Reverse Mortgages in Portland

|

Michael G. Branson, CEO of All Reverse Mortgage, Inc., and moderator of ARLO™, has 45 years of experience in mortgage banking, with the past 20 years devoted exclusively to reverse mortgages. A Forbes Real Estate Council member, he developed the industry's first fixed-rate jumbo reverse mortgage and has been featured in Forbes, Kiplinger, the LA Times, and Yahoo Finance. (License: NMLS# 14040) |

|

Cliff Auerswald, President of All Reverse Mortgage, Inc., and co-creator of ARLO™ — the industry's first real-time reverse mortgage pricing engine — has 27 years of experience in mortgage banking, with 20+ years focused exclusively on reverse mortgages. A recognized expert in reverse mortgage technology and consumer education, he has been featured in Kiplinger, Yahoo Finance, Realtor.com, and HousingWire. (License: NMLS# 14041) |

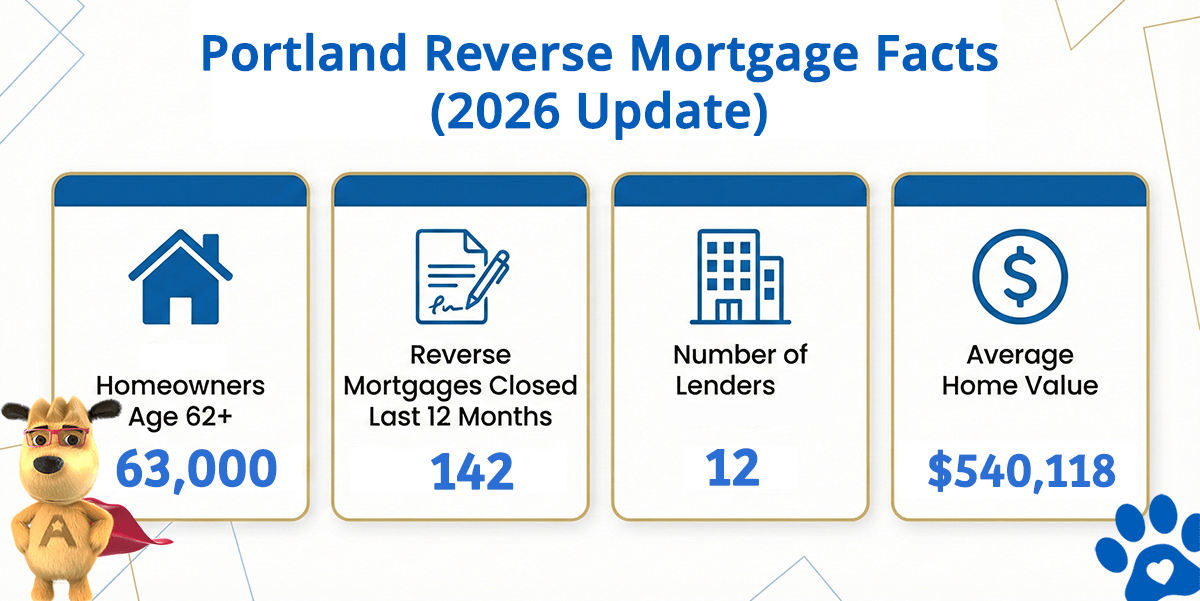

Portland Reverse Mortgage Market at a Glance

Portland Reverse Mortgage Facts (2026 Update)

| City | Homeowners Age 62+ | Reverse Mortgages Closed Last 12 Months | Lenders in Portland (est) | Avg. Home Value |

|---|---|---|---|---|

| Portland | 63,000 | 142 | 12 | $540,118 |

What the Numbers Tell Us About Reverse Mortgages in Portland

Portland is Oregon’s largest city, with approximately 63,000 homeowners aged 62 and older and an average home value near $540,000. The city’s diverse neighborhoods, from the historic homes of Irvington and Laurelhurst to the bungalows of Southeast Portland, represent decades of sustained appreciation that has left many long-term residents equity-rich on paper but cash-constrained in retirement.

At the FHA lending limit of $1,249,125, most Portland properties qualify for a standard HECM. Rising Multnomah County property taxes, Oregon’s income tax burden, and general cost-of-living increases can strain fixed retirement incomes, creating a gap between home wealth and available cash flow that a reverse mortgage can help bridge.

How a Reverse Mortgage Works for Portland Homeowners

A reverse mortgage is a loan secured by your home that allows homeowners age 62 and older to convert a portion of their equity into tax-free funds without making monthly mortgage payments. The most common type is the Home Equity Conversion Mortgage (HECM), insured by the Federal Housing Administration and regulated by HUD since 1989.

The loan becomes due when the last borrower permanently leaves the home, whether through sale, relocation, or passing. Until then, borrowers retain full title and may continue living in the property as long as they meet standard obligations: property taxes, homeowners insurance, and home maintenance.

Common Uses in Portland

- Eliminating an existing mortgage payment — Particularly valuable for Portland retirees managing Multnomah County property taxes, Metro bonds, and Oregon income tax on fixed retirement incomes.

- Establishing a growing credit line — A reverse mortgage line of credit serves as a strategic reserve for healthcare, home maintenance, or long-term care that grows over time regardless of home value fluctuations.

- Purchasing a new home in retirement — Some borrowers use a HECM for Purchase to relocate within the Portland metro without taking on monthly mortgage payments.

- Supplementing retirement income — Access home equity to maintain quality of life in one of Oregon’s most vibrant cities without selling a home that has appreciated significantly over decades.

Portland Reverse Mortgage Eligibility

| Requirement | Details |

|---|---|

| Age | 62 or older (both spouses if applicable) |

| Property | Primary residence — single-family home, townhome, FHA-approved condo, or 2–4 unit (owner-occupied) |

| Equity | Substantial equity required (typically 50% or more) |

| Counseling | HUD-approved reverse mortgage counseling session required before application |

| Financial Assessment | Lender evaluates income, credit history, and ability to maintain property taxes, insurance, and upkeep |

For a personalized estimate based on your Portland home value, try our free reverse mortgage calculator — no personal information required.

Understanding the Costs

Reverse mortgages carry upfront and ongoing costs including an origination fee, FHA mortgage insurance premium, and third-party closing costs. Most can be financed into the loan rather than paid out of pocket.

Because interest compounds over time, the loan balance grows, meaning more equity is used the longer the loan remains in place. A thorough review of the pros and cons helps ensure this tradeoff aligns with your goals.

Is a Reverse Mortgage Right for You?

A reverse mortgage works best for homeowners who plan to remain in their Portland home long-term, have substantial equity, and want to improve cash flow or eliminate existing mortgage payments during retirement. It may not be ideal if you plan to move within a few years or want to preserve maximum equity for heirs.

Our guide on how reverse mortgages work covers the full process from application through funding.

HUD-Approved Direct Lender Serving Portland

All Reverse Mortgage, Inc. (ARLO) is a HUD-approved direct lender specializing in reverse mortgages since 2004 with an A+ Better Business Bureau rating. We originate, process, and fund reverse mortgages in-house, giving Portland homeowners a single point of contact from first conversation through closing.

Portland’s wide range of home values across neighborhoods makes program selection critical. For homeowners whose properties exceed FHA limits in the West Hills, Dunthorpe, or Eastmoreland, we offer proprietary reverse mortgage programs with no mortgage insurance requirement.

All Reverse Mortgage, Inc. is licensed by the Oregon Division of Financial Regulation (License #ML-5006).

Get a Reverse Mortgage Quote for Your Portland Home

Use our calculator to see real-time rate data based on your home’s current market value and your age.

Related Resources