Reverse Mortgages in The Villages

|

Michael G. Branson, CEO of All Reverse Mortgage, Inc., and moderator of ARLO™, has 45 years of experience in mortgage banking, with the past 20 years devoted exclusively to reverse mortgages. A Forbes Real Estate Council member, he developed the industry's first fixed-rate jumbo reverse mortgage and has been featured in Forbes, Kiplinger, the LA Times, and Yahoo Finance. (License: NMLS# 14040) |

|

Cliff Auerswald, President of All Reverse Mortgage, Inc., and co-creator of ARLO™ — the industry's first real-time reverse mortgage pricing engine — has 27 years of experience in mortgage banking, with 20+ years focused exclusively on reverse mortgages. A recognized expert in reverse mortgage technology and consumer education, he has been featured in Kiplinger, Yahoo Finance, Realtor.com, and HousingWire. (License: NMLS# 14041) |

The Villages: America’s Unique Reverse Mortgage Market

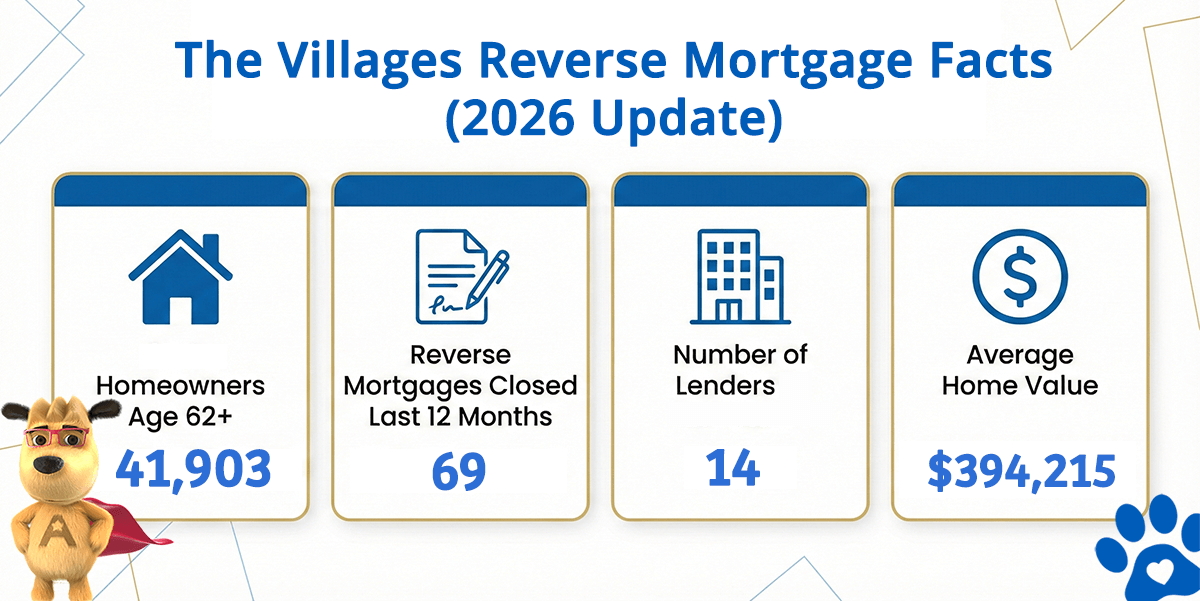

The Villages Reverse Mortgage Facts (2026 Update)

| City | Homeowners Age 62+ | Reverse Mortgages Closed Last 12 Months | Active Lenders | Avg. Home Value |

|---|---|---|---|---|

| The Villages | 41,903 | 69 | 14 | $394,215 |

Understanding The Villages Reverse Mortgage Opportunity

The Villages stands uniquely as America’s largest age-restricted retirement community, a master-planned world spanning Sumter, Lake, and Marion counties explicitly designed for residents 55 and older. With 41,903 households virtually all headed by residents 62 and older, The Villages represents an unparalleled concentration of age-qualified borrowers. The average home value of $394,215 places most residents comfortably within the FHA ceiling of $1,249,125, making conventional HECM products accessible to the vast majority. With 69 loans executed in the past 12 months across 14 active lenders, The Villages clearly demonstrates how reverse mortgages align with intentional retirement community living designed to maximize active-adult lifestyles.

The Villages’ residential design is entirely engineered around 55+ lifestyles. Three championship golf courses, executive courses, par-3 courses, and driving ranges weave through the community. Golf-cart culture enables car-free living along 2,000+ miles of paths and roads. Neighborhoods like Pinewood and Hacienda Heights feature newer homes (2010s-2020s) with modern construction standards, while Penrose and Laurel Park include established 1990s-2000s homes. Each village has its own recreation center, multiple pools, bocce courts, shuffleboard, and social programming. Medical centers, pharmacies, and healthcare services cater specifically to aging residents. The infrastructure is entirely age-appropriate—accessible design, proximity-based walkability, and leisure-focused amenities unmatched in conventional communities. This means Villages residents represent people who explicitly paid premiums for age-restricted living and amenity-rich retirement, then seek reverse mortgages to maximize the active lifestyle they purchased into.

The Villages economy is distinct: The Villages Company, the master developer, is the primary employer and economic engine. Real estate, community management, recreation programming, golf course maintenance, and hospitality employ thousands of team members. Retail and service businesses—restaurants, golf shops, fitness centers, spas—depend entirely on Villages resident spending. Some residents maintain encore careers with regional employers in Ocala and Orlando. Travel clubs, social organizations, and leisure activities drive significant discretionary spending. The fundamental economic fact about Villages residents is that they’re retirement-focused by definition and brought accumulated wealth and home equity when they relocated. Reverse mortgage borrowers here are almost universally in strong financial positions, seeking to optimize retirement income while funding the golf, travel, family connection, and active experiences they explicitly chose through HECM for Purchase programs or equity refinancing to support Villages lifestyle maximization.

How a Reverse Mortgage Works for The Villages Homeowners

A reverse mortgage is a loan secured by your home that allows homeowners age 62 and older to convert a portion of their equity into usable funds. The most common type is the Home Equity Conversion Mortgage (HECM), which is insured by the Federal Housing Administration and regulated by HUD.

With a HECM, you retain full ownership of your home. No monthly mortgage payments are required as long as you continue living in the property, maintain it, and stay current on property taxes and homeowners insurance. The loan balance is repaid when you sell, move out permanently, or pass away — and FHA insurance guarantees you will never owe more than the home is worth.

How Villages Residents Use Reverse Mortgages

- Maximizing golf memberships, club access, and recreational pursuits without reducing fixed income

- Supporting grandchildren’s education and hosting extended family stays within the community

- Funding home accessibility modifications for long-term aging within Villages homes and neighborhood culture

- Maintaining flexible access to growing credit lines for travel clubs, cruises, and extended family experiences

The Villages Reverse Mortgage Eligibility

| Requirement | Details |

|---|---|

| Age | 62 or older (at least one borrower) — virtually all Villages residents meet this requirement |

| Property | Primary residence — single-family home or approved dwelling within The Villages master-planned community |

| Equity | Sufficient equity in the home (typically 50% or more) |

| Counseling | Counseling through a HUD-approved agency is mandatory before application submission |

| Financial Assessment | Lender evaluates income, credit history, and ability to maintain property obligations |

Villages residents can get a quick estimate of their reverse mortgage options — just enter your home’s approximate value and your age.

Understanding Program Expenses

Reverse mortgages incorporate origination fees, FHA insurance premiums, third-party settlement costs, and accruing interest. Structurally similar to traditional refinancing, with one critical advantage: most expenses can be incorporated into the loan balance rather than paid upfront.

For a detailed breakdown, review our resources on cost breakdown and benefits and drawbacks to understand the full program implications for Villages borrowers.

Is a Reverse Mortgage Appropriate for Your Situation?

Reverse mortgages suit homeowners planning permanent residency who want enhanced cash flow, an enriched lifestyle, access to travel, or flexible financial reserves. They don’t suit those expecting to relocate soon or who prioritize preserving maximum equity for heirs above all other goals.

For comprehensive information, explore our resources on the complete process from application to closing and how the loan resolves for your heirs to understand the full implications.

HUD-Approved Direct Lender Serving The Villages

All Reverse Mortgage, Inc. (ARLO) is a HUD-approved direct lender — not a broker or lead generator. We originate, process, and fund reverse mortgages in-house, giving Villages homeowners a single point of contact from first conversation through closing.

You can verify our credentials through the HUD lender lookup tool or review our BBB profile, which reflects more than two decades of client feedback. For homeowners whose property value exceeds FHA limits, we also offer jumbo reverse mortgage programs with no mortgage insurance requirement.

All Reverse Mortgage, Inc. is fully licensed by the Florida Office of Financial Regulation (License #MLD874), ensuring that you receive expert guidance every step of the way.

Get a Reverse Mortgage Quote for Your Villages Home

ARLO™ generates personalized quotes with today’s rates — completely confidential, no data sharing necessary.

Related Resources

HECM for Purchase lets you buy in The Villages without monthly payments