Reverse Mortgages in Conroe

|

Michael G. Branson, CEO of All Reverse Mortgage, Inc., and moderator of ARLO™, has 45 years of experience in mortgage banking, with the past 20 years devoted exclusively to reverse mortgages. A Forbes Real Estate Council member, he developed the industry's first fixed-rate jumbo reverse mortgage and has been featured in Forbes, Kiplinger, the LA Times, and Yahoo Finance. (License: NMLS# 14040) |

|

Cliff Auerswald, President of All Reverse Mortgage, Inc., and co-creator of ARLO™ — the industry's first real-time reverse mortgage pricing engine — has 27 years of experience in mortgage banking, with 20+ years focused exclusively on reverse mortgages. A recognized expert in reverse mortgage technology and consumer education, he has been featured in Kiplinger, Yahoo Finance, Realtor.com, and HousingWire. (License: NMLS# 14041) |

Conroe Reverse Mortgage Market Overview

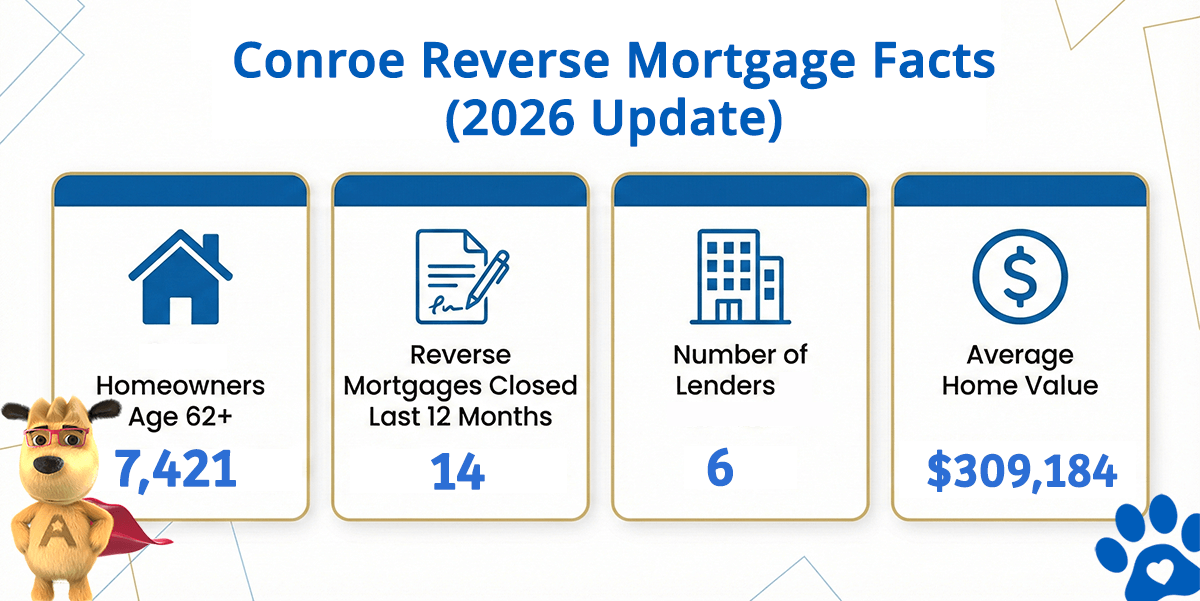

Conroe Reverse Mortgage Facts (2026 Update)

| City | Homeowners Age 62+ | Reverse Mortgages Closed Last 12 Months | Lenders in Conroe (est) | Avg. Home Value |

|---|---|---|---|---|

| Conroe | 7,421 | 14 | 6 | $309,184 |

Conroe’s Growing Retiree Base and Housing Market

Conroe sits at the heart of Montgomery County’s residential boom, located about 40 miles north of Houston. Over the past two decades, this region has transformed from a quieter forestry and oil-focused economy into a vibrant suburban destination. The city and surrounding areas now support approximately 7,400 households headed by residents age 62 and older. Home values in Conroe have held steady around $309,184, making it an attractive market for retirees seeking affordability compared to Houston proper while maintaining access to world-class medical facilities and cultural attractions.

The housing stock in Conroe reflects multiple development waves. Older neighborhoods near downtown feature 1970s and 1980s brick homes with mature trees and charm, while newer communities like Seven Bridges, Westside Estates, and Spring Creek offer contemporary homes built within the last 15 years. Many retirees have lived here for 20, 30, or even 40 years, paying off their mortgages long ago. With 14 HECM loans closed in the past 12 months and six active lenders operating in the area, Conroe homeowners have meaningful choice when considering reverse mortgage options. Unlike common misconceptions, many borrowers here view a reverse mortgage not as a last resort but as a strategic tool to unlock equity they’ve worked decades to build.

Conroe’s economy has matured well beyond its oil-and-timber origins. Today, the region hosts ExxonMobil’s North American operations, one of the world’s largest petrochemical complexes at Baytown, plus numerous manufacturing facilities and corporate back-offices for Houston-based firms. The University of Houston-Conroe campus brings educational jobs and younger professionals. Medical employment has grown substantially with the expansion of CHI St. Luke’s Health and other hospital networks. This economic diversity means Conroe retirees often spent entire careers with stable employers, building homes free and clear or with minimal debt—the exact profile suited to reverse mortgage benefits.

How Reverse Mortgages Work

A reverse mortgage enables homeowners age 62 and older to borrow against their home’s equity without making monthly mortgage payments. The most widely available option is the Home Equity Conversion Mortgage (HECM), a federally-insured product that allows you to remain the owner of your home while accessing your accumulated equity.

Key features include: You keep your name on the deed and continue living in your home. The loan doesn’t require monthly mortgage payments as long as you maintain the property, keep current on property taxes and homeowners insurance, and stay as your primary resident. The loan matures when you sell, permanently leave the home, or pass away—at which point the balance is repaid from sale proceeds or your heirs’ resources.

Common Uses for Conroe Homeowners

- Building a financial cushion — Many retirees worry about unexpected medical expenses or long-term care costs; a flexible credit line provides a safety net that grows over time.

- Staying in the home longer — Home care, aging-in-place modifications, and community involvement often cost money; reverse mortgage proceeds let retirees remain in their neighborhoods rather than downsizing.

- Eliminating debt and improving cash flow — Conroe residents who still carry second mortgages or HELOC balances can clean them up with reverse mortgage proceeds, reducing monthly obligations.

- Supporting adult children or grandchildren — Some borrowers use proceeds to help pay for college, weddings, or down payments for their family members.

Eligibility Requirements for Conroe Homeowners

| Requirement | Details |

|---|---|

| Age | 62 or older (at least one borrower) |

| Property | Primary residence — single-family home, condo, or manufactured home on permanent foundation |

| Equity | Adequate equity in the property (minimum 50% typically required) |

| Counseling | Counseling through a HUD-approved agency required before loan proceeds |

| Financial Assessment | Lender reviews income, credit history, and capacity to maintain home expenses |

Conroe homeowners can get a quick estimate of their reverse mortgage options — just enter your home’s approximate value and your age.

What Costs Should You Expect?

Reverse mortgage expenses include an origination fee, FHA mortgage insurance premium, appraisal fees, title insurance, and other third-party closing costs. Interest accumulates over the life of the loan, though most expenses are rolled into the loan balance rather than paid upfront.

To understand your specific situation, review our detailed cost breakdown and explore our program fundamentals guide. This will help you compare a reverse mortgage against other equity options available to Conroe homeowners.

Is This Right for Your Conroe Home?

A reverse mortgage makes sense if you plan to remain in your home long-term and want to improve cash flow without selling or taking on monthly debt payments. It’s less suitable for homeowners who expect to move within 5 years or who want to preserve as much equity as possible for heirs.

To learn more about the process, read our resource on what a reverse mortgage actually is and understand how the loan is handled after your passing by reviewing our guide on how the loan is settled after passing.

Direct Lender for Montgomery County

All Reverse Mortgage, Inc. (ARLO) originates and funds reverse mortgages directly for Conroe and Montgomery County homeowners. We’re not a broker—we handle everything in-house from initial consultation through closing, ensuring a transparent, straightforward process.

Verify our standing with the HUD lender verification system or check our Better Business Bureau profile. We hold a license from the Texas Department of Savings & Mortgage Lending (License #84280).

Get Your Conroe Reverse Mortgage Estimate

Calculator shows your estimated proceeds with today’s rates — free, fast, and no personal information needed.

Related Resources