New Jersey's #1 Rated Reverse Mortgage

|

Michael G. Branson, CEO of All Reverse Mortgage, Inc., and moderator of ARLO™, has 45 years of experience in mortgage banking, with the past 20 years devoted exclusively to reverse mortgages. A Forbes Real Estate Council member, he developed the industry's first fixed-rate jumbo reverse mortgage and has been featured in Forbes, Kiplinger, the LA Times, and Yahoo Finance. (License: NMLS# 14040) |

|

Cliff Auerswald, President of All Reverse Mortgage, Inc., and co-creator of ARLO™ — the industry's first real-time reverse mortgage pricing engine — has 27 years of experience in mortgage banking, with 20+ years focused exclusively on reverse mortgages. A recognized expert in reverse mortgage technology and consumer education, he has been featured in Kiplinger, Yahoo Finance, Realtor.com, and HousingWire. (License: NMLS# 14041) |

New Jersey's average home value of $552,000 sits under the 2026 HECM limit, though Bergen County and Shore homes often exceed it. This page compares the top 20 New Jersey lenders and shows how a reverse mortgage works with the Senior Freeze and ANCHOR programs.

Experience Excellence with New Jersey’s Top Reverse Mortgage Lender

For over 20 years, All Reverse Mortgage, Inc. (ARLO™) has helped New Jersey homeowners access their home equity through HUD-approved HECM and jumbo reverse mortgages. As New Jersey’s #1 Rated Reverse Mortgage Lender, we hold an A+ BBB rating with perfect 5-star reviews and zero complaints — a record that earned us recognition as a BBB Torch Award for Ethics Finalist three years running.

As a HUD-approved direct lender and proud member of the National Reverse Mortgage Lenders Association (NRMLA), we specialize exclusively in reverse mortgages — it’s all we’ve done since 2004. That singular focus is especially valuable in New Jersey, where property values in Bergen County communities like Alpine, Saddle River, and Englewood Cliffs, along the Shore in Spring Lake, Bay Head, and Deal, and in sought-after suburbs like Short Hills, Summit, and Princeton regularly exceed the $1,249,125 HECM lending limit. Our team introduced the first fixed-rate jumbo reverse mortgage in 2008, giving us deep expertise in helping New Jersey homeowners with higher-value properties evaluate both HECM and jumbo options side by side.

Whether your goal is to eliminate monthly mortgage payments, create a financial safety net with a growing line of credit, or access equity for retirement planning, we’re here to help you choose the right program with competitive rates and lower costs. Let us show you the difference two decades of dedicated experience can make.

| Top 10 Reverse Mortgage Cities in New Jersey |

|---|

| 1 Jersey City |

| 2 Sea Girt |

| 3 Brick |

| 4 Bergenfield |

| 5 Tom’s River |

| 6 Asbury Park |

| 7 Cresskil |

| 8 Mountainside |

| 9 Millburn |

| 10 Point Pleasant |

| Data by MCA (January 2026) |

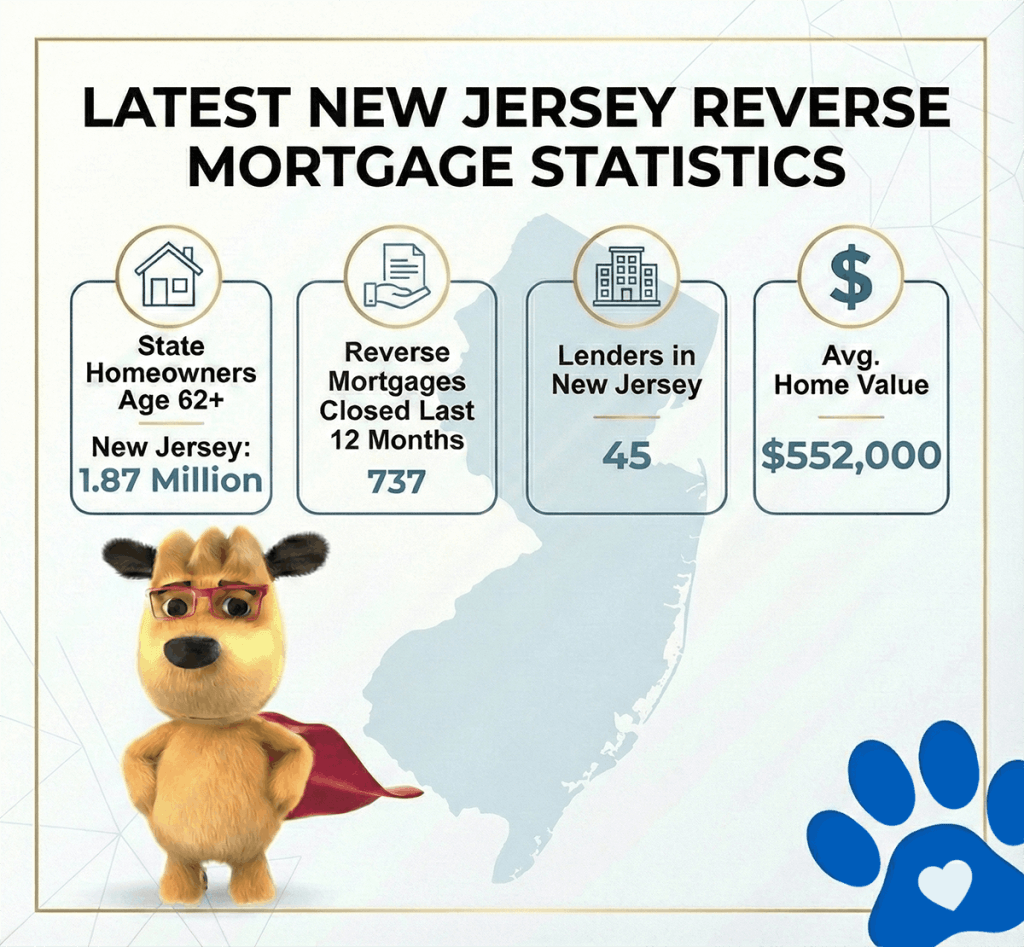

Latest New Jersey Reverse Mortgage Statistics

| State | Homeowners Age 62+ | Reverse Mortgages Closed Last 12 Months | Lenders in New Jersey | Avg. Home Value |

|---|---|---|---|---|

| New Jersey | 1.87 Million | 737 | 45 | $552,000 |

How this data was derived: Reverse mortgage counts reflect FHA-insured HECM loans endorsed over a rolling 12-month period (Dec 2024–Nov 2025) using HUD HECM Snapshot data. Active lenders represent unique FHA sponsor numbers with at least one endorsed loan during this period. Estimated homeowners age 62+ are based on U.S. Census ACS 5-year owner-occupied households age 65+ as a conservative proxy. Home values are sourced from Zillow’s Home Value Index (latest available).

Top Reverse Mortgage Lenders in New Jersey

| Lender | BBB Rating | Accredited | Years in Business | Customer Rating (0–5) | % Positive Reviews | Complaints | Source |

|---|---|---|---|---|---|---|---|

| All Reverse Mortgage, Inc. (ARLO) | A+ | YES | 21 | 4.94/5 | 99.0% | 0 | Source |

| American Pacific Mortgage | F | NO | 28 | 1.75/5 | 35.0% | 6 | Source |

| CrossCountry Mortgage, LLC. | F | YES | 22 | 1.43/5 | 29.0% | 303 | Source |

| Fairway Independent Mortgage | A+ | YES | 29 | 4.51/5 | 90.0% | 26 | Source |

| Finance of America Reverse LLC (FAR) | A+ | YES | 22 | 3.71/5 | 74.0% | 36 | Source |

| Goodlife Home Loans | A+ | YES | 13 | N/A (Not enough reviews) | N/A (Not enough reviews) | 1 | Source |

| Guaranteed Rate | A+ | YES | 26 | 2.25/5 | 45.0% | 45 | Source |

| Guild Mortgage Company LLC | A+ | NO | 65 | 1.55/5 | 31.0% | 73 | Source |

| HighTechLending Inc | A+ | YES | 19 | 4.94/5 | 99.0% | 1 | Source |

| Liberty Home Equity Solutions Inc. | A+ | NO | 22 | 1.00/5 | 20.0% | 1 | Source |

| Longbridge Financial LLC | A+ | YES | 13 | 3.77/5 | 75.0% | 34 | Source |

| Luminate Bank | NR | NO | 84 | NA | NA | NA | Source |

| MCM Holdings | A+ | YES | 27 | NA | NA | NA | Source |

| The Money House | NR | NO | 28 | NA | NA | 0 | Source |

| Movement Mortgage, LLC | A+ | NO | 18 | 4.43/5 | 89.0% | 92 | Source |

| Mutual of Omaha Mortgage | A+ | YES | 12 | 3.31/5 | 66.0% | 65 | Source |

| New American Funding | A+ | YES | 26 | 4.65/5 | 93.0% | 147 | Source |

| Plaza Home Mortgage Inc | A+ | YES | 24 | 2.67/5 | 53.0% | 6 | Source |

| Smartfi Home Loans | A+ | YES | 6 | N/A (Not enough reviews) | N/A (Not enough reviews) | 0 | Source |

| South River Mortgage, LLC | A+ | NO | 6 | 3.79/5 | 76.0% | 14 | Source |

New Jersey Reverse Mortgage Lending Limits

New Jersey, known as “The Garden State,” is home to nearly 9.3 million people, of whom over 1.87 million are homeowners aged 62 and older. This means that well over half a million New Jersey residents may qualify for a reverse mortgage, offering a way to access their home’s equity.

As of January 2026, the average home value in New Jersey is $552,000, which is comfortably below the HECM reverse mortgage lending limit of $1,249,125. This allows many homeowners to take advantage of their home’s value through a reverse mortgage.

New Jersey’s history is rich and storied, from its role as one of the original 13 colonies to General Washington’s famous crossing of the Delaware River in 1776. The state earned the nickname “the Crossroads of the American Revolution” and became the third state to ratify the U.S. Constitution and the first to ratify the Bill of Rights. Its prime location between New York and Philadelphia fueled industrial growth in the 19th century and suburban expansion in the 20th.

Today, New Jersey’s economy is driven by pharmaceuticals, finance, chemical development, telecommunications, and tourism. Atlantic City remains a popular destination for entertainment, while communities across the state — from the Jersey Shore to the Delaware Valley — attract retirees seeking to stay close to family while enjoying a lower cost of living than neighboring New York City.

If you’re a homeowner aged 62 or older in New Jersey, a reverse mortgage could be a valuable financial tool for your retirement. Whether you’re looking to eliminate monthly mortgage payments or access additional funds from your home’s equity, All Reverse Mortgage, Inc. (ARLO™) is here to help. We’re ready to answer your questions and guide you through the process.

Essential Protections for New Jersey Borrowers

New Jersey provides key consumer protections for reverse mortgage borrowers to ensure transparency and safeguard your interests. Here’s what you need to know:

- Mandatory HUD-Approved Counseling — Before applying for a reverse mortgage in New Jersey, you are required to complete a HUD-approved counseling session. This step ensures you fully understand the loan terms, potential risks, and alternative options.

- Prohibition on Tied Products — New Jersey law prohibits lenders from requiring you to purchase additional financial products, such as annuities or life insurance, as a condition for obtaining a reverse mortgage. This prevents unnecessary financial pressure during the process.

- Borrower Notifications — Lenders in New Jersey must provide clear written disclosures explaining the borrower’s obligations, including maintaining property taxes, homeowners insurance, and home upkeep. Failure to meet these obligations can result in loan default.

- Licensed and Regulated Lenders — Reverse mortgage lenders in New Jersey must be licensed and comply with the New Jersey Department of Banking and Insurance (DOBI) regulations. This ensures you are working with reputable professionals who meet strict consumer protection standards.

- Equity Preservation Protections — New Jersey has safeguards in place to ensure that borrowers or their heirs retain any remaining equity after the reverse mortgage is repaid. This non-recourse feature means you’ll never owe more than the home’s value at the time of repayment.

- Foreclosure Protections — In New Jersey, borrowers are protected by the state’s foreclosure process, which includes mandatory notices and opportunities to resolve defaults, such as unpaid taxes or insurance, before foreclosure proceedings begin.

Industry Update — February 2026: NRMLA has formally requested revisions to New Jersey Senate Bill 264, a proposed law that would require reverse mortgage counseling to be conducted in-person by a New Jersey–domiciled agency and would extend the rescission period to 7 days beyond the 3 days already mandated under federal law. In its letter to Senator Shirley K. Turner, NRMLA pointed out that only two HUD-approved counseling agencies in New Jersey currently offer reverse mortgage counseling — making the bill’s five-agency requirement impossible to meet. NRMLA also noted that requiring in-person sessions would create hardships for seniors with mobility limitations or language needs who currently have the right to choose telephone counseling under the federal HECM program. NRMLA has coordinated a letter-writing campaign with its New Jersey members to help ensure the bill is amended before advancing.

HUD-Approved Reverse Mortgage Counseling Agencies in New Jersey

| Name | Agency ID | Address | Phone | Web Site |

|---|---|---|---|---|

| CREDIT.ORG - NEW JERSEY BRANCH | 90795 | 11 White St, Eatontown, New Jersey, 07724-1524 | (201) 365-4197 | credit.org |

| GARDEN STATE CONSUMER CREDIT COUNSELING, INC. D/B/A/ NAVICORE SOLUTIONS | 84870 | 200 US Highway 9, Manalapan, New Jersey, 07726-3072 | (732) 409-6281 | navicoresolutions.org |

| NAVICORE SOLUTIONS - MANALAPAN, NJ | 82226 | 200 US Highway 9, Manalapan, New Jersey, 07726-3072 | (732) 409-6281 | navicoresolutions.org |

Did you know? New Jersey does not currently mandate in-person counseling — though Senate Bill 264 (discussed above) proposes to change that. For now, you have the right to choose. Visit our counseling page for a list of phone-based counseling agencies, and you can conduct your required counseling from the comfort of your home.

New Jersey Reverse Mortgage FAQs

Will a reverse mortgage affect my Senior Freeze (Property Tax Reimbursement) benefits in New Jersey?

Will a reverse mortgage affect my ANCHOR Property Tax Relief benefit in New Jersey?

Does New Jersey have a property tax deferral program, and can I participate if I have a reverse mortgage?

How does a reverse mortgage affect NJ FamilyCare (Medicaid) eligibility?

What is New Jersey’s Medicaid Estate Recovery Program, and how does it relate to reverse mortgages?

Does my spouse need to be on the reverse mortgage in New Jersey?

Can I place my reverse mortgage in a living trust in New Jersey?

Ready to Unlock Your Home’s Equity?

As New Jersey’s #1 Rated Reverse Mortgage Lender, All Reverse Mortgage, Inc. (ARLO™) is here to provide trusted guidance, real-time rates, and expert support to help you make informed decisions.

✔ No obligations. Just real-time rates and expert advice.

✔ Instant quote. No personal info required.

✔ Licensed experts. Get clear, honest answers.

All Reverse Mortgage, Inc. is fully licensed by the New Jersey Department of Banking & Insurance (License #0509639), ensuring that you receive expert guidance every step of the way.

Get Your Reverse Mortgage Quote from New Jersey’s #1 Rated Reverse Mortgage Lender* or call (800) 565-1722 to speak with a licensed expert.

Other Areas of Interest in New Jersey

Brick Township Jackson Township Manchester Neptune Township Tom's River

Additional Resources: