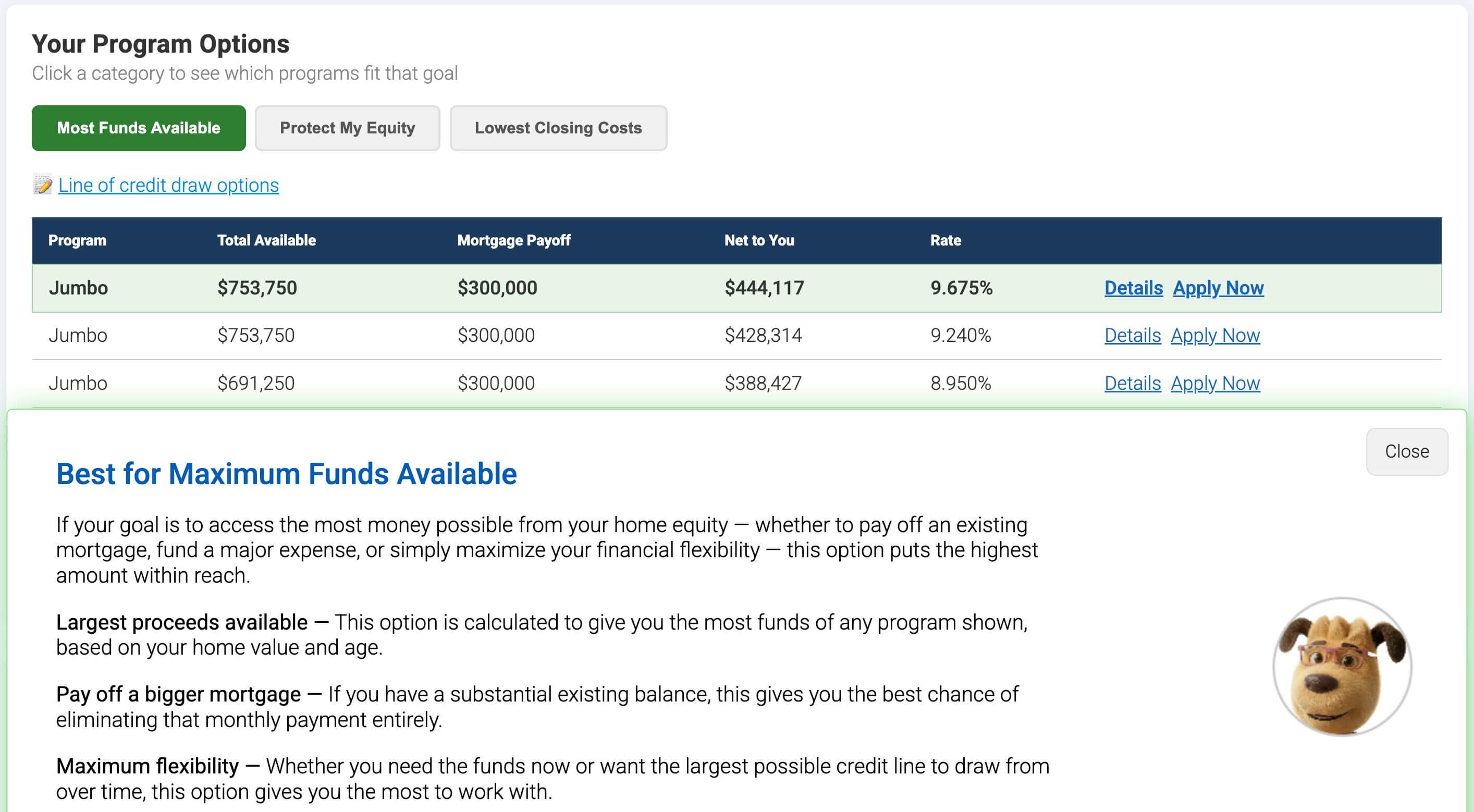

1. Most Funds Available

Shows the product that delivers the largest cash payout at closing. This is typically the right view if you need to pay off an existing mortgage, eliminate consumer debt, or fund a major expense like a home renovation. Maximum-payout products often use a fixed rate with a full draw, which means giving up the line-of-credit growth feature available on adjustable options.

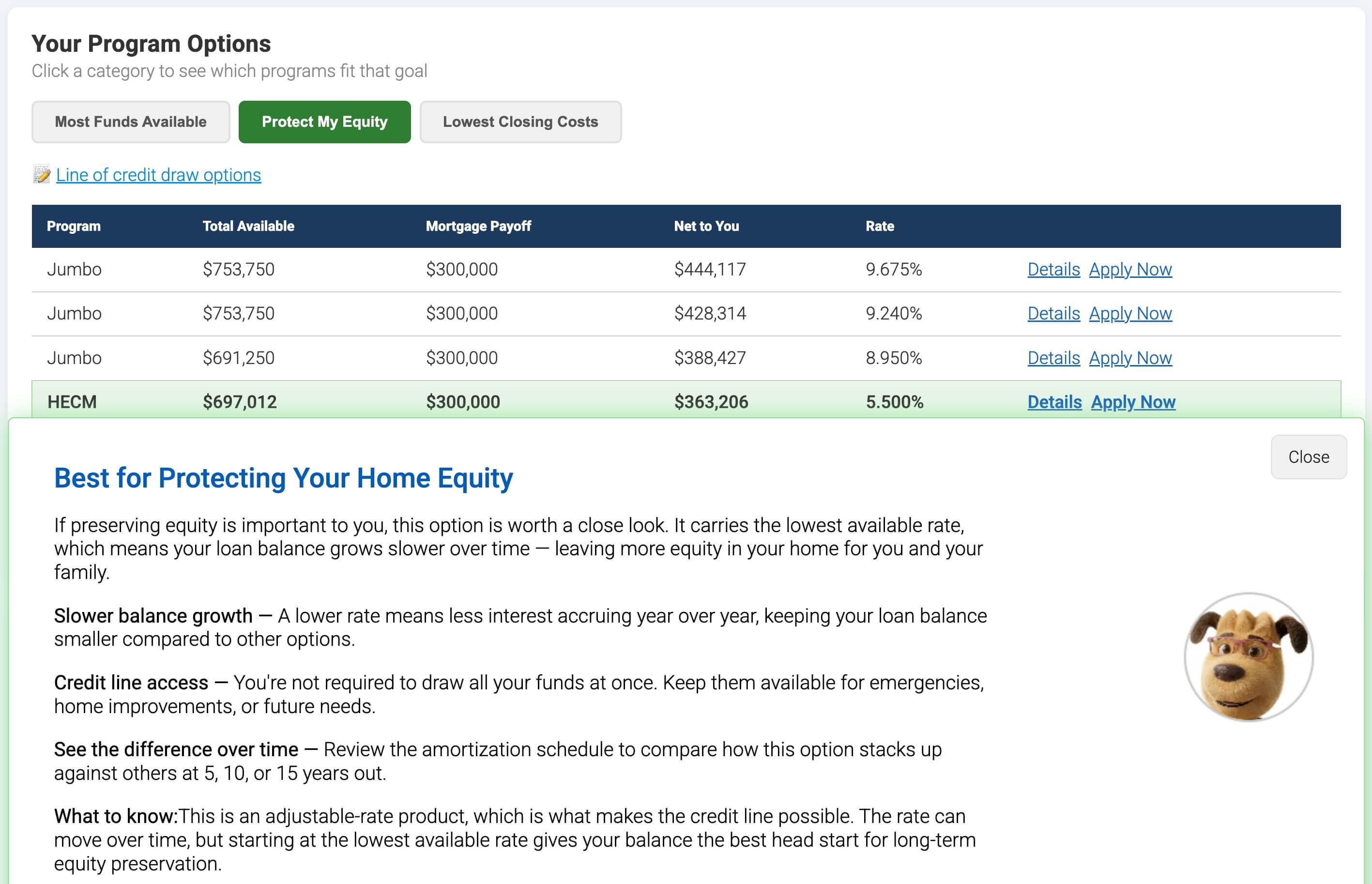

2. Protect My Equity

Shows the product with the lowest starting interest rate currently available. A lower rate means slower balance growth, which preserves more equity in the home for you and your heirs. This is the right view if you want access to funds in the future but want to retain as much equity as possible. Open the amortization schedule to see year-by-year how much equity stays intact.

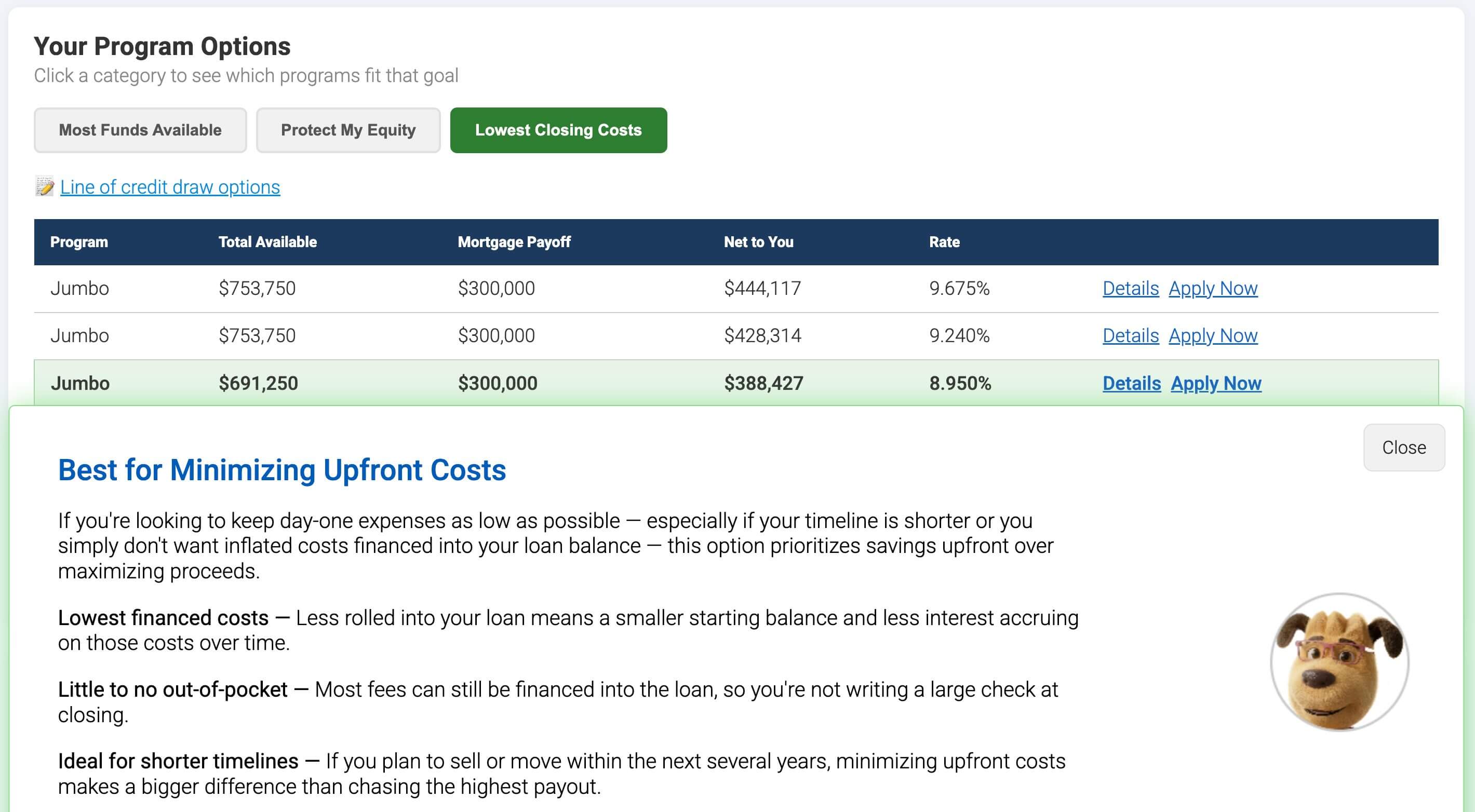

3. Lowest Closing Costs

Shows the product with the smallest upfront fees. This view prioritizes keeping closing costs down over maximizing proceeds. It is usually the right choice if you have a shorter timeline for keeping the loan in place. Compare the closing-cost savings against the smaller payout to make sure the math still works for your situation.

When a Reverse Mortgage May Not Be the Right Choice

Qualifying for a reverse mortgage does not always mean the loan is the right move. There are situations where another option is better:

- Short-term plans for the home. If you may sell or move within a few years, the upfront costs of a reverse mortgage rarely pay off. A HELOC or short-term financing often makes more sense.

- Heirs who want to keep the home. Heirs can keep the property, but they will need to pay off the loan balance, typically by refinancing. Have that conversation before you apply.

- Difficulty keeping up with property charges. A reverse mortgage requires you to stay current on property taxes, homeowners insurance, and maintenance. If those payments are already a struggle, a financial assessment set-aside may be required.

- Means-tested benefits. Loan proceeds are not income, but funds left in the bank can affect Medicaid and SSI eligibility. Talk to a benefits specialist before drawing a large lump sum.

- Limited equity. If your existing mortgage balance is close to your home’s value, the proceeds may not be enough to make the upfront costs worthwhile.

HUD requires independent counseling before any HECM closing. Every borrower completes a session with a HUD-approved counselor who walks through alternatives, costs, and obligations with no pressure to proceed. Learn more about HECM counseling.

Frequently Asked Questions

Is the reverse mortgage calculator free to use?

Do I need to provide my Social Security number?

Does using the calculator affect my credit?

How accurate are the results?

What if I am under age 62?

What information do I need to use the calculator?

How much can I borrow with a reverse mortgage?

What rates does the calculator use?

What is a tenure payment vs a term payment?

Can the calculator also be used for a refinance or home purchase?

“All Reverse Mortgage offered the clearest calculator with detailed results immediately. Their rates were lower, and their team quickly answered all our questions. Highly recommended!” — Peter H., Verified BBB Review

Important: Calculator results are estimates based on current pricing and the information you provide. They are not a loan commitment. A formal quote and final loan terms require a complete application and underwriting review.

See your real numbers above using the reverse mortgage calculator, or call (800) 565-1722 to speak with a specialist. All Reverse Mortgage, Inc. is America’s #1 rated HUD-approved direct reverse mortgage lender, with 20+ years of experience and a 4.9/5 customer satisfaction rating.

Other Reverse Mortgage Calculators

For specialized scenarios, see our companion tools:

- Line of Credit (LOC) Calculator — projects HECM credit line growth over time.

- HECM-to-HECM Refinance Calculator — checks whether refinancing your existing HECM passes the 5x net tangible benefit test.

- HECM for Purchase Calculator — estimates down payment for buying a home with a reverse mortgage.

- Amortization Calculator — downloadable year-by-year loan balance and equity projection.