America’s #1 Rated Reverse Lender*

How Lower Interest Rates Drive Larger Reverse Mortgage Amounts

|

Michael G. Branson, CEO of All Reverse Mortgage, Inc., and moderator of ARLO™, has 45 years of experience in mortgage banking, with the past 20 years devoted exclusively to reverse mortgages. A Forbes Real Estate Council member, he developed the industry's first fixed-rate jumbo reverse mortgage and has been featured in Forbes, Kiplinger, the LA Times, and Yahoo Finance. (License: NMLS# 14040) |

|

Cliff Auerswald, President of All Reverse Mortgage, Inc., and co-creator of ARLO™ — the industry's first real-time reverse mortgage pricing engine — has 27 years of experience in mortgage banking, with 20+ years focused exclusively on reverse mortgages. A recognized expert in reverse mortgage technology and consumer education, he has been featured in Kiplinger, Yahoo Finance, Realtor.com, and HousingWire. (License: NMLS# 14041) |

Michael G. Branson

Michael G. Branson Cliff Auerswald

Cliff Auerswald

If You’ve Looked at a Reverse Mortgage in the Past, You May Want to Look Again!

If you have ever investigated a reverse mortgage or have thought about it, especially in the past 24 months and didn’t think the numbers worked for your needs, it may be time to check again. The reason we say this is because one of the main factors that determines how much money you will receive in your reverse mortgage is the interest rate.

Since HUD changed the Floor Rate on the program, borrowers had been receiving less and less money as interest rates rose. However, now that we have seen a drop off in the rates recently, borrowers have been getting more reverse mortgage proceeds than they have for quite a while.

And this is even better news for borrowers with property values at or above the old loan limit of $636,150. HUD raised the lending limit significantly this year when the new limit came out at $970,800, over $90,000 higher than the previous limit. You had to go back to 2009 to see increases like that and then it was part of the stimulus plan but stayed the same for several years before moving slightly higher.

The 2019 limit was a real increase but there was only one problem, the rising rates were eating into the increased loan amounts borrowers expected to receive. Many borrowers saw the new limit as a small help, but not the big increase for which they were hoping.

But now may be the time for all those to give the loan another look. Rates have fallen in the recent past, making the Principal Limit on the loan rise. Borrowers now receive more proceeds on the reverse mortgage loan than they have for a very long time. And since the rates are down, you accrue less interest on the money you borrow as well making it a win-win situation for borrowers at a time when the stock market is not being kind to people’s 401’s and other investments.

Why does a reverse mortgage give you more money now than it did in the past?

As we stated, HUD uses several factors to determine the amount of money the borrowers will be eligible to receive under the program. This benefit amount is called their “Principal Limit” and it’s the maximum loan amount before any line of credit growth or any limitations HUD places on draws and I will get into that in a minute.

Your Principal Limit is the amount of money you are eligible for, but your available Principal Limit may be different based on how you wish to draw the funds. For example, if you are using all the money to pay off existing loans, all the funds are available, and HUD does not place a limitation on the proceeds under the adjustable line of credit or the fixed rate loan.

However, if you do not have a loan on your home now, HUD limits the amount you can draw at closing or in the first 12 months on any of the programs to 60% of your Principal Limit. Furthermore, there is only one draw allowed on the fixed rate program so anything that you cannot take at closing, you would forfeit on the fixed rate product. If you combine the HUD limitations on the draws with amounts that could be dropped by thousands of dollars by increased interest rates, many borrowers felt that the loan just didn’t meet their needs.

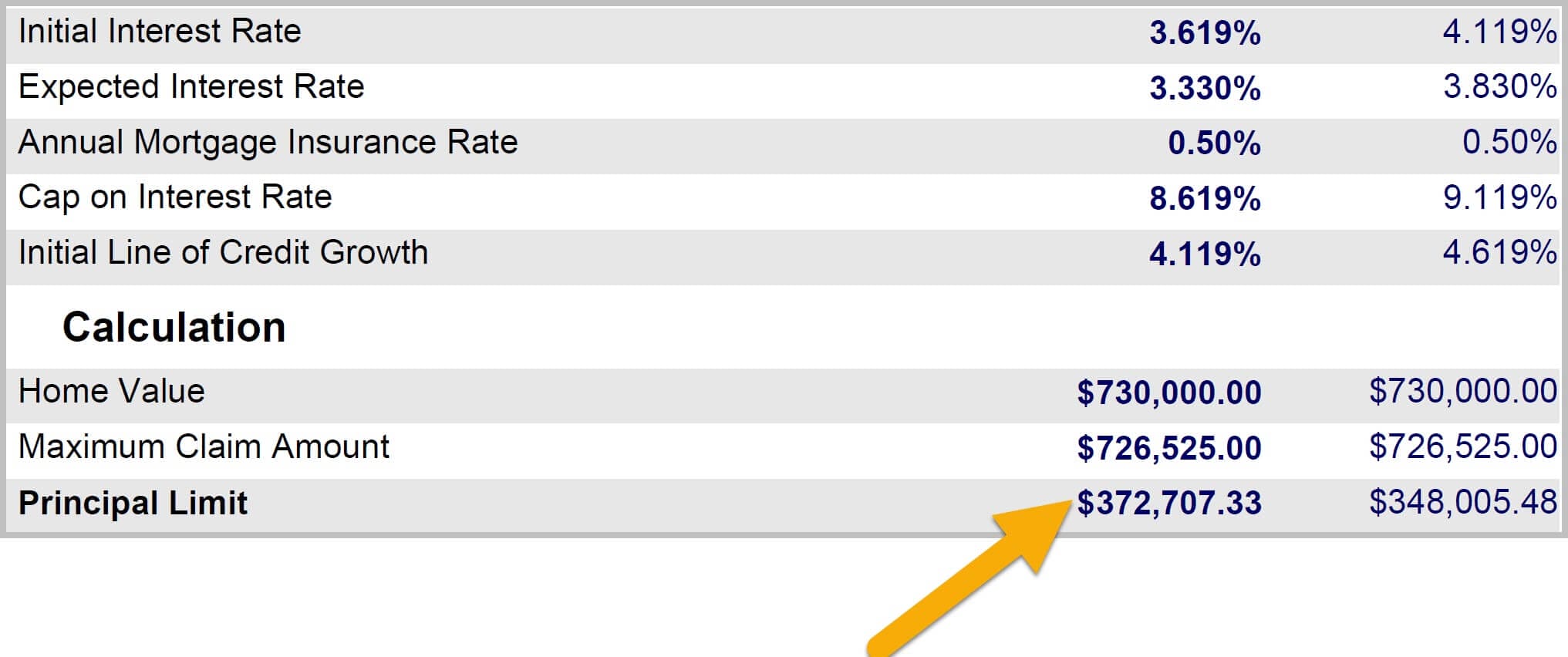

HUD uses the 10-year LIBOR index to determine the “Expected Rate” which is the rate that will determine the amount of money you receive with your loan, even though it is a rate at which you do not accrue interest. The importance of this rate though is huge. You may not accrue interest on your loan at this rate, but the longer-term rate is higher than the 1-year rate on your mortgage if you have the line of credit program and therefore, the interest rate used to determine your loan amount is higher. The higher the rate, the lower the proceeds.

This didn’t even come into play before HUD changed the “floor” rate because all loans with an expected rate a little over 5% or less all received the same proceeds and rates were low enough to where all loans were below this rate for years. Then with HUD moving this floor to 3% and rates rising, soon all loans were receiving less money as the rates increased. HUD still has their 60% rule, but now that rates have come down, borrowers are pleased to see that they are receiving more money as a result.

What does all this mean to borrowers? More Money!

We don’t even have to go back a year to do a little comparison that might shock you. For a 62-year-old borrower with a property worth the maximum value or above, the difference the lower rate makes is a little over $24,700 in proceeds to the borrower. That means that same borrower will receive over $24,700 more now versus what they would have gotten just in January or February of this year with no other changes!

Different values and ages will show different results, but I think you will agree that this is huge. This just illustrates that it doesn’t take a 3-year time frame to really make a difference and that it pays to keep abreast of the market. And, based on all the economic news as of late, next week should be even better for borrowers (this is not a guarantee, rates are subject to change and that prediction is based on news events that have already taken place – no one knows for sure what the future will bring).

But if nothing else, we wanted to show borrowers that if you looked before and were not happy with the results, now might be a good time to check it out again. We can’t force HUD to make the loan any more advantageous and we can’t improve the interest rates, but we can tell you when HUD does do something good or rates have improved and that time is now! Lending limits are up, and rates are down.

If you like the idea of more money available to you on your loan at a lower cost to borrow, visit ARLO™ calculator and see what the current rates will do for you. Remember, your expected rate is locked in for 120 days from the date of application with a 1-time “float down” available at the time you order documents if the rates should continue to drop so you have all upside and no downside by looking into it now.

Have a Question About Reverse Mortgages?

Over 2000 of your questions answered by ARLO™

Ask your question now!