|

Michael G. Branson, CEO of All Reverse Mortgage, Inc., and moderator of ARLO™, has 45 years of experience in mortgage banking, with the past 20 years devoted exclusively to reverse mortgages. A Forbes Real Estate Council member, he developed the industry's first fixed-rate jumbo reverse mortgage and has been featured in Forbes, Kiplinger, the LA Times, and Yahoo Finance. (License: NMLS# 14040) |

|

Cliff Auerswald, President of All Reverse Mortgage, Inc., and co-creator of ARLO™ — the industry's first real-time reverse mortgage pricing engine — has 27 years of experience in mortgage banking, with 20+ years focused exclusively on reverse mortgages. A recognized expert in reverse mortgage technology and consumer education, he has been featured in Kiplinger, Yahoo Finance, Realtor.com, and HousingWire. (License: NMLS# 14041) |

This page provides an informational overview of reverse mortgage activity and housing trends in Akron, Ohio, based on publicly available federal and housing market data. It is intended for educational purposes only and should not be interpreted as an offer to lend or an indication of licensure in this state.

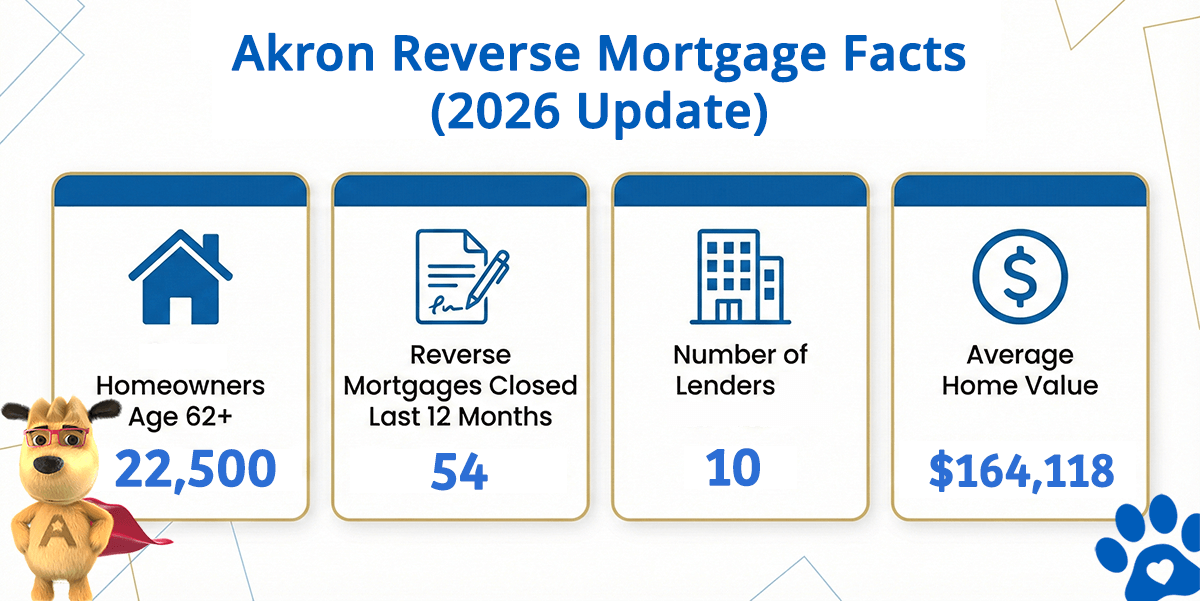

Akron Reverse Mortgage Facts (2026 Update)

| City | Homeowners Age 62+ | Reverse Mortgages Closed Last 12 Months | Lenders in Akron (est) | Avg. Home Value |

|---|---|---|---|---|

| Akron | 22,500 | 54 | 10 | $164,118 |

How this data was derived: Reverse mortgage counts reflect FHA-insured HECM loans endorsed over a rolling 12-month period (Dec 2024–Nov 2025) using HUD HECM Snapshot data. Active lenders represent unique FHA sponsor numbers with at least one endorsed loan during this period. Estimated homeowners age 62+ are based on U.S. Census ACS 5-year owner-occupied households age 65+ as a conservative proxy. Home values are sourced from Zillow’s Home Value Index (latest available).

Understanding HUD HECM Reverse Mortgages

The Home Equity Conversion Mortgage (HECM) is the only reverse mortgage program insured by the Federal Housing Administration (FHA) and overseen by the U.S. Department of Housing and Urban Development (HUD).

A HECM reverse mortgage allows eligible homeowners age 62 or older to access a portion of their home equity while deferring repayment for as long as the home remains their primary residence and property taxes, insurance, and maintenance obligations are met.

HECM loans include federal consumer protections, including:

-

Non-recourse protection (borrowers or heirs never owe more than the home’s value)

-

Required HUD counseling prior to application

-

Federally defined loan limits and payout structures

How Reverse Mortgages Are Commonly Used

Across Ohio markets like Akron, reverse mortgages are most often evaluated by homeowners who want to:

-

Pay off an existing mortgage to remove monthly payment obligations

-

Supplement retirement income

-

Establish a line of credit for future needs

-

Remain in their home long term without selling

Use of reverse mortgages has increasingly shifted toward retirement planning and cash-flow management, rather than emergency borrowing.

HECM vs. Proprietary (Jumbo) Reverse Mortgages

Most homes in Akron fall well below the 2026 FHA HECM lending limit of $1,249,125, making the federally insured HECM program the most common reverse mortgage option in the area.

For higher-value properties that exceed the FHA limit, some homeowners may explore proprietary or jumbo reverse mortgage programs, which are privately funded and not FHA-insured. These programs may offer higher loan amounts but typically involve different rates, terms, and consumer protections.

Choosing between a HECM and a proprietary program depends on home value, age, financial goals, and risk tolerance.

Akron Housing and Demographics Overview

Akron is the fifth-largest city in Ohio, with an estimated population near 198,000 residents. Approximately 17 percent of homeowners are age 62 or older, reflecting a meaningful population that may evaluate reverse mortgage options as part of long-term housing and retirement planning.

Founded in the early 19th century along the Little Cuyahoga River, Akron has historically been associated with rubber and polymer manufacturing. Today, education, healthcare, and advanced materials remain central to the local economy.

The city also offers a strong cultural presence, including the Akron Civic Theatre, extensive park systems, and a well-known role in professional sports history.

Akron Reverse Mortgage Lending Limits (2026)

With an average home value of approximately $164,118, most Akron properties fall comfortably within FHA HECM lending limits. This allows eligible homeowners to consider federally insured reverse mortgage options without requiring proprietary loan programs.