Reverse Mortgages in Bethlehem

|

Michael G. Branson, CEO of All Reverse Mortgage, Inc., and moderator of ARLO™, has 45 years of experience in mortgage banking, with the past 20 years devoted exclusively to reverse mortgages. A Forbes Real Estate Council member, he developed the industry's first fixed-rate jumbo reverse mortgage and has been featured in Forbes, Kiplinger, the LA Times, and Yahoo Finance. (License: NMLS# 14040) |

|

Cliff Auerswald, President of All Reverse Mortgage, Inc., and co-creator of ARLO™ — the industry's first real-time reverse mortgage pricing engine — has 27 years of experience in mortgage banking, with 20+ years focused exclusively on reverse mortgages. A recognized expert in reverse mortgage technology and consumer education, he has been featured in Kiplinger, Yahoo Finance, Realtor.com, and HousingWire. (License: NMLS# 14041) |

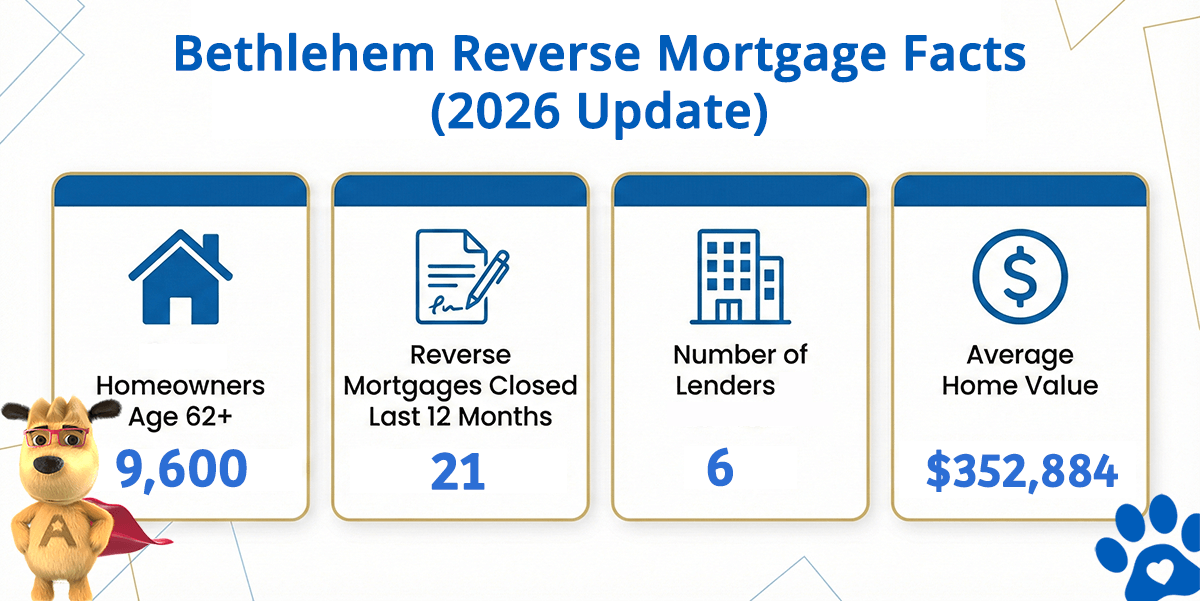

Bethlehem Reverse Mortgage Market at a Glance

Bethlehem Reverse Mortgage Facts (2026 Update)

| City | Homeowners Age 62+ | Reverse Mortgages Closed Last 12 Months | Lenders in Bethlehem (est) | Avg. Home Value |

|---|---|---|---|---|

| Bethlehem | 9,600 | 21 | 6 | $352,884 |

How this data was derived

Reverse mortgage counts reflect FHA-insured HECM loans endorsed over a rolling 12-month period (Dec 2024–Nov 2025) using HUD HECM Snapshot data. Active lenders represent unique FHA sponsor numbers with at least one endorsed loan during this period. Estimated homeowners age 62+ are based on U.S. Census ACS 5-year owner-occupied households aged 65+ as a conservative proxy. Home values are sourced from Zillow’s Home Value Index (latest available).

What the Numbers Tell Us About Bethlehem

Bethlehem is one of eastern Pennsylvania’s most established cities, located in the Lehigh Valley region of Northampton County. Founded in 1741 by Moravian settlers, Bethlehem has evolved from a steel manufacturing center — anchored for over a century by Bethlehem Steel — into a diverse regional hub supported by healthcare, education (including Lehigh University and Moravian University), and a growing arts and culture economy. The city’s historic neighborhoods contain a significant stock of well-maintained older homes, many held by families who have been part of the community for decades.

With approximately 9,600 homeowners aged 62 and older and an average home value of $352,884, most Bethlehem properties fall well within the federal HECM lending limit of $1,249,125. The standard FHA-insured program is the most appropriate option for the majority of eligible homeowners here, offering strong borrower protections, flexible disbursement options, and the non-recourse guarantee that ensures neither you nor your heirs will ever owe more than the home is worth.

Bethlehem Market Context

Bethlehem’s housing stock reflects the city’s layered history — from colonial-era stone homes on the north side to Victorian and early twentieth-century rowhomes in the south, along with mid-century neighborhoods and newer developments on the city’s edges. Many senior homeowners purchased during earlier decades when the Lehigh Valley was still a more affordable alternative to the New York metro area, building meaningful equity as regional demand has grown. For retirees on fixed incomes, managing property taxes, insurance, and the rising cost of daily necessities in a region that has experienced steady appreciation can present financial challenges that equity conversion is well suited to address.

Because most Bethlehem home values fall within the federal HECM lending limit of $1,249,125, the standard FHA-insured program covers the vast majority of properties. Some homeowners in premium neighborhoods or with larger historic properties may approach the limit, in which case jumbo reverse mortgage programs offer an alternative — but most Bethlehem residents will find the standard HECM provides the strongest combination of borrower protections and available proceeds.

How a Reverse Mortgage Works

A reverse mortgage allows homeowners aged 62 and older to convert a portion of their home equity into funds — without selling, moving, or making monthly mortgage payments. The loan is repaid when the last borrower permanently leaves the home, and it carries a non-recourse guarantee, meaning neither you nor your heirs will ever owe more than the home is worth at the time of repayment.

Funds can be received as a lump sum, monthly payments, a flexible line of credit, or a combination — depending on which structure best supports your retirement plan. You retain full ownership of the home and can sell or refinance at any time.

Common Uses in Bethlehem

Homeowners across Bethlehem and Northampton County use reverse mortgages in a variety of ways, depending on their individual financial situation and long-term goals. The most common applications include:

Eliminating an existing mortgage payment to reduce monthly fixed costs — particularly valuable for Bethlehem retirees managing Northampton County property taxes and insurance on a fixed retirement income

Establishing a line of credit that grows over time — a strategic reserve for healthcare expenses, home maintenance, or long-term care planning that grows regardless of home value fluctuations

Supplementing retirement income to maintain quality of life in the Lehigh Valley without selling a home that has built meaningful equity over decades of ownership

Funding repairs or accessibility modifications on older homes — helping long-term homeowners age in place safely in Bethlehem’s established historic neighborhoods

Eligibility at a Glance

| Requirement | Details |

|---|---|

| Age | 62 or older (at least one borrower) |

| Property type | Primary residence — single-family, townhome, FHA-approved condo, or 2–4 unit (owner-occupied) |

| Equity | Sufficient equity in the home (varies by age and current interest rates) |

| Financial assessment | Ability to maintain property taxes, insurance, and basic upkeep |

| Counseling | HUD-approved reverse mortgage counseling session required before application |

For a personalized estimate based on your Bethlehem home value, try our free reverse mortgage calculator — no personal information required.

Understanding Costs and Protections

Reverse mortgages carry upfront and ongoing costs that are important to understand before proceeding. These typically include an origination fee, FHA mortgage insurance premium (for HECM loans), third-party closing costs, and a servicing fee. Most of these costs can be financed into the loan rather than paid out of pocket.

The federal HECM program includes several borrower protections that distinguish it from other financial products: the non-recourse guarantee limits repayment to the home’s value, FHA insurance ensures loan funds remain available even if the lender exits the market, and borrowers retain full ownership of the home throughout the life of the loan. Understanding both the benefits and limitations is an important part of making an informed decision.

Is a Reverse Mortgage Right for You?

A reverse mortgage is not the right fit for everyone — and understanding when it makes sense is just as important as understanding how it works. It tends to be most beneficial for homeowners who plan to stay in their home for the foreseeable future, have meaningful equity, and want to improve their monthly cash flow or establish a financial safety net without selling.

If you are considering downsizing in the near term, have very limited equity, or are looking for a short-term financial fix, other options may be more appropriate. A candid conversation about your specific situation — including your estate planning goals and how a reverse mortgage interacts with your overall financial picture — is the best starting point.

HUD-Approved Lender Serving Bethlehem

All Reverse Mortgage, Inc. (ARLO™) is a HUD-approved direct lender serving Bethlehem and all of Northampton County. As a company that has focused exclusively on reverse mortgages for more than two decades, we bring a depth of experience that generalist lenders cannot match — including firsthand involvement in the development of the first fixed-rate jumbo reverse mortgage program in 2008.

We are licensed by the Department of Banking and Securities (License #38143) and offer both the federally insured HECM program and proprietary jumbo programs for higher-value properties. Our familiarity with both program types ensures Bethlehem homeowners receive guidance tailored to their specific property value and financial goals — particularly relevant in a market shaped by the Lehigh Valley’s transition from industrial economy to diversified regional center.

Pennsylvania’s #1 Rated Reverse Mortgage Lender

Compare our rates, costs, and customer reviews with any lender in the state.

or call (800) 565-1722

Related Resources

Pennsylvania Reverse Mortgage Guide

State-level program information and lender details

Key terms and definitions explained clearly

What to expect from the FHA home appraisal

Program Rules and Requirements

Eligibility criteria and borrower obligations

Required counseling session overview and what to prepare

Philadelphia Reverse Mortgages

Pennsylvania’s largest city to the south

Historic Lancaster County borough to the southwest

How living trusts interact with reverse mortgage programs