|

Michael G. Branson, CEO of All Reverse Mortgage, Inc., and moderator of ARLO™, has 45 years of experience in mortgage banking, with the past 20 years devoted exclusively to reverse mortgages. A Forbes Real Estate Council member, he developed the industry's first fixed-rate jumbo reverse mortgage and has been featured in Forbes, Kiplinger, the LA Times, and Yahoo Finance. (License: NMLS# 14040) |

|

Cliff Auerswald, President of All Reverse Mortgage, Inc., and co-creator of ARLO™ — the industry's first real-time reverse mortgage pricing engine — has 27 years of experience in mortgage banking, with 20+ years focused exclusively on reverse mortgages. A recognized expert in reverse mortgage technology and consumer education, he has been featured in Kiplinger, Yahoo Finance, Realtor.com, and HousingWire. (License: NMLS# 14041) |

All Reverse Mortgage, Inc. is a HUD-approved reverse mortgage lender with more than 20 years of experience focused exclusively on reverse mortgages. We publish research-based guides like this one to help homeowners better understand how reverse mortgages work, what the federal rules allow, and how these loans are commonly used in large housing markets like Chicago.

Our goal is simple: clear explanations, accurate data, and no sales pressure.

Chicago Reverse Mortgage Guide (2026 Data, Limits & HECM Rules)

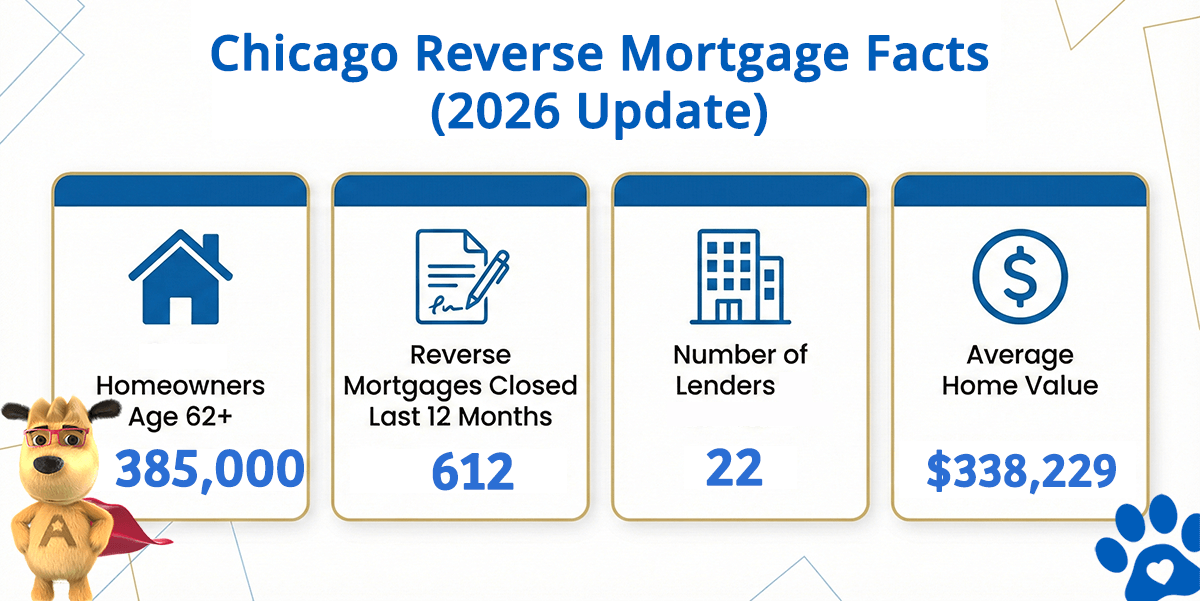

Chicago Reverse Mortgage Facts (2026 Update)

| City | Homeowners Age 62+ | Reverse Mortgages Closed Last 12 Months | Lenders in Chicago (est) | Avg. Home Value |

|---|---|---|---|---|

| Chicago | 385,000 | 612 | 22 | $338,229 |

How this data was derived: Reverse mortgage counts reflect FHA-insured HECM loans endorsed over a rolling 12-month period (Dec 2024–Nov 2025) using HUD HECM Snapshot data. Active lenders represent unique FHA sponsor numbers with at least one endorsed loan during this period. Estimated homeowners age 62+ are based on U.S. Census ACS 5-year owner-occupied households age 65+ as a conservative proxy. Home values are sourced from Zillow’s Home Value Index (latest available).

Understanding the HUD HECM Reverse Mortgage Program

The most common reverse mortgage in the U.S. is the Home Equity Conversion Mortgage (HECM). It is insured by the Federal Housing Administration (FHA) and regulated by the U.S. Department of Housing and Urban Development (HUD).

Key characteristics of a HECM include:

-

Available to homeowners age 62 and older

-

No required monthly mortgage payments

-

Borrowers retain title to the home

-

The loan is repaid when the home is sold, vacated, or the last borrower passes away

-

Federally insured consumer protections apply

Reverse mortgages are no longer viewed as a last resort. Many homeowners now use them strategically to eliminate existing mortgage payments, create cash flow flexibility, or establish a standby line of credit.

Chicago Housing Market Context

Chicago is the third-largest city in the United States, with an estimated population of nearly 2.8 million residents. Approximately 373,000 homeowners are age 62 or older, making Chicago one of the largest reverse mortgage–eligible markets in the country.

As of early 2024, Chicago’s median home value was approximately $309,814, well below the federal HECM lending limit of $1,249,125. This means the vast majority of owner-occupied homes in Chicago fall within standard HECM guidelines.

Homes with values above the federal limit may require proprietary or jumbo reverse mortgage programs, which are privately insured and follow different rules than HUD-backed loans.

How Reverse Mortgages Are Commonly Used in Chicago

Older homeowners in major metro areas like Chicago often explore reverse mortgages to:

-

Pay off an existing mortgage and remove a monthly payment

-

Improve monthly cash flow in retirement

-

Fund home improvements or accessibility upgrades

-

Establish a flexible line of credit for long-term planning

Every situation is different, and reverse mortgages are not suitable for everyone. Understanding the structure, costs, and long-term implications is critical before making any decisions.

Learn More About Reverse Mortgages

If you want to explore how reverse mortgages work nationally, including estimated loan amounts based on age and home value, you can use our online reverse mortgage calculator. It provides instant estimates without requiring personal information.

If you prefer to speak with a licensed reverse mortgage professional in your state, HUD also maintains a public directory of approved counselors and lenders at 800-CALL-FHA.