|

Michael G. Branson, CEO of All Reverse Mortgage, Inc., and moderator of ARLO™, has 45 years of experience in mortgage banking, with the past 20 years devoted exclusively to reverse mortgages. A Forbes Real Estate Council member, he developed the industry's first fixed-rate jumbo reverse mortgage and has been featured in Forbes, Kiplinger, the LA Times, and Yahoo Finance. (License: NMLS# 14040) |

|

Cliff Auerswald, President of All Reverse Mortgage, Inc., and co-creator of ARLO™ — the industry's first real-time reverse mortgage pricing engine — has 27 years of experience in mortgage banking, with 20+ years focused exclusively on reverse mortgages. A recognized expert in reverse mortgage technology and consumer education, he has been featured in Kiplinger, Yahoo Finance, Realtor.com, and HousingWire. (License: NMLS# 14041) |

Reverse Mortgage Fixed Rate & Unusable Funds Explained

If you have decided that you’d like to use a reverse mortgage to tap into your home equity while remaining in your home, there are several considerations that will help you determine how to make the most out of your loan. A reverse mortgage can be an excellent way for some households to boost their cash flow in retirement, establish a “rainy day” fund for health care expenses or other unexpected costs, or provide a lump sum for a pressing expense such as home renovations or maintenance.

If you are 62 or older and have enough home equity to qualify, a Home Equity Conversion Mortgage (HECM), the most common reverse mortgage type and insured by the Federal Housing Administration, may be the solution for your retirement needs. The decisions you make regarding how and when you will access your proceeds and the type of interest rate you choose could make a real difference in how much you can borrow.

One of those decisions is whether you opt for a fixed or adjustable rate – both options are available to borrowers.

Fixed-rate lump sum restrictions

Several years ago, the Department of Housing and Urban Development, the government agency that oversees the HECM program, placed some new rules on fixed rate reverse mortgages. The new rules were intended to prevent borrowers from drawing all their accessible home equity and spending it at once. The rules essentially restrict fixed-rate borrowers by allowing them access to less funds in total than if they were to take out an adjustable-rate loan.

Taking a fixed-rate reverse mortgage can leave some money on the table that borrowers otherwise would be able to access under an adjustable rate. But how much home equity you have versus how large a mortgage you have can make a major difference in the amount you ultimately will be able to borrow.

If you own your home free and clear, you may be leaving a lot of your home equity untapped when you could access it via an adjustable-rate reverse mortgage.

Also See: Reverse Mortgage Types: Lump Sum Payout -VS- Line of Credit

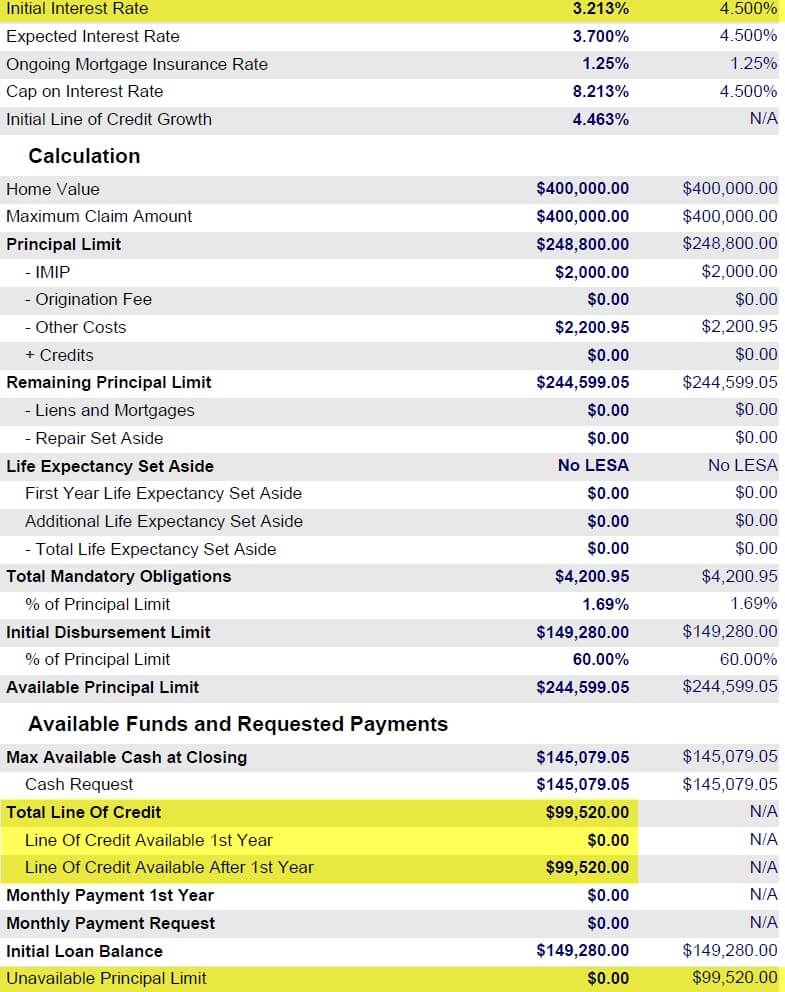

Scenario 1: Borrower owns a home outright (free & clear)

- Option 1: The borrower takes out an adjustable rate reverse mortgage with an initial interest rate of 3.213%.

*ILLUSTRATION FOR BORROWER AGE 75 as of the date of this article. This example is run to illustrate the difference between fixed and adjustable rate programs and payment options, not interest rate availability. Rates are subject to change and the amount you receive under the program is also affected by current interest rates.

The amount available at closing is $145,079

The line of credit available after the first year is $99,520.

- Option 2: He takes out a fixed-rate reverse mortgage with an initial interest rate of 4.5%.

The amount provided at closing is $145,079.

No line of credit is available after the first year since all proceeds are taken upfront. Therefore, there is $99,520 in unused principal limit. The borrower is much better off taking the adjustable rate option when the home is owned free and clear.

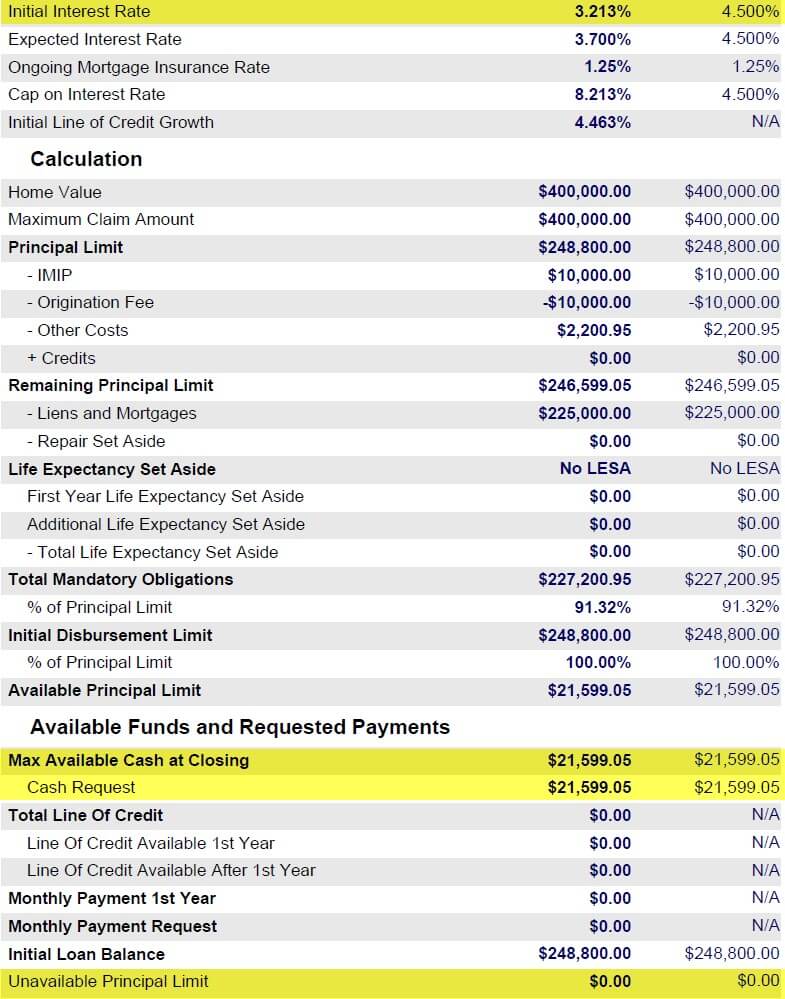

Scenario 2: Borrower has a mortgage of $225,000.

- Option 1: The borrower takes out an adjustable-rate reverse mortgage with an initial interest rate of 3.213%.

The amount available at closing is $21,599.

There are no additional funds available.

- Option 2: The borrower takes out a fixed-rate reverse mortgage with an initial interest rate of 4.5%.

The amount available at closing is $21,599.

The borrower can access the exact same funds regardless of whether he chooses a fixed-rate or an adjustable-rate loan when he has a mortgage balance of $225,000.

The bottom line

Homes that are owned free and clear can leave a lot of equity on the table or unable to be borrowed when choosing a fixed-rate reverse mortgage. But for borrowers who have a large mortgage balance, the proceeds can be much closer under the two options—they can even be the same.

ARLO recommends these helpful resources:

Have a Question About Reverse Mortgages?

Over 2000 of your questions answered by ARLO™

Ask your question now!

July 15th, 2023

July 20th, 2023

August 5th, 2019

August 8th, 2019

December 12th, 2016

December 12th, 2016