Free Reverse Mortgage Calculator

|

Michael G. Branson, CEO of All Reverse Mortgage, Inc., and moderator of ARLO™, has 45 years of experience in mortgage banking, with the past 20 years devoted exclusively to reverse mortgages. A Forbes Real Estate Council member, he developed the industry's first fixed-rate jumbo reverse mortgage and has been featured in Forbes, Kiplinger, the LA Times, and Yahoo Finance. (License: NMLS# 14040) |

|

Cliff Auerswald, President of All Reverse Mortgage, Inc., and co-creator of ARLO™ — the industry's first real-time reverse mortgage pricing engine — has 27 years of experience in mortgage banking, with 20+ years focused exclusively on reverse mortgages. A recognized expert in reverse mortgage technology and consumer education, he has been featured in Kiplinger, Yahoo Finance, Realtor.com, and HousingWire. (License: NMLS# 14041) |

Free Reverse Mortgage Calculator | No Personal Info Required (2026)

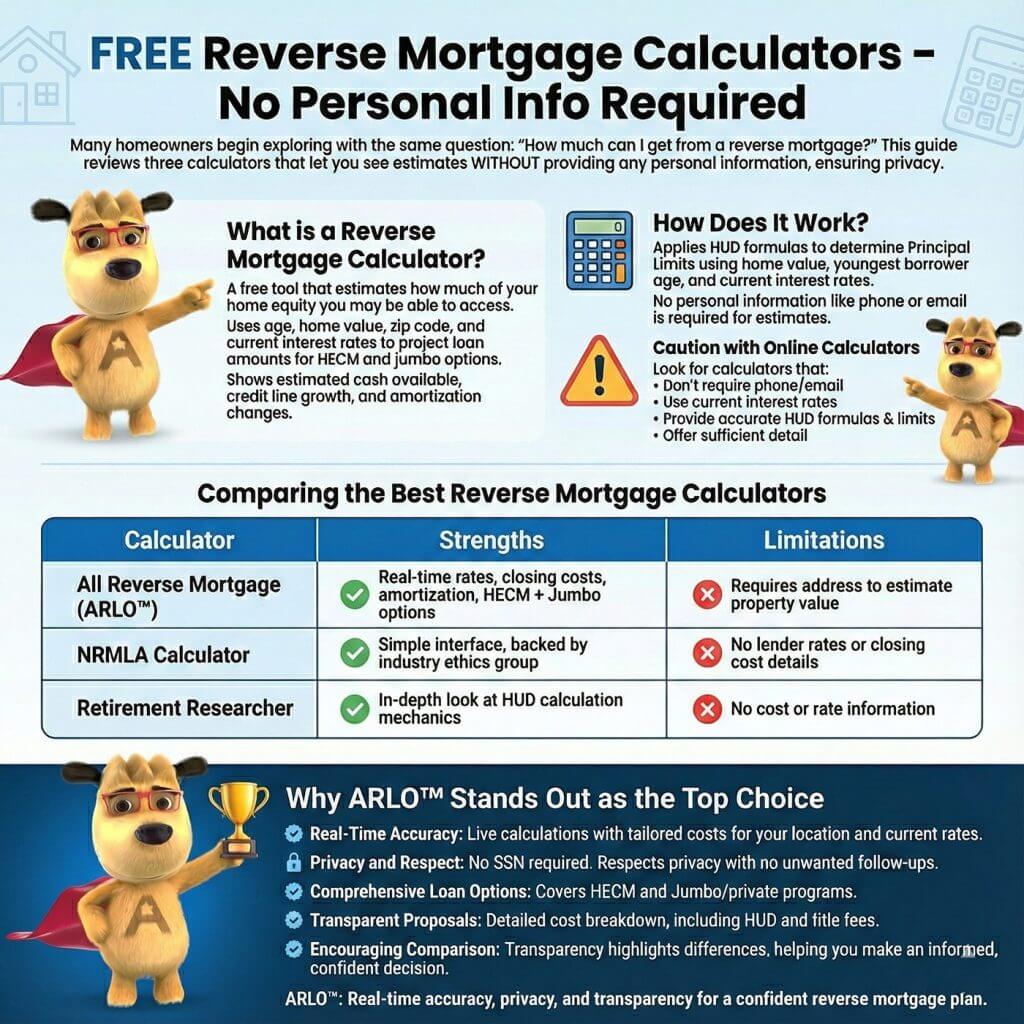

Free Reverse Mortgage Calculators That Don’t Ask for Personal Information

Many homeowners begin exploring a reverse mortgage with the same question:

How much can I get from a reverse mortgage?

The challenge is that most online calculators won’t give you an answer unless you provide your phone number or email address. That creates hesitation for anyone who wants to learn without being contacted.

This guide reviews three calculators that let you see your estimated loan amount without providing any personal information. These tools are private, use current data, and give you a clear starting point before talking with a lender.

What Is a Reverse Mortgage Calculator?

A reverse mortgage calculator is a free tool that estimates how much of your home equity you may be able to access through a reverse mortgage. It uses your age, home value, ZIP code, and current interest rates to project loan amounts for available programs. The calculator applies HUD formulas that determine Principal Limits, using your home’s value, the age of the youngest borrower, and current interest rate assumptions.

Most calculators focus on the Home Equity Conversion Mortgage (HECM), but some also include proprietary or jumbo options for higher-value homes. Depending on the program, you may see estimates for lump-sum funds, monthly payments, or a line of credit. These tools won’t replace a full financial review, but they let you learn privately at your own pace.

What to Watch for With Online Calculators

Not all calculators are built with the borrower in mind. Many require personal information before showing results, and some are operated by third-party lead companies that share your data with multiple lenders, which can lead to persistent phone calls or unwanted email follow-up. Others provide only broad estimates that don’t reflect current rates or closing costs.

For a useful and private experience, look for calculators that:

- Don’t require a phone number or email

- Use current interest rates

- Apply accurate HUD formulas and lending limits

- Provide enough detail to understand the options available

The three calculators reviewed below meet those criteria.

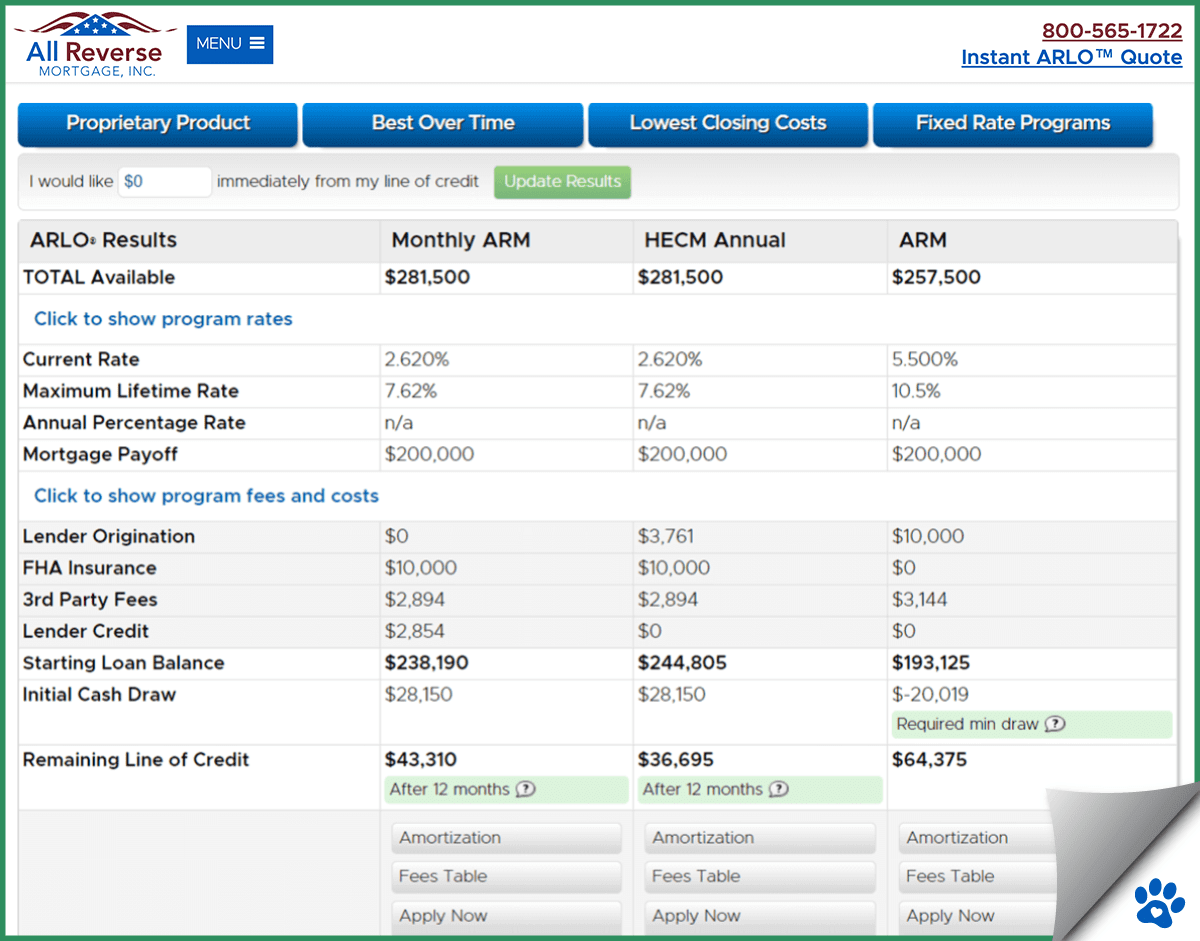

1. All Reverse Mortgage Calculator (ARLO)

The All Reverse Mortgage calculator is built on the same pricing engine used for live loan scenarios, so the results match what you would receive from our lending team. No phone number, email, or Social Security number is required.

To use the calculator, enter your ZIP code, home value, date of birth, and existing mortgage balance (if any). The tool returns results for both HECM and jumbo programs, along with origination costs based on loan type and rate, and amortization schedules projecting up to 20 years.

This level of detail lets you compare program options and understand how each affects your available funds, costs, and long-term equity position. You won’t receive any follow-up calls or emails from using the tool.

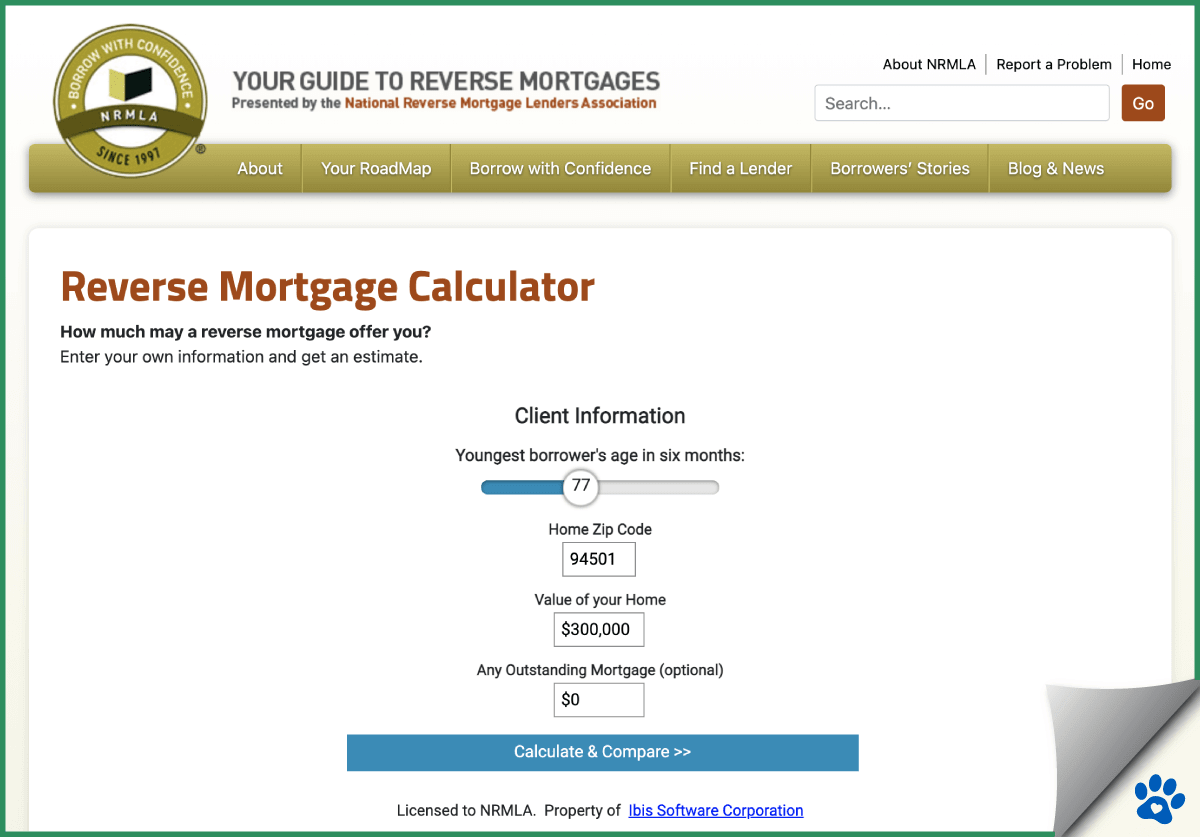

2. NRMLA Reverse Mortgage Calculator

The NRMLA Reverse Mortgage Calculator is provided by the National Reverse Mortgage Lenders Association, an industry trade and ethics advocacy group. It serves as a reliable starting point for initial estimates.

Enter your ZIP code, adjust the slider to the youngest borrower’s age, and input your home’s estimated value. The calculator displays approximate amounts for annual adjustable, monthly adjustable, and fixed-rate loan types.

The NRMLA calculator does not include lender-specific rates or closing costs, so the amounts shown may differ from what you ultimately qualify for. It works best as a first look before moving to a more detailed tool.

3. Retirement Researcher’s Independent Calculator

The Retirement Researcher calculator is an advanced tool designed for users who already understand reverse mortgage mechanics and want to explore the HUD factor tables directly.

Enter your loan terms, age, and property details. The calculator focuses on the Principal Limit Factors that determine HECM loan amounts and allows you to add parameters like funds reserved for repairs or reserves required for income or credit conditions.

This tool does not include costs, interest rates, or lender-specific details, making it less practical for direct cost comparisons. It works best for understanding how HUD calculates loan amounts and pairs well with a more detailed calculator for complete estimates.

How the Three Calculators Compare

All three tools offer value, but they differ in depth and accuracy. The table below summarizes where each calculator falls in terms of features, privacy, and detail.

Comparing the Best Reverse Mortgage Calculators

| Calculator | Strengths | Limitations |

|---|---|---|

| All Reverse Mortgage (ARLO™) | Real-time rates, closing costs, amortization, HECM + Jumbo options | Requires address to estimate property value |

| NRMLA Calculator | Simple interface, backed by industry ethics group | No lender rates or closing cost details |

| Retirement Researcher | In-depth look at HUD calculation mechanics | No cost or rate information |

The All Reverse calculator provides the most complete estimate because it uses real-time lender pricing, includes closing costs by ZIP code, covers both HECM and jumbo programs, and generates a written proposal with a full cost breakdown. The NRMLA calculator is the best starting point for a quick ballpark estimate. The Retirement Researcher tool is most useful for borrowers who want to understand the HUD formulas behind the numbers.

We encourage you to use more than one and compare lenders before making any decision.

See Your Estimate Now: Use the All Reverse Mortgage calculator for real-time rates, detailed closing costs, and personalized loan options, with no personal information required. Or call (800) 565-1722 to speak with a specialist.

Frequently Asked Questions

How does a free reverse mortgage calculator work?

Is there a reverse mortgage calculator for jumbo loans?

Why do some reverse mortgage calculators ask for personal information?

How is interest calculated on a reverse mortgage?

What is the current interest rate for a reverse mortgage?

Have a Question About Reverse Mortgages?

Over 2000 of your questions answered by ARLO™

Ask your question now!