How to Payoff a Reverse Mortgage at 95% of Appraised Value

|

Michael G. Branson, CEO of All Reverse Mortgage, Inc., and moderator of ARLO™, has 45 years of experience in the mortgage banking industry. He has devoted the past 19 years to reverse mortgages exclusively. (License: NMLS# 14040) |

|

All Reverse Mortgage's editing process includes rigorous fact-checking led by industry experts to ensure all content is accurate and current. This article has been reviewed, edited, and fact-checked by Cliff Auerswald, President and co-creator of ARLO™. (License: NMLS# 14041) |

Michael G. Branson

Michael G. Branson Cliff Auerswald

Cliff AuerswaldHello All Reverse,

I have read the information that was provided on the website and the questions and responses. I am concerned that there is some contradictory information here. I would like you to offer some clarification which will help me better understand what happens to my mother’s home and the possible sale to grandchildren.

Since the text on this website states in one paragraph that the loan is non-recourse and the balance is not due to the lender by the heirs of the estate for a shortfall on the reverse mortgage (appraised value of the home vs the loan amount) if the house is sold to a third party.

However, the same paragraph in brackets states that there are no restrictions on family members and that the home can be sold to family members at 95% of the appraised value. I have also noted that in some of your responses, you mentioned that grandchildren and heirs can purchase the home at 95% of the appraised value.

Here is my situation:

My mother passed away in August 2012 with a reverse mortgage balance of $230k. The original mortgage could go as far as approximately $270k. I have kept in contact with the lender and have rented the home kept up the property taxes and made improvements on the home, and kept up the property. I cannot afford to purchase the home, but two of the heirs (grandchildren) are in the process of gaining loans to purchase the property at 95% of the lenders appraisal of 140k. Due to the contradicting verbiage and the responses given to others questions above, I am not sure if this home can or cannot be sold to my mothers grandchildren. Could you help clarify this for me?

Best Regards, Don H.

Hi Don,

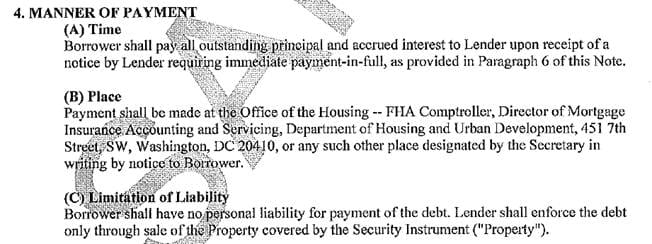

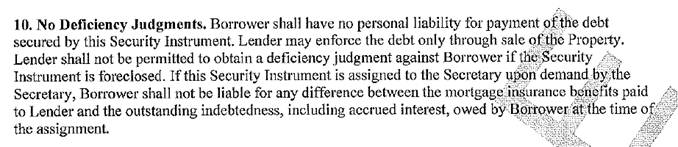

Here is the exact verbiage in the Note and Deed of Trust for the HUD HECM reverse mortgage with regard to no Deficiency Judgment:

Note:

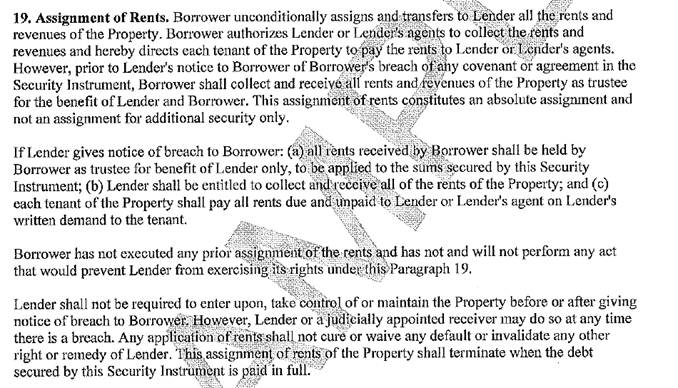

Deed of Trust:

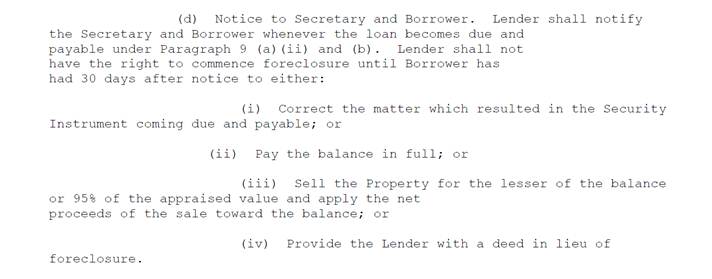

This is the verbiage in the HUD manual 4235.1 which is the manual for reverse mortgages:

What it all boils down to is that the Note, Deed, and Security Agreement that the borrower has signed and the contracts for the loan, if you will, all guarantee that there is no personal liability for the loan. Since there is no personal liability, HUD and the lender can only look to the property to repay the debt.

Therefore, HUD has realized that a sale in the marketplace will cost them money. They will not be able to sell the property for above market value, and the costs will be at least 5%, so if the family sells the home, they can pay the loan off for 95% of the current value of the property or the balance owed, whichever is less.

HUD makes no differentiation in anything I can find, they only talk about the right to sell the home for a minimum of 95% of the current appraised value, and there is no restriction about to whom the home is sold.

Having said that, you brought up another issue here that I would like to touch on. The Deed of Trust also contains provisions for the Assignment of Rent (and you mentioned that you rented the property).

You do need to keep this in mind when dealing with the lender and HUD:

The sooner you can complete the sale, the better, as all rent should go to the lender.

ARLO recommends these helpful resources:

May 23rd, 2023

May 23rd, 2023

May 20th, 2022

May 23rd, 2022

February 1st, 2022

February 2nd, 2022

July 11th, 2021

July 19th, 2021

March 30th, 2021

March 30th, 2021

October 22nd, 2020

October 22nd, 2020

October 8th, 2020

October 8th, 2020

September 23rd, 2020

September 23rd, 2020

September 4th, 2019

September 4th, 2019

August 20th, 2019

August 25th, 2019

April 4th, 2018

April 4th, 2018

September 13th, 2016

September 14th, 2016

September 7th, 2013